Need To Know: Analysts Just Made A Substantial Cut To Their EHang Holdings Limited (NASDAQ:EH) Estimates

Today is shaping up negative for EHang Holdings Limited (NASDAQ:EH) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

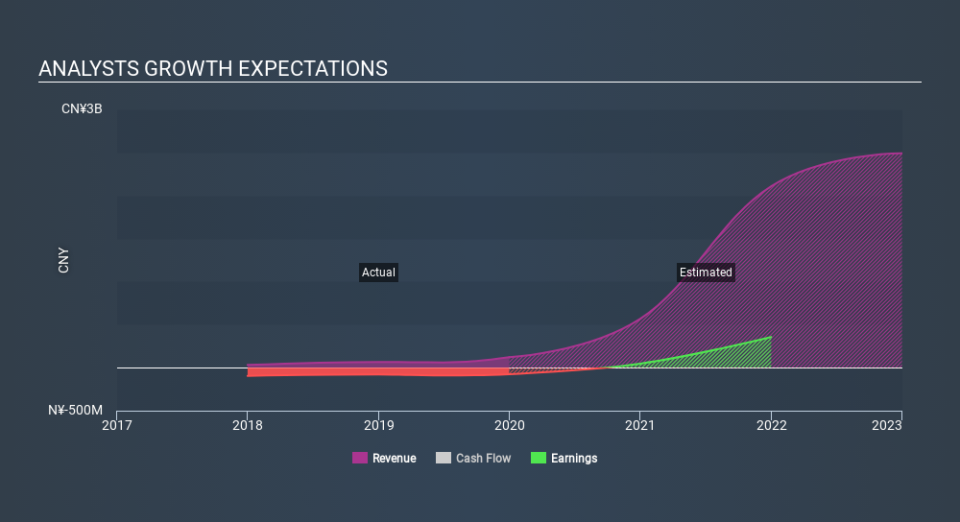

Following the downgrade, the most recent consensus for EHang Holdings from its two analysts is for revenues of CN¥568m in 2020 which, if met, would be a huge 366% increase on its sales over the past 12 months. Losses are expected to turn into profits real soon, with the analysts forecasting CN¥0.89 in per-share earnings CN¥0.89. Previously, the analysts had been modelling revenues of CN¥714m and earnings per share (EPS) of CN¥1.28 in 2020. Indeed, we can see that the analysts are a lot more bearish about EHang Holdings' prospects, administering a sizeable cut to revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for EHang Holdings

Analysts made no major changes to their price target of CN¥99.21, suggesting the downgrades are not expected to have a long-term impact on EHang Holdings'valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values EHang Holdings at CN¥99.54 per share, while the most bearish prices it at CN¥98.87. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that the analysts have a clear view on its prospects.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that EHang Holdings' rate of growth is expected to accelerate meaningfully, with the forecast 4x revenue growth noticeably faster than its historical growth of 83% over the past year. Compare this with other companies in the same industry, which are forecast to grow their revenue 4.9% next year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect EHang Holdings to grow faster than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for EHang Holdings. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on EHang Holdings after the downgrade.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At least one analyst has provided forecasts out to 2022, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.