Investors Who Bought Kopy Goldfields (STO:KOPY) Shares A Year Ago Are Now Down 36%

Kopy Goldfields AB (publ) (STO:KOPY) shareholders should be happy to see the share price up 13% in the last quarter. But that is minimal compensation for the share price under-performance over the last year. After all, the share price is down 36% in the last year, significantly under-performing the market.

See our latest analysis for Kopy Goldfields

Kopy Goldfields recorded just kr4,325,000 in revenue over the last twelve months, which isn't really enough for us to consider it to have a proven product. You have to wonder why venture capitalists aren't funding it. As a result, we think it's unlikely shareholders are paying much attention to current revenue, but rather speculating on growth in the years to come. It seems likely some shareholders believe that Kopy Goldfields will find or develop a valuable new mine before too long.

We think companies that have neither significant revenues nor profits are pretty high risk. There is usually a significant chance that they will need more money for business development, putting them at the mercy of capital markets. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies do very well over the long term, others become hyped up by promoters before eventually falling back down to earth, and going bankrupt (or being recapitalized).

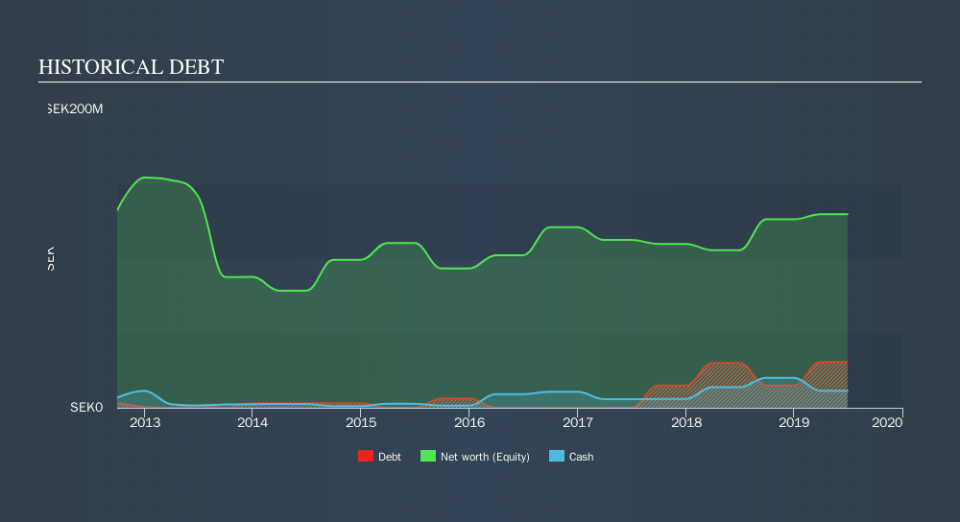

Kopy Goldfields had liabilities exceeding cash by kr22,416,000 when it last reported in June 2019, according to our data. That makes it extremely high risk, in our view. But with the share price diving 36% in the last year, it's probably fair to say that some shareholders no longer believe the company will succeed. The image below shows how Kopy Goldfields's balance sheet has changed over time; if you want to see the precise values, simply click on the image. You can click on the image below to see (in greater detail) how Kopy Goldfields's cash levels have changed over time.

Of course, the truth is that it is hard to value companies without much revenue or profit. Would it bother you if insiders were selling the stock? I would feel more nervous about the company if that were so. It only takes a moment for you to check whether we have identified any insider sales recently.

What about the Total Shareholder Return (TSR)?

We've already covered Kopy Goldfields's share price action, but we should also mention its total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Kopy Goldfields hasn't been paying dividends, but its TSR of -35% exceeds its share price return of -36%, implying it has either spun-off a business, or raised capital at a discount; thereby providing additional value to shareholders.

A Different Perspective

While the broader market gained around 7.1% in the last year, Kopy Goldfields shareholders lost 35%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Longer term investors wouldn't be so upset, since they would have made 5.0%, each year, over five years. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. If you would like to research Kopy Goldfields in more detail then you might want to take a look at whether insiders have been buying or selling shares in the company.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on SE exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.