Is IQE (LON:IQE) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, IQE plc (LON:IQE) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for IQE

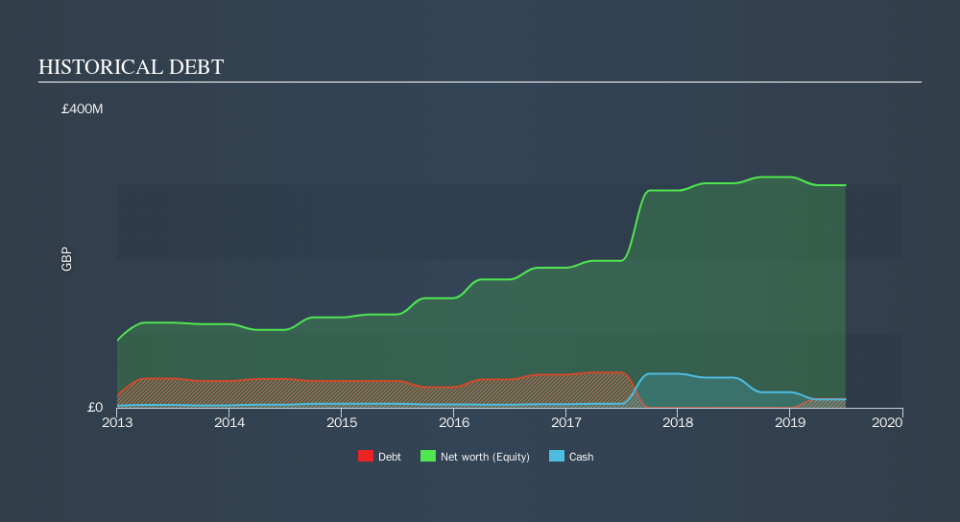

How Much Debt Does IQE Carry?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 IQE had UK£12.0m of debt, an increase on none, over one year. However, it also had UK£11.2m in cash, and so its net debt is UK£835.0k.

How Strong Is IQE's Balance Sheet?

We can see from the most recent balance sheet that IQE had liabilities of UK£47.2m falling due within a year, and liabilities of UK£58.4m due beyond that. On the other hand, it had cash of UK£11.2m and UK£37.9m worth of receivables due within a year. So it has liabilities totalling UK£56.5m more than its cash and near-term receivables, combined.

Given IQE has a market capitalization of UK£411.3m, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. But either way, IQE has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With debt at a measly 0.045 times EBITDA and EBIT covering interest a whopping 16.7 times, it's clear that IQE is not a desperate borrower. So relative to past earnings, the debt load seems trivial. In fact IQE's saving grace is its low debt levels, because its EBIT has tanked 50% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if IQE can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, IQE saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

While IQE's EBIT growth rate has us nervous. For example, its interest cover and net debt to EBITDA give us some confidence in its ability to manage its debt. Taking the abovementioned factors together we do think IQE's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. While IQE didn't make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away.Click here to see if its earnings are heading in the right direction, over the medium term.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.