Is Hon Kwok Land Investment Company (HKG:160) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Hon Kwok Land Investment Company, Limited (HKG:160) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Hon Kwok Land Investment Company

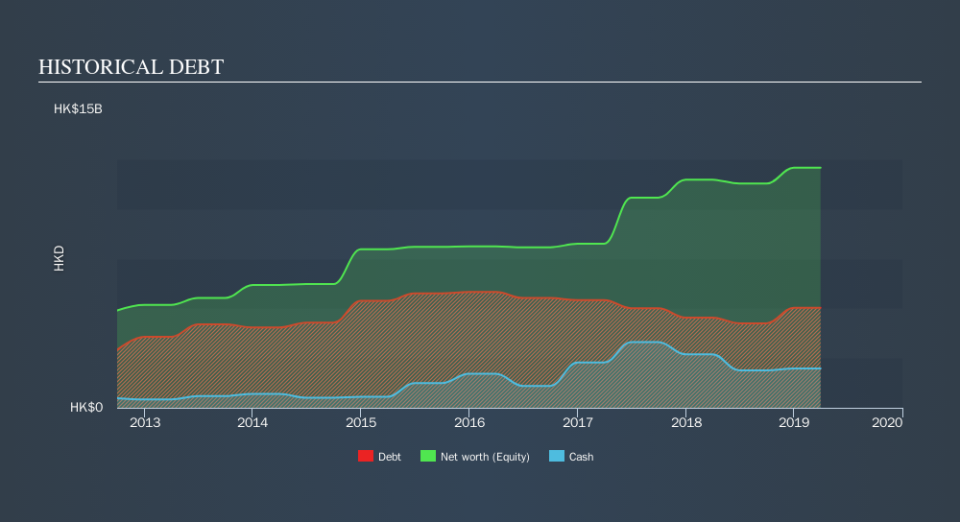

What Is Hon Kwok Land Investment Company's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Hon Kwok Land Investment Company had HK$5.03b of debt, an increase on HK$4.54b, over one year. However, it does have HK$1.97b in cash offsetting this, leading to net debt of about HK$3.06b.

How Healthy Is Hon Kwok Land Investment Company's Balance Sheet?

We can see from the most recent balance sheet that Hon Kwok Land Investment Company had liabilities of HK$2.00b falling due within a year, and liabilities of HK$5.47b due beyond that. On the other hand, it had cash of HK$1.97b and HK$105.0m worth of receivables due within a year. So it has liabilities totalling HK$5.39b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the HK$2.52b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Hon Kwok Land Investment Company would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Hon Kwok Land Investment Company has a debt to EBITDA ratio of 4.9 and its EBIT covered its interest expense 5.9 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Unfortunately, Hon Kwok Land Investment Company's EBIT flopped 17% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is Hon Kwok Land Investment Company's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Hon Kwok Land Investment Company reported free cash flow worth 5.2% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

On the face of it, Hon Kwok Land Investment Company's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to cover its interest expense with its EBIT isn't such a worry. Taking into account all the aforementioned factors, it looks like Hon Kwok Land Investment Company has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. Given Hon Kwok Land Investment Company has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.