Are Impresa - Sociedade Gestora de Participações Sociais, S.A.'s (ELI:IPR) Interest Costs Too High?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

While small-cap stocks, such as Impresa - Sociedade Gestora de Participações Sociais, S.A. (ELI:IPR) with its market cap of €40m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Assessing first and foremost the financial health is essential, as mismanagement of capital can lead to bankruptcies, which occur at a higher rate for small-caps. Let's work through some financial health checks you may wish to consider if you're interested in this stock. Nevertheless, potential investors would need to take a closer look, and I’d encourage you to dig deeper yourself into IPR here.

Does IPR Produce Much Cash Relative To Its Debt?

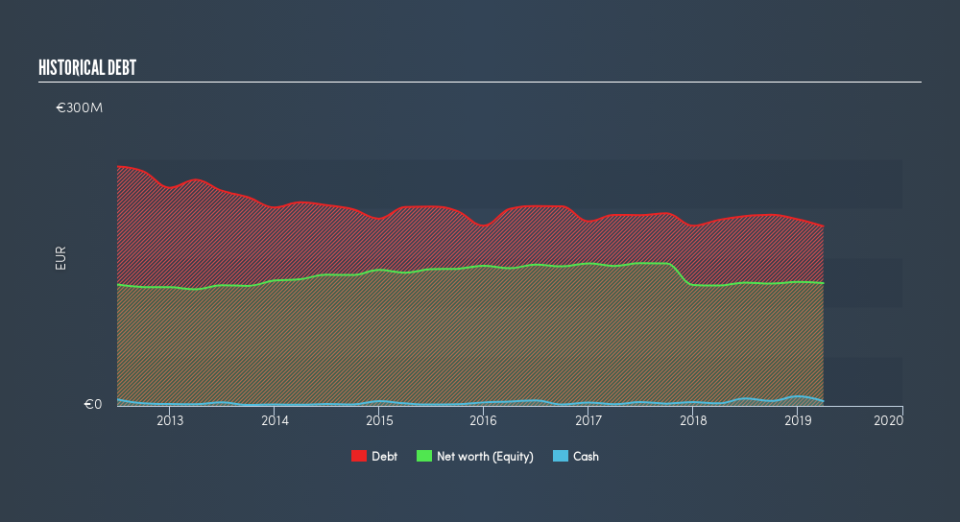

Over the past year, IPR has maintained its debt levels at around €182m including long-term debt. At this current level of debt, IPR's cash and short-term investments stands at €4.8m to keep the business going. Additionally, IPR has produced cash from operations of €23m during the same period of time, leading to an operating cash to total debt ratio of 13%, signalling that IPR’s debt is not covered by operating cash.

Can IPR meet its short-term obligations with the cash in hand?

At the current liabilities level of €159m, the company may not be able to easily meet these obligations given the level of current assets of €63m, with a current ratio of 0.39x. The current ratio is the number you get when you divide current assets by current liabilities.

Can IPR service its debt comfortably?

With total debt exceeding equity, IPR is considered a highly levered company. This is a bit unusual for a small-cap stock, since they generally have a harder time borrowing than large more established companies. We can check to see whether IPR is able to meet its debt obligations by looking at the net interest coverage ratio. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. In IPR's, case, the ratio of 2.24x suggests that interest is not strongly covered, which means that lenders may refuse to lend the company more money, as it is seen as too risky in terms of default.

Next Steps:

Although IPR’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet debt obligations which means its debt is being efficiently utilised. Though its low liquidity raises concerns over whether current asset management practices are properly implemented for the small-cap. Keep in mind I haven't considered other factors such as how IPR has been performing in the past. You should continue to research Impresa - Sociedade Gestora de Participações Sociais to get a more holistic view of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for IPR’s future growth? Take a look at our free research report of analyst consensus for IPR’s outlook.

Valuation: What is IPR worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether IPR is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.