A Look At Hi Sun Technology (China) Limited's (HKG:818) Exceptional Fundamentals

Attractive stocks have exceptional fundamentals. In the case of Hi Sun Technology (China) Limited (HKG:818), there's is a financially-sound company with a great track record of performance, trading at a great value. Below is a brief commentary on these key aspects. For those interested in understanding where the figures come from and want to see the analysis, take a look at the report on Hi Sun Technology (China) here.

Very undervalued with flawless balance sheet

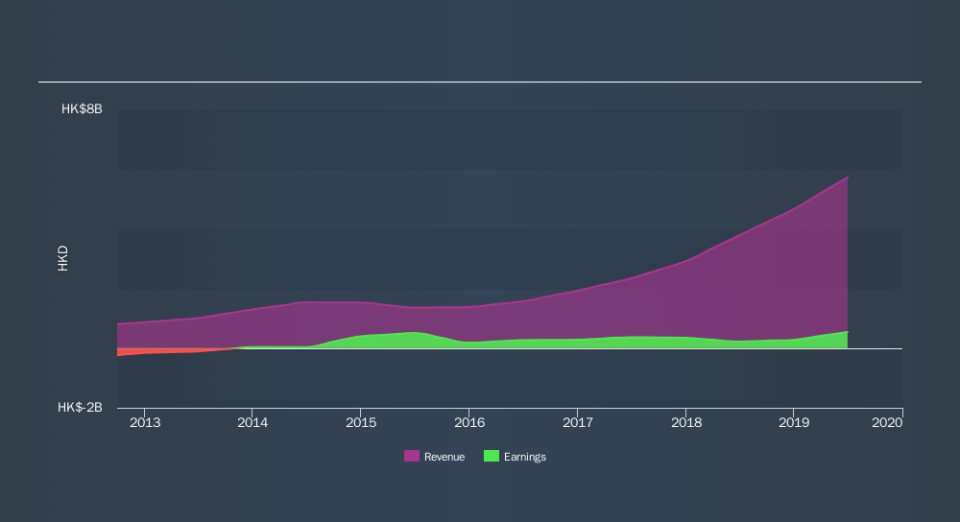

Over the past few years, 818 has more than doubled its earnings, with its most recent figure exceeding its annual average over the past five years. Not only did 818 outperformed its past performance, its growth also surpassed the IT industry expansion, which generated a -3.8% earnings growth. This is an notable feat for the company. 818's strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This implies that 818 manages its cash and cost levels well, which is a key determinant of the company’s health. 818 currently has no debt on its balance sheet. This implies that the company is running its operations purely on off equity funding. which is typically normal for a small-cap company. 818 has plenty of financial flexibility, without debt obligations to meet in the short term, as well as the headroom to raise debt should it need to in the future.

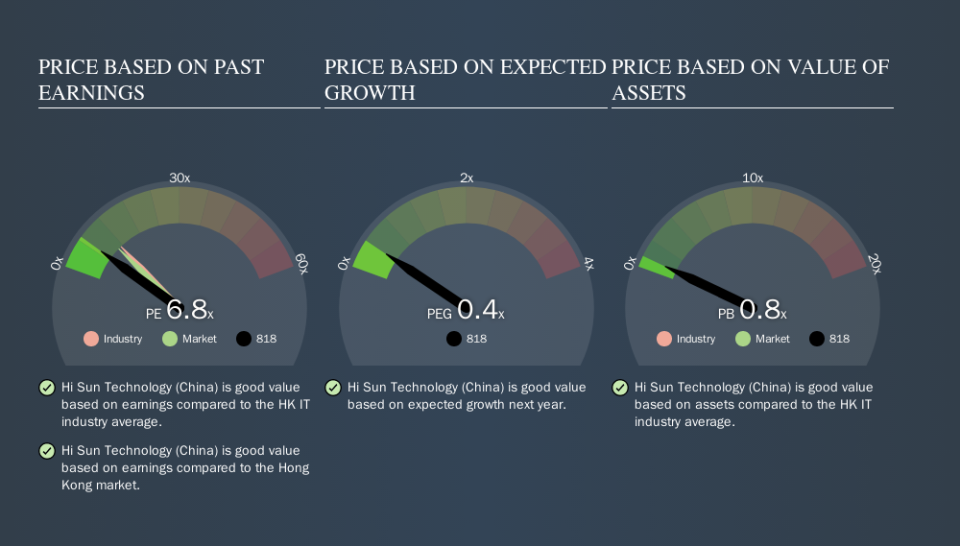

818's shares are now trading at a price below its true value based on its discounted cash flows, indicating a relatively pessimistic market sentiment. According to my intrinsic value of the stock, which is driven by analyst consensus forecast of 818's earnings, investors now have the opportunity to buy into the stock to reap capital gains. Also, relative to the rest of its peers with similar levels of earnings, 818's share price is trading below the group's average. This supports the theory that 818 is potentially underpriced.

Next Steps:

For Hi Sun Technology (China), I've put together three pertinent aspects you should further examine:

Future Outlook: What are well-informed industry analysts predicting for 818’s future growth? Take a look at our free research report of analyst consensus for 818’s outlook.

Dividend Income vs Capital Gains: Does 818 return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from 818 as an investment.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of 818? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.