Is Lucapa Diamond (ASX:LOM) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Lucapa Diamond Company Limited (ASX:LOM) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Lucapa Diamond

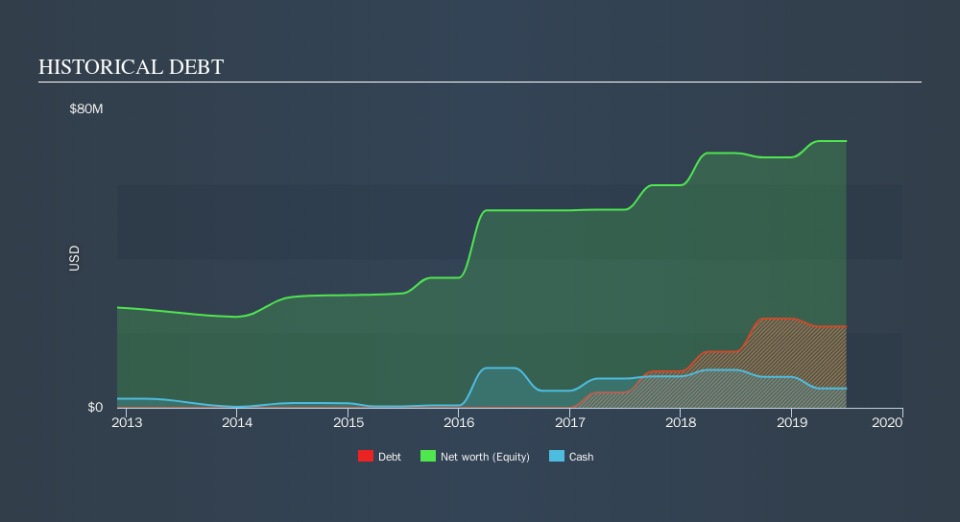

How Much Debt Does Lucapa Diamond Carry?

As you can see below, at the end of June 2019, Lucapa Diamond had US$21.8m of debt, up from US$15.1m a year ago. Click the image for more detail. However, it does have US$5.23m in cash offsetting this, leading to net debt of about US$16.6m.

How Strong Is Lucapa Diamond's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Lucapa Diamond had liabilities of US$17.7m due within 12 months and liabilities of US$10.1m due beyond that. Offsetting this, it had US$5.23m in cash and US$2.01m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$20.6m.

Lucapa Diamond has a market capitalization of US$51.3m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Lucapa Diamond's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

While it hasn't made a profit, at least Lucapa Diamond booked its first revenue as a publicly listed company, in the last twelve months.

Caveat Emptor

Importantly, Lucapa Diamond had negative earnings before interest and tax (EBIT), over the last year. To be specific the EBIT loss came in at US$3.3m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through US$15m of cash over the last year. So suffice it to say we consider the stock very risky. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Lucapa Diamond insider transactions.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.