The Market Sectors Showing Resilience As Earnings Estimates Slip

Note: The following is an excerpt from this week’s Earnings Trends report. You can access the full report that contains detailed historical actual and estimates for the current and following periods, please click here>>>

Here are the key points:

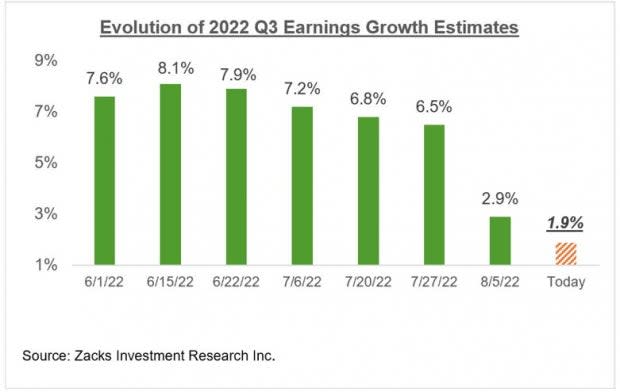

The +1.9% earnings growth expected for the S&P 500 index in 2022 Q3 is down from +7.2% at the start of the period. Excluding the Energy sector, Q3 earnings are expected to be down -4.5% at present, a significant decline from +2.1% in the beginning of July.

Q3 estimates have been cut for 13 of the 16 Zacks sectors since the quarter got underway, with the biggest declines at the Consumer Discretionary, Consumer Staples, Technology, Retail and Conglomerates sectors.

On the positive side, Q3 estimates have gone up the most for the Energy sector, but the revisions trend has been positive for the Auto and Utilities sectors as well.

The overall corporate profitability picture emerging from the Q2 earnings season, with over 90% of S&P 500 results out, continues to show stability and resilience in key earnings drivers like consumer and business spending.

While this stability and resilience run contrary to worries of an imminent economic slowdown or even a recession, we are starting to see tell-tale signs of emerging weakness in both consumer and business spending.

The market appreciated Walmart’s WMT results, but the favorable market reaction likely had more to do with fears created by its earlier pre-announcement. The inventory overhang at Walmart WMT, Target TGT and other retailers was mostly due to shifting consumer preferences. But part of the problem could be attributed to weakness in lower-income households as a result of inflationary pressures.

It makes intuitive sense for this consumer segment to be feeling some squeeze, as we heard from companies in a variety of industries, including AT&T T. Other households seem to be doing just fine, as we heard from banks, credit card operators and beyond.

With respect to business spending, we have started seeing a squeeze on advertising budgets and hiring plans, but Microsoft MSFT and others didn’t see anything disconcerting with respect to spending on software and other services. That said, it is reasonable to expect some moderation in demand trends going forward as the full extent of the Fed’s tightening cycle permeates through the broader economy.

A slowdown has gotten underway, but there is nothing in the earnings data, management commentary or guidance that would suggest the U.S. economy heading into a major economic downturn. That said, estimates have started coming down, with the overall revisions trend turning negative even after accounting for the persistent favorable revisions trend enjoyed by the Energy sector.

You can see this in the revisions trend to Q3 estimates in the chart below.

Image Source: Zacks Investment Research

If we look at the evolution of Q3 earnings growth expectations on an ex-Energy basis, the expected growth rate has dropped from +2.1% on July 6th to -4.5% today.

The chart below shows the expected aggregate total earnings for full-year 2023 have evolved on an ex-Energy basis.

Image Source: Zacks Investment Research

As you can see above, aggregate S&P 500 earnings outside of the Energy sector have declined -3.4% since mid-April, with double-digit percentage declines in Retail (down -14.6%) and Construction (-10.8%), and high single-digit percentage declines for the Tech (-9.7%), Industrial Products (-8.8%) and Consumer Discretionary (-7%).

The Overall Earnings Picture

Beyond Q2, the growth picture is expected to modestly improve, as you can see in the chart below that provides a big-picture view of earnings on a quarterly basis.

Image Source: Zacks Investment Research

The chart below shows the overall earnings picture on an annual basis, with the growth momentum expected to continue.

Image Source: Zacks Investment Research

As strong as the full-year 2022 earnings growth picture is expected to be, it’s worth remembering that a big part of it is due to the unprecedented Energy sector momentum. Excluding the Energy sector, full-year 2022 earnings growth for the remainder of the index drops to a -0.1% decline.

There is a rising degree of uncertainty about the outlook, reflecting a lack of macroeconomic visibility in a backdrop of Fed monetary policy tightening. The evolving earnings revisions trend will reflect this macro backdrop.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AT&T Inc. (T) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research