What Is Lloyds Steels Industries's (NSE:LSIL) P/E Ratio After Its Share Price Rocketed?

Lloyds Steels Industries (NSE:LSIL) shares have had a really impressive month, gaining 33%, after some slippage. However, that doesn't change the fact that longer term shareholders might have been mercilessly wrecked by the 50% share price decline throughout the year.

Assuming no other changes, a sharply higher share price makes a stock less attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that deep value investors might steer clear when expectations of a company are too high. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

See our latest analysis for Lloyds Steels Industries

Does Lloyds Steels Industries Have A Relatively High Or Low P/E For Its Industry?

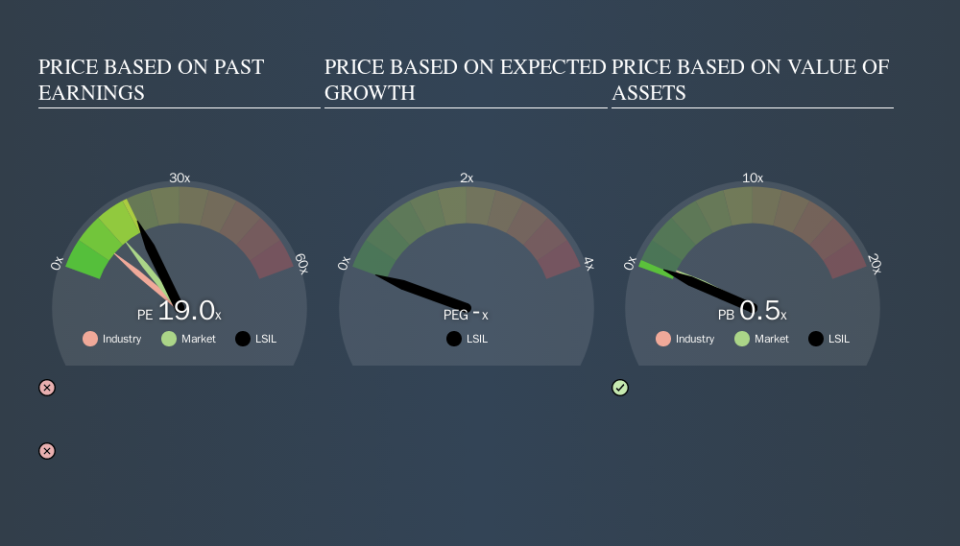

Lloyds Steels Industries's P/E of 18.95 indicates some degree of optimism towards the stock. The image below shows that Lloyds Steels Industries has a higher P/E than the average (8.5) P/E for companies in the metals and mining industry.

That means that the market expects Lloyds Steels Industries will outperform other companies in its industry. Shareholders are clearly optimistic, but the future is always uncertain. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. Earnings growth means that in the future the 'E' will be higher. That means even if the current P/E is high, it will reduce over time if the share price stays flat. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

Lloyds Steels Industries saw earnings per share decrease by 48% last year.

Remember: P/E Ratios Don't Consider The Balance Sheet

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. Thus, the metric does not reflect cash or debt held by the company. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Is Debt Impacting Lloyds Steels Industries's P/E?

With net cash of ₹224m, Lloyds Steels Industries has a very strong balance sheet, which may be important for its business. Having said that, at 44% of its market capitalization the cash hoard would contribute towards a higher P/E ratio.

The Verdict On Lloyds Steels Industries's P/E Ratio

Lloyds Steels Industries's P/E is 19.0 which is above average (13.3) in its market. Falling earnings per share is probably keeping traditional value investors away, but the net cash position means the company has time to improve: and the high P/E suggests the market thinks it will. What we know for sure is that investors have become more excited about Lloyds Steels Industries recently, since they have pushed its P/E ratio from 14.2 to 19.0 over the last month. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

Investors should be looking to buy stocks that the market is wrong about. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. Although we don't have analyst forecasts shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

But note: Lloyds Steels Industries may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.