Hershey and One Brands: Confectionery Company Continues Diversification Through Acquisitions

On Sept. 23, The Hershey Co. (NYSE:HSY) completed the acquisition of protein bar company One Brands for $397 million. The closing of the deal came slightly ahead of schedule, as it was originally meant to be completed in the fourth quarter.

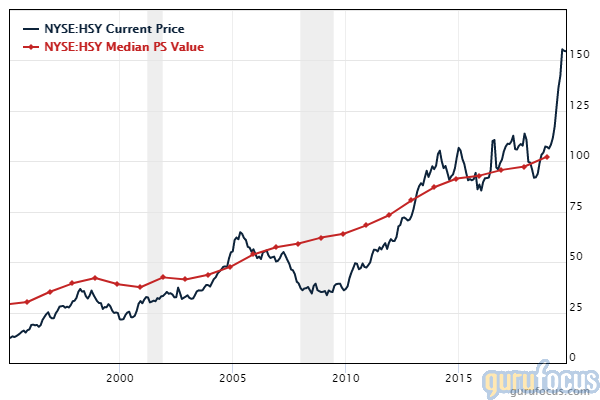

Hershey is best known as a confectionary giant, some of its most popular products being Kit Kats, Reese's, Jolly Ranchers and many types of chocolate. With a market cap of $30.8 billion and an enterprise value of $34.8 billion, this stalwart has achieved steady growth and strong stock valuation. In 2018-19, the share price has skyrocketed to the overvalued range, according to the company's median price-sales value.

Acquisitions

The acquisition of One Brands marks Hershey's first foray into the protein bar market. Founded in 1999 by Ron McAfee, One Brands makes protein bars that are meant to taste like cakes, candies and donuts. Their popular flavors include birthday cake, chocolate brownie and cinnamon roll.

"ONE Brands is a great addition to Hershey's growing portfolio of better-for-you snacking brands, and we are excited about getting to work with this talented team," said Mary Beth West, chief growth officer, about the acquisition. "As the nutrition bar category continues to grow, ONE offers a compelling brand proposition with great-tasting, unique flavors, low sugar and high protein."

One Brands is the most recent acquisition in Hershey's quest to turn itself from a famous chocolate producer to a famous snack producer. Previous acquisitions include KRAVE Jerky (2015), Ripple Brand Collective (2016), Amplify Snack Brands (2017) and Pirate Brands (2018), and popular brand names gained form these acquisitions include Krave Jerky, SimplyPop, Oatmega and barkTHINS.

Diversification or 'diworseification'

Given that many companies have suffered from rapid acquisitions, some may worry that Hershey is overreaching itself and that its acquisitions will flop. Bad acquisitions (or 'diworseifications' as Peter Lynch calls them) are acquisitions that put a drain on the acquirer that is more than the profits received from the new business.

Certainly, many of Hershey's new brands would not benefit from having the company's name attached to them. Frequent buyers of gluten-free Krave Jerky, for example, might feel a bit suspicious upon finding out that Hershey owns the brand name. Products claimed to be gluten-free are sometimes falsely labelled, and in these cases, gluten will show up as part of the natural flavors or as "naturally occurring in soy sauce." Brand trust is key to consumer decisions in these instances, and Hershey isn't exactly famous for being gluten-free - quite the opposite, in fact. However, since Hershey is not sticking its label on all these new "better-for-you" products, customers are unlikely to notice there has been any change.

In terms of profit margins, Hershey has long enjoyed an enviable 45% profit margin, which its smaller acquisitions are not able to achieve. Competing companies in the packaged foods sector almost all have profit margins of 40% or below, and small companies like One Brands and Krave are not exceptions. Profit margins are not everything, though, and the Hershey company believes that appealing to more health-minded customers is more valuable than maintaining the highest possible statistics in any certain measurement.

Given Hershey's three-year revenue growth rate of 3.3%, this may be the wisest approach. Hershey currently shares a duopoly with Mars in the confection industry; Hershey has approximately 44% of the market, while Mars has approximately 30%, with no other competitor having more than 10% of the market share. Expanding into other types of snack foods and appealing to consumers who are not attracted to its other offerings may be the only way for the company to continue growing in the U.S.

In addition to this, though Hershey has acquired brands that are pickier about their ingredients, it has avoided trying to break into the true health food market, which would mark a real diworseification. The acquisition of One Brands is likely to be successful because One Brands appeals to Hershey's typical customer base while also expanding into the market of people who exercise and care more about food quality. While more health-conscious than the company's main products, One Brands still appeals to consumers who want healthier food that tastes like candy.

Looking forward

As mentioned above, Hershey's stock price may have reached the overvalued range recently. However, the company recently posted strong third-quarter results, with net sales increasing 2.6% and sales in China increasing 12% (adjusted for currency exchange at a 21.8% margin). Adjusted earnings per share for the quarter were $1.61, an increase of 3.9% that is in line with analyst estimates.

In terms of the company's stability long term, Hershey is a proven stalwart with decades of history. Although its cash-to-debt ratio is 0.08, its interest coverage is 11.09 and its Altman-Z score is 6.05, well out of the danger range.

The company has been paying dividends since 1972. It has a dividend yield of 2.02%, a payout ratio of 0.5 and a three-year growth rate of 7.2%, ranked higher than 53.46% of competitors. Its three-year average share buyback ratio is 1.5.

Hershey also has a history of not being affected much by periods of economic recession. The chart below shows the company's revenue and net income each year, with periods of economic recession in grey. As you can see, although net income suffered in 2002, revenue remained constant, and year-to-year net income was not harmed in the early 1990s or in 2008-09.

In conclusion, Hershey is a strong company with a history of profitability that is continuing to find new ways to grow. While the new acquisitions may hurt some metrics, such as the profit margin, they are not harming the profitability of the rest of the company, which is what is most important. The One Brands acquisition, in particular, seems to sync well with Hershey's overall company image. However, the current price-earnings ratio is 25.28, and the stock is now heavily overvalued like it has rarely been in the past, so I might prefer to wait for a better entry price.

Disclosure: Author owns no shares in any of the stocks mentioned.

Read more here:

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.

This article first appeared on GuruFocus.