Shares in Aggreko, one of the top global suppliers of portable power generators, surged after the group reportedly received takeover interest from a second potential suitor.

US private equity group Platinum Equity has approached the FTSE 250 group over a potential buyout, even as the deadline for a rival buyout consortium to make a firm offer looms, Bloomberg reported.

It said Platinum had expressed interest in a acquiring the company, which has supplied generators to events such as the London Olympics.

Sources close to Aggreko said progress has been made in its negotiations with a consortium backed by TDR Capital and I Square ahead of today’s deadline for a firm offer to be made. The company declined to comment, however, on the report of another approach.

On Monday, Aggreko posted full-year results that met City expectations. Its shares rose 66p to 889p as investors hoped the reports may herald a bidding war.

London-listed stocks had a poor session overall, with the FTSE 250 dropping having closed near a one-year high in the wake of Wednesday’s Budget, and the FTSE 100 dipping amid concerns over a global rebound in inflation.

IT group Sage led FTSE 100 risers, climbing 17.6p to 597p after announcing it will begin a share buyback programme of up to £300m, which will run until early September at the latest.

The group previously scrapped a £250m buyback programme last April in the face of the pandemic. Only £6m of purchases had been completed before the programme was frozen. Stifel’s George O’Connor said the plans signal “that better times lie ahead”.

Hot on its heels was Reckitt Benckiser, which climbed 182p to £62.82 following a double upgrade from analysts at Societe Generale, who said the consumer goods giant offered a “more attractive risk/reward opportunity” at its current valuation.

Miners put a drag on the blue-chip index as rising bond yields rekindled nerves across the markets. Rio Tinto sold off particularly hard, dropping 491.2p to £58.78 as its shares traded without their dividend. On Wednesday, Simon Thompson, its chairman, announced plans to step down following the blasting scandal last year that destroyed two ancient Aboriginal sites in Australia.

Among mid-caps, housebuilder Vistry rose 32p to 943p. The group stored its dividend despite a fall in profits after reporting a slight increase in annual revenues.

Molten metal flow company Vesuvius dropped 42p to 509p after reporting a fall in profit and revenue for 2020. The steel and foundry specialist said it had been hit by the pandemic, but forecasts an improved performance during the year ahead.

06:19 PM

Wrapping up

That is all from us today! Thank you for reading along.

Here are some of our top stories so far. As always, stay tuned on the Business page for more:

Have a great evening - Louis will be back in the morning to finish the week off.

What to expect tomorrow (among more):

Updates from: ConvaTec, Essentra, London Stock Exchange Group

Numbers on: Halifax house price index (UK), manufacturing orders (Germany), non-farm payrolls (US)

06:12 PM

US stocks slump on Powell comments

US stocks are slumping, having opened higher, with the S&P 500 dropping towards the lowest in almost five weeks.

It comes as Fed chairman Jerome Powell refrained from pushing back more forcefully against the recent spike in treasury yields.

He said the surge caught his attention and that disorderly market moves would be unwelcome, but added that the central bank is still a "long way" from achieving its goals as he sees a "lot of ground to cover before tightening".

05:48 PM

Insurer Admiral braces for more accidents

Oxford Circus

Insurer Admiral is bracing for a surge in road accidents as lockdown lifts and people return to the roads, saying it expects the frequency of claims “to return to more normal levels” when compared to last year.

It posted a 20pc jump in pre-tax profits in 2020, to £608.2m, after reduced car travel amid the pandemic - particularly in the first lockdown - led to claims volumes falling. Net revenue gained 8pc to £1.31bn, as it reported a 10pc rise in customer numbers.

As lockdowns lift and car journeys resume, Admiral expects an uptick of claims.

Chief financial officer Geraint Jones said: “We expect the 2021 loss ratio will be higher than 2020, as claims frequency is very likely to return towards more normal levels".

The FTSE 100 firm confirmed a 12pc hike in its full dividend to 156.5p, giving founder Henry Englehardt a payout worth around £44m.

Admiral also said it paid out £110m to UK motor insurance customers last year as part of a "Stay at Home" refund. Shares, however, dropped 2.7pc to £30.63.

05:22 PM

Marriott to give money to workers who get jabs

marriott

Marriott International, the world’s largest lodging company, is offering a financial incentive to hotel workers who receive Covid vaccines, reported Bloomberg.

The company will provide the equivalent of four hours pay to employees at hotels it manages in the US and Canada once the workers have completed the vaccination course, according to a statement.

Marriott said it views the distribution of vaccines to travelers and hospitality workers as a key driver of an economic recovery. While it is strongly encouraging employees to get vaccinated, it is not mandating the shots.

Separately, the hotel giant opened a new hotel in central Birmingham on Wednesday. Aloft Birmingham Eastside - part of the Marriott International Group - launched as the fourth of its brand in the UK, as part of a conference centre development.

04:55 PM

Crash in bookmaker William Hill's profits

William Hill

William Hill’s full-year profits crashed 91pc last year after the pandemic forced the closure of its betting shops.

My colleague Simon Foy reports:

The FTSE 250 bookmaker, which is being bought by US casino giant Caesars Group, posted adjusted pre-tax profits of just £9.1m, down from £96.5m in 2019.

Its retail arm plunged to a £29.5m loss with like-for-like sales falling 30pc, however its online business was boosted by more punters placing bets from home, with online net revenues rising 9pc.

Chief executive Ulrik Bengtsson said the group’s betting shops will reopen alongside non-essential retailers on April 12, adding that he expects a swift recovery.

However, the company warned that the risk of a regulatory crackdown “remains ever-present in Europe and the UK”. The Government launched the Gambling Act review at the end of last year, in what is expected to be the biggest shake-up of the online gambling sector.

Mr Bengtsson said tighter regulation is “clearly one of the most important things for the industry to navigate through during 2021”.

04:38 PM

Capco bought out for $1.45bn

Indian software exporter Wipro has agreed to buy British consultancy firm Capco for $1.45bn (£1bn) as it looks to win customers in Europe and Asia.

The New York-listed firm said it expects the deal to close by the end of June.

London-headquartered Capco - which has 5,000 consultants - will help Wipro add banking, insurance and financial services clients.

It comes less than a year after Bangalore-based Wipro hired Thierry Delaporte from Capgemini to boost the company against rivals like HCL Technologies and Infosys. Wipro has over 180,000 staff across six continents.

04:17 PM

Oil prices jump as Opec chooses not to increase output

Oil prices have soared in recent minutes after Opec and its allies decided not to cut output next month.

Bloomberg has more details:

The cartel had been debating whether to restore as much as 1.5m barrels a day of production, but after being urged to “keep our powder dry” by Saudi Arabia delegates said they decided to hold output steady at current levels. Brent crude rose 5pc in London.

The decision is a victory for the Gulf kingdom, which has consistently pushed for tighter production restraints. It leaves the world facing a significant supply squeeze and higher energy costs just as widespread vaccination allows economies to start emerging from the downturn caused by the pandemic.

04:15 PM

Management shifts at Shell

Shell’s UK country chair Sinead Lynch has been promoted to global head of low-carbon fuels as the company adapts to the shift away from fossil fuels.

My colleague Rachel Millard reports:

Ms Lynch will be replaced by David Bunch, currently in charge of Shell’s retail business in Europe and South Africa, according to Reuters which first reported the changes.

Meanwhile, Simon Roddy, who currently has a senior role in Shell’s Nigerian operations, will take over running its North Sea operations from Steve Phimister, whose new role in the company has yet to be announced.

Lynch joined Shell in 2016 and sits on the UK government’s Hydrogen Advisory Council.

03:57 PM

Full report: US suspends tariffs on British exports

My colleagues Alan Tovey and Ben Riley-Smith have a full report on the US’s decision to suspend tariffs on UK goods that were imposed in the fallout from a long-running battle between America and the EU over illegal state aid for aircraft makers. They write:

Products sold to America were affected by the World Trade Organisation-sanctioned tariffs announced two years ago, as former President Donald Trump sought to protect domestic manufacturers such as Boeing.

The tariffs were imposed after the WTO ruled that both aerospace companies had received state support that broke international rules - the culmination of a 16-year feud between Airbus and Boeing fought by proxy through their governments.

To offset the harm, both the EU and US were allowed to slap tariffs totalling $12bn on a wide range of imports and not those in the aerospace sector alone.

Former Bank of England Governor Mark Carney has finally weighed on an FT Alphaville report which noted his name in among those on a blacklist compiled by holiday park Pontins.

The existence of the list was revealed on Tuesday by the i paper, which reported:

An investigation by the Equality and Human Rights Commission (EHRC) found that the company had been using the blacklist of mainly Irish surnames as part of a policy of refusing bookings by Gypsies and Travellers to its holiday parks.

The list, seen by i, was uploaded to the Pontins intranet under the heading “Undesirable Guests”, instructing call handlers that people using these names were “unwelcome”.

03:17 PM

Those US jobless claims numbers…

Slightly late (apologies, technical issues at my end), but here are the US jobless claims numbers for last week, showing claims rose slightly to 745,000, compared to a revised 736,000 in the previous week.

02:58 PM

Full report: Sunak’s post-pandemic spending plans are ‘implausibly low’, warns IFS

My colleague Tim Wallace has a full report on the IFS' budget warning. He writes:

Rishi Sunak could be forced to hike borrowing or taxes as analysts warned his spending plans for the post-Covid era look “implausibly low”.

The Chancellor's Budget has pencilled in a £17bn cut to public services compared to pre-pandemic plans, which the Institute for Fiscal Studies says is unlikely to be realistic given pressures on the NHS, social care and transport.

“I may be proved wrong, but I’d offer 10 to one against that happening,” said Paul Johnson, director at the IFS. He anticipates more pressure to spend on the NHS and other areas.

“The NHS is perhaps the most obvious. Further top-ups seem near-inevitable. Catching up on lost learning in schools, dealing with the backlog in our courts system, supporting public transport providers, and fixing our system for social care funding would all require additional spending. The Chancellor’s medium-term spending plans simply look implausibly low.”

Richard Hughes, head of the Office for Budget Responsibility, said “it is not entirely clear the rescue phase is over” when it comes to Government spending, meaning pressures are already building.

“There is an overhang of potential legacy costs, which this Government is going to have to incur,” he said.

“Delayed activity, postponed operations in the health service, students who have missed out on up to six months of schooling, a transport system which is now back in public ownership with its fare box being filled by the Treasury every month and where passenger numbers may not recover to pre-pandemic levels for months if not year

“At the moment the Government doesn’t really have a plan for that.”

US stocks opened higher after data showed that jobless claims came in slightly below estimates.

S&P 500 +0.3pc

Dow Jones +0.3pc

Nasdaq +0.3pc

02:15 PM

Platinum approaches Aggreko as TDR talks progress, according to reports

Aggreko

Aggreko, one of the world’s largest suppliers of portable power generators, has been approached by another suitor about a potential takeover, according to reports.

Bloomberg has the details:

Platinum Equity has approached Aggreko about a potential takeover, as a deadline looms for a rival buyout consortium to make a firm offer, people with knowledge of the matter said.

Platinum expressed interest in a potential acquisition of London-listed Aggreko, according to the people, who asked not to be identified because the information is private.

Aggreko’s negotiations with a consortium backed by TDR Capital and I Squared have been progressing ahead of their Friday deadline to submit a firm offer, the people said.

Representatives for Aggreko and TDR couldn’t immediately comment.

01:59 PM

Ocado to refund customers for plastic bag returns

Ocado - Hollie Adams/Bloomberg

Ocado will refund 5p per plastic bag returned by customers as the online retailer restarts its recycling scheme.

My colleague Simon Foy reports:

From next Monday, up to 99 unwanted grey bags can be collected by an Ocado driver during a delivery as part of a contact-free exchange.

Customers will have to place their unwanted carrier bags into a single bag and let the driver know how many Ocado bags are being handed back so a refund can be arranged.

Since last summer, Ocado shoppers have been charged up to 5p per bag as part of their delivery, but they will now be able to reclaim this charge.

Government’s Help to Grow scheme draws strong interest

Over 1,000 small businesses registered an interest in the Government’s Help to Grow: Management scheme within half an hour of its announcement.

The management programme for small- and medium-sized business, announced during yesterday’s Budget, will offer 30,000 bosses and managers to receive training.

The scheme has received £220m in funding from the Government, which will cover 90pc of the cost for attendees. Running for 12 weeks, the programme will be led by experts from the country’s top business schools.

Anne Kiem, chief executive of the Chartered Institution of Business Schools, said:

This represents a fantastic opportunity for the nation’s small businesses to experience the first class practical support on offer in the UK’s business schools. Through evidence-informed business and management education, this timely initiative will help small business leaders to drive their businesses towards growth and give the economy, and the millions employed within it, a much-needed boost.

01:21 PM

Wall Street set to extend losses at open

With just over an hour until the US open, futures trading is pointing towards a continued dip across the main US indices.

The S&P 500 is set to extend yesterday’s fall, dropping 0.2pc, while the tech-heavy Nasdaq will fall 0.3pc on current trends.

01:07 PM

New cars sales plunge

Sales of new cars plunged to levels not seen since 1959 in February as coronavirus lockdowns continued to ravage Britain’s automotive industry.

My colleague Alan Tovey reports:

However, with January lockdowns forcing showrooms to shut and dealers going online to make sales, demand has collapsed. reports:

Just 51,312 new cars were registered last month according to data from the Society of Motor Manufacturers and Traders (SMMT) – a 35.5pc decline that equated to 28,282 fewer cars than in February last year.

February is traditionally a quiet month for the car industry as it comes ahead of the new registration plate in March.

Motorists keen to have the latest car on their drives mean March is normally the busiest time for dealers, accounting for a fifth of all new vehicle sales each year.

However, with January lockdowns forcing showrooms to shut and dealers going online to make sales, demand has collapsed.

OBR chair: Government has kicked the can down the road on several fronts

Office for Budget Responsibility chair Richard Hughes has been speaking to Sky News. He’s noted that the Government is going to face several difficult spending decision in the Autumn, including on topics such as catch-up schooling and further vaccination programmes. Watch below:

"The govt has set itself up for an even tougher spending review this Autumn."

Oil prices have dipped as Opec officials gather to decide whether increase crude output.

My colleague Rachel Millard reports:

Brent Crude fell 0.7pc to $63.48, while US oil was down 0.8pc to $60.63 on Thursday morning.

The Opec+ alliance that includes the Opec cartel as well as other oil producers agreed to hold production steady in January while Saudi Arabia cut its own production by 1m barrels per day.

The move helped maintain prices despite the prolonged subdued demand due to coronavirus, and they have climbed back to pre-pandemic levels after starting the year at $50.

Analysts have predicted Saudi Arabia will reverse its own cut at Thursday’s meeting, to be held via videolink, while other producers will be allowed to increase their production by 500,000 barrels per day.

US to suspend tariffs on UK products linked to Airbus–Boeing dispute

The US plans to suspend retaliatory tariffs slapped on UK products that have been caught in the long-running dispute over state aid to Boeing and Airbus.

Bloomberg has more details:

The tariff suspension will last four months to “focus on negotiating a balanced settlement to the disputes”, the UK government said in a statement on Thursday. The decision means goods like Scotch whisky, biscuits and clotted cream can be imported to the US from Britain without being subject to an additional 25pc duty.

Removing tariffs on UK-US commerce has been a priority for Prime Minister Boris Johnson’s government as they seek a broader trade deal with President Joe Biden’s administration. Britain unilaterally dropped tariffs on some US products indefinitely in January in a bid to reduce trade tensions. The former Trump administration did not reciprocate the UK’s concession.

11:47 AM

European retail sales dived in January

Retail sales in the eurozone plunged during January, with much of the bloc back under the tightest Covid-19 restrictions.

Here’s how sales volumes have shifted – from a sharply recovery to a steady unravelling over recent months.

Capital Economics’ Melania Debono said:

January’s data show that euro-zone retail sales fell very sharply at the start of this year, despite the strength of online sales. As lockdowns have been extended in many economies and daily virus cases are creeping up, shops may remain closed into Q2, keeping retail sales subdued for a while yet.

11:41 AM

FCA fines former Stifel trader for market abuse

The Financial Conduct Authority has fined a former Stifel trader £52,000 for market abuse, according to a statement.

The City watchdog said Adrian Horn, previously a trader at Stifel Nicolaus Europe, has also been prohibited from performing any function in relation to regulated activity.

Mr Horn received a 30pc discount to the possibly fine of £75,000 for complying with the regulator’s procedures.

The FCA said Mr Horn, an “experienced trader”, undertook a practice known as “wash trading”, in whihc he he placed buy order in McKay, a commercial property investment company, that traded with his existing sell orders.

It said Mr Horn conducted 129 wash orders between July 20218 and May 2019, doing so in such as way as to avoid detection:

As part of this strategy, Mr Horn would check to see how many McKay shares had traded before the market closed and, if the volume traded was below 13,000, would make up the shortfall by executing wash trades with himself

The FCA added:

This market manipulation was serious and directly undermined the integrity of the market. As well as creating a false volume in McKay shares, it was intended to falsely keep McKay in the FTSE All Share Index. Mr Horn’s conduct was intentional and repeated.

11:33 AM

IFS event rounds up

After some questions (and an apology from Paul Johnson, who whose request that Stuart Adam move through his presentation more quickly was picked up on a hot mic), the IFS’s event is finished.

The think tank’s researchers have reached some mixed conclusions, with a general sense that Rishi Sunak has created problems further down the line with his Budget approach.

11:26 AM

Full report: Aviva profits steady as it exit Italy

My colleague Simon Foy has a full report on Aviva’s exit from Italy, as well as the group’s full-year results. He writes:

The selling spree is part of chief executive Amanda Blanc's strategy to focus the insurer's operations on its more profitable regions.

It came as Aviva’s operating profits remained stable at £3.18bn last year. However, pre-tax profits fell by nearly a third to £2.61bn. It declared a total dividend for 2020 of 21p, compared to 15.5p a year earlier.

In the UK, the company's savings and retirement business posted a £1bn jump in net flows to a record £8.5bn.

IFS researcher Stuart Adam has raised some questions about the Chancellor’s new ‘Super Deduction’ scheme, in which companies will be able to deduct 130pc of the cost of some plant and machinery investment from taxable profits.

He says that the policy, which will last for the next two fiscal years, could strongly encourage investment over those years – but with caveats.

He notes that although this should be an “effective short-term fiscal stimulus”, but warned:

There could be an investment ‘hangover’ afterwards

It could encourage ‘bad’ investments that would otherwise be unviable

There would be a bias towards investment in plants and machinery instead of (e.g.) buildings or intangibles

There is a risk of tax avoidance or fraud

More fun facts from Mr Johnson:

Freezing things for a long time makes a big difference. Since 2010 there has been a doubling of the number of people, to almost 500,000, paying the additional 45% rate of income tax. That's because it has kicked in at £150k for that whole period.

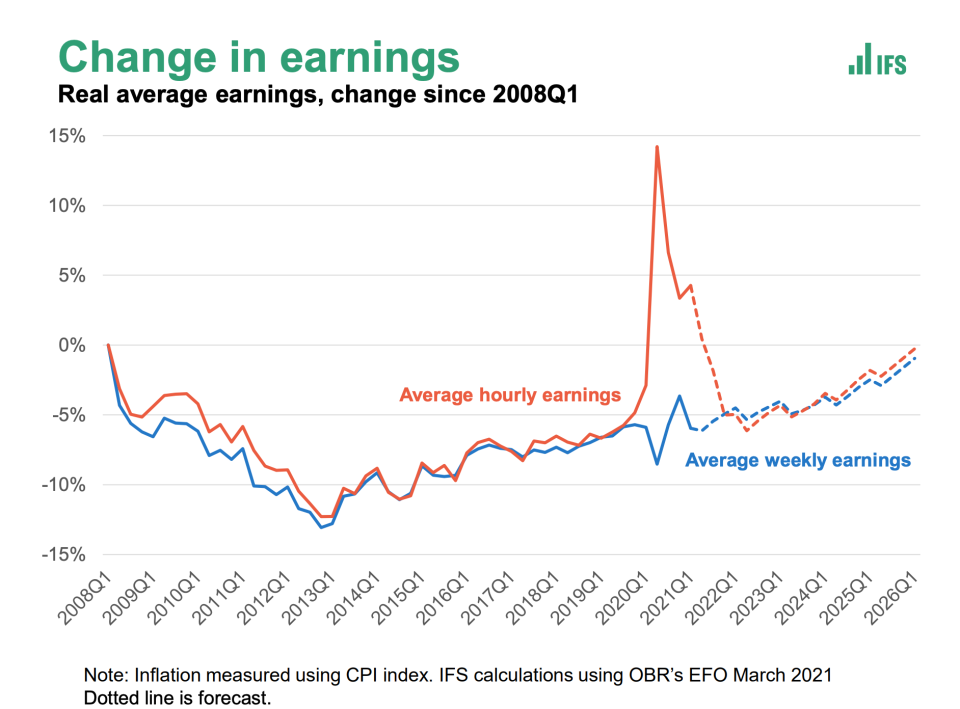

Average earnings will still be below pre-financial crisis levels in 2026

Looking at the OBR’s projections for real-term average earnings, Mr Water notes that real weekly and hourly earnings will STILL be below pre-financial crisis levels at the end of the forecast period – 18 years without breaking that threshold.

IFS - IFS

10:45 AM

Further extensions to UC lift would not be a surprise

IFS researcher Tom Waters, who is discussing the impact of the Budget on household finances, echoes Paul Johnson in saying a further extension of the £20 a week Universal Credit uplift beyond September now look fairly likely.

He notes that a further 2.5m people on out-of-work pre-UC benefits have not seen an increase in their benefits during the pandemic – with most of this group unable to work for health reasons.

On UC, he says: “Further extensions would not be a complete surprise”.

10:36 AM

Further tax-raising measures may come

Concluding, Mr Emmerson says the outlook for tax receipts is now “hugely uncertain”, and says that interest rate rises could be “painful” for the Treasury.

10:32 AM

Higher inflation could add £7bn to debt interest

IFS researcher Carl Emmerson is analysing the Budget’s effects on the public finances. He notes the potential impact a rise in interest rates could have on UK debt over the coming years.

He says levels of quantitative easing mean that debt is effectively finances at the Bank of England’s main bank rate, which is currently at a record low of 0.1pc.

Mr Emmerson says the OBR based its forecast for the bank rate on market expectations as of February 5th, when it stood at 0.5pc for the end of 2026. Since then, however, expectations have risen to 0.8pc.

He says this level of an increase to all interest rates would add £7bn to the UK’s total debt interesting – noting that big an expected jump has happened in just four weeks.

It wouldn’t all be bad, however, he notes:

Higher interest rates could be associated with stronger outlook for receipts, which overall would be good for the public finances.

10:24 AM

Lufthansa to shrink in wake of record loss

Lufthansa - Sean Gallup/Getty Images

Lufthansa is planning to ground more jets after the German flag-carrier reported a record €6.7bn (£5.8bn) loss in the wake of the collapse in air travel caused by coronavirus.

My colleague Alan Tovey reports:

Europe's largest airline group is likely to emerge form the pandemic smaller, executives said, as they said older planes will be retired.

Announcing the dire annual results, chief executive Carsten Spohr said Lufthansa was “examining whether all aircraft older than 25 years will remain on the ground permanently”.

The company reported annual revenues of €13.6bn, down 63pc on the previous year.

To battle the impact of Covid, the airline is shedding a fifth of its staff, taking headcount down to 110,000, with a further 10,000 jobs or their equivalent in wages costs to go.

The UK’s competition watchdog has launched an investigation into Apple over the terms and conditions the iPhone-maker makes its app developers agree to.

The Competition & Markets Authority said:

All apps available through the App Store have to be approved by Apple, with this approval hinging on developers agreeing to certain terms. The complaints from developers focus on the terms that mean they can only distribute their apps to iPhones and iPads via the App Store.

These complaints also highlight that certain developers who offer ‘in-app’ features, add-ons or upgrades are required to use Apple’s payment system, rather than an alternative system. Apple charges a commission of up to 30pc to developers on the value of these transactions or any time a consumer buys their app.

The CMA’s investigation will consider whether Apple has a dominant position in connection with the distribution of apps on Apple devices in the UK – and, if so, whether Apple imposes unfair or anti-competitive terms on developers using the App Store, ultimately resulting in users having less choice or paying higher prices for apps and add-ons.

Andrea Coscelli, the CMA’s chief executive, said:

Millions of us use apps every day to check the weather, play a game or order a takeaway. So, complaints that Apple is using its market position to set terms which are unfair or may restrict competition and choice – potentially causing customers to lose out when buying and using apps – warrant careful scrutiny.

10:16 AM

Spending plans ‘don’t look deliverable’

Mr Johnson wraps up with some pretty damning commentary. He says Mr Sunak has been generous in the short term, but that the Chancellor’s medium-term goals “don’t look deliverable”, and said the Chancellor has been “silent” on the UK’s longer-term path towards economic recovery:

Mr Sunak had three challenges in this budget: to ensure the right level of support for the economy over the next few months, to set about fixing the longer-term public finances, and to deal with the longer term consequences of the pandemic, especially its unequal consequences.

He has done a decent job of the first – arguably erring on the side of generosity.

He has given us a sense of where he wants to go on the second, but he still has a lot of work to do and his spending plans in particular don’t look deliverable – at least not without considerable pain.

On the third he has been silent. No money to deal with post-pandemic priorities. No policies to deal with the inequalities that have opened up over the last year between rich and poor, old and young, more and less well–educated.

This is a big hole in the chancellor’s and the government’s policies, a hole which needs to be filled and soon if we are not to suffer a much worse hangover from this crisis than need be the case.

10:14 AM

Sunak ‘taking a gamble’ on corporation tax

Mr Johnson draws a distinction between the UK’s actual corporation tax rate (low by international standards), and its effective rate (more middling). The IFS director says:

Our corporation tax take is certainly healthy. With this increase Mr Sunak is taking a gamble that raising corporate taxes further up the international pecking order won’t have too terrible an effect on investment.

10:12 AM

Spending plans look ‘implausibly low’

More doubts from Mr Johnson over how possible it will be for the Treasury to meet the spending expectations set out yesterday. He says Mr Sunak painted a picture of predictable spending shifts and shrugged off a new £4bn cut to public spending:

In reality, there will be pressures from all sorts of directions. The NHS is perhaps the most obvious. Further top-ups seem near-inevitable. Catching up on lost learning in schools, dealing with the backlog in our courts system, supporting public transport providers, and fixing our system for social care funding would all require additional spending. The Chancellor’s medium-term spending plans simply look implausibly low.

10:10 AM

Sustained Universal Credit uplift would cost £6bn a year

Mr Johnson says Universal Credit is one of the most uncertain parts of the spending plans. The Chancellor said a £20 a week extension to the support for the poorest families would be extended to the end of September. Mr Johnson said:

If it doesn’t – and the pressure will mount to keep it – then that adds over £6 billion to spending each year going forward.

It is, by the way, remarkable that while the Chancellor felt the need for a gradual phase out of furlough, business rates support, stamp duty reductions and VAT reductions he is still set on a cliff edge reduction in UC such that incomes of some of the poorest families will fall by over £80 between one month and the next. Whatever the case for cutting generosity into the longer term, if you’re going to do so the case for doing it gradually rather than all at once looks unanswerable.

Claimant levels have jumped sharply during the pandemic:

10:07 AM

‘50–50 chance’ of further concessions on corporation tax

Mr Sunak’s plans for a corporation tax hike came with a number of caveats and exemptions. Mr Johnson reckons there’s a high chance that the Treasury will soften its stance further, saying:

Whether that rise in the corporation tax will actually be delivered without additional concessions we will wait and see. I reckon 50-50 at best. Even if it does, as the OBR expects, raise £17bn in 2025-26, it will raise less over the long run.

10:05 AM

Unemployment peak at 6.5pc would be ‘remarkable triumph’

Reflecting the Office for Budget Responsibility’s latest set of unemployment forecasts, Mr Johnson says that an unemployment peak of “only” 6.5pc at the end of the year would represent a “remarkable triumph”.

10:02 AM

IFS verdict: Watch live

You can watch the IFS event here. Paul Johnson’s speaking first, and then IFS researchers will speak on a the other key areas.

10:01 AM

IFS verdict: Key highlights

As the IFS’s event gets underway, here are some highlights from director Paul Johnson’s opening remarks, which were sent out in advance (slides and further comment to come).

The big picture

This was of course a tale of two budgets. By the end of the forecast period we are looking at a fiscal tightening of over £30 billion relative to previous plans. Take account of the cuts to planned spending announced in the Autumn and Santa Sunak, purveyor of billions today looks more like Scrooge Sunak cutting spending and raising taxes to the tune of nearly £50 billion relative to his pre-pandemic plans of March 2020.

That’s mostly a result of two big tax increases, both screeching U turns on Conservative policy over the last decade. The long term freezes in various tax allowances and thresholds raise £9 billion or so, mostly from the freeze in the income tax personal allowance. The rise in corporation tax is of historic proportions.

Debt worries

Good news on this year’s deficit is more than offset by an increase in borrowing next year. But it is the slightly longer-term numbers that really matters. While he didn’t quite tie himself to this, it looks pretty clear that the chancellor wants to achieve two outcomes.

First, he’d like to get to current budget balance, only borrowing for investment. That could still involve total borrowing in excess of £70 billion in 2025–26. Second, he’d like debt to be at least stabilised, and preferably on a downward trajectory. That’s not a bad set of aims for the medium term, and it is sensible given uncertainties to be no more specific than that at this stage.

We didn’t hear enough about those uncertainties yesterday.

Tax

While Mr Sunak told us time and again that he was being honest with us about what needed doing, he managed to find two big tax increases which will be somewhat hidden from most of us.

Freezing the income tax personal allowance is, as he said, a progressive tax increase. But it is the least progressive way of raising income tax. Even four years of freezes though will undo only a fraction of the increases we saw over the 2010s…

The really remarkable policy though was the raising of the corporation tax rate from 19% to 25%. This looks in large part like the act of a chancellor hemmed in by manifesto commitments not to raise the rates of income tax, VAT or NICs.

‘Absurdities’

Finally and briefly on tax I can’t end without mentioning two perennial absurdities. This is the 11th year in a row that a government supposedly committed to net zero greenhouse gas emissions has cut the tax on burning petrol and diesel. And the freeze in the lifetime allowance means that the goalposts have been moved for pension savings yet again – something which has happened at least every other year for the last 12 years. How savers are supposed to make long term plans for their retirement in such circumstances is beyond me.

09:54 AM

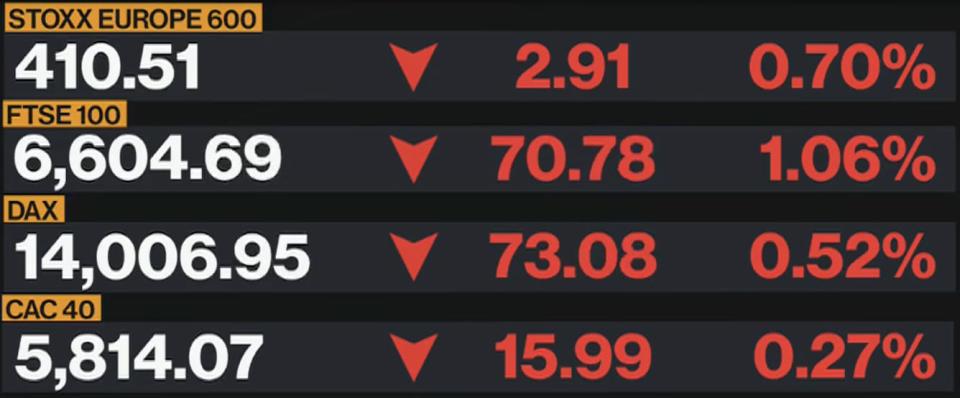

FTSE extends losses

The FTSE 100 has extended its losses, and is now down more than a percentage point. Miners are selling off sharply, with financial group also performing poorly.

Bloomberg TV - Bloomberg TV

09:52 AM

PJ’s verdict

The IFS’s omnipresent director Paul Johnson offered his snap verdict on the Budget yesterday:

What we can be sure of is that Rishi Sunak has spent big again, extending some support right through 2021 at a cost of an additional £60 billion or more. As a result borrowing is now forecast to again be above 10% of national income in the coming financial year.

Whether the big fiscal tightening planned for subsequent years will actually happen is less certain. It continues to depend on spending being lower than planned prior to the pandemic. And it also depends on a large increase in corporation tax actually being implemented without additional measures to at least ease its long-run impact.

Make no mistake, this proposed increase in the main rate of corporation tax is a big reversal of decades of policy direction and a significant risk. For all the rhetoric about it leaving the headline rate here below that in other G7 countries, our effective tax rate will be relatively high.

"Mr Sunak made much of his desire to be honest and to level with the British people. The fact that he felt constrained to raise taxes by hitting companies and through freezing allowances, rather than through more explicit rises in people’s taxes, suggests there are limits to how far he wants to level with us as he attempts to raise the overall tax burden to its highest sustained level in history.

Chancellor's needed to respond to big fiscal and big inequality challenges created by pandemic.

He set out a route to current budget balance via tax rises and tight spending after this year.

He said little on inequality: no promises on education, welfare etc

Chancellor Rishi Sunak has been speaking to BBC Radio 4’s Today programme this morning, where he argued the new rate would still be competitive. He added:

It is not coming in for two years, because in the short term we want to support economic recovery and when it does come in we will have a lower corporation tax rate than our G7 competitors.

09:43 AM

Construction activity rebounds

The UK’s construction sector bounced back to growth in February as commercial building activity offset a housing slowdown.

The latest construction purchasing managers’ index reading from IHS Markit came in at 53.3, clearing the no-change threshold of 50 following a slowdown in January.

IHS Markit said:

Extended supplier lead times persisted in February as vendors struggled with transport delays and stronger demand conditions. Stretched global supply chains, greater shipping charges and rising commodity prices all contributed to the sharpest increase in average cost burdens across the construction sector since August 2008.

Here are some key findings:

Residential work remained the strongest area of growth

The slowdown in house building was more than offset by the sharpest rise in commercial work since last September and a slower fall in civil engineering activity

New order volumes increased for the ninth consecutive month

Meanwhile, purchasing prices increased at a rapid pace

Duncan Brock from the Chartered Institute of Procurement & Supply, which helped gather the data, said:

With part-time furlough options now in place, some constructors will be mixing and matching their approaches to meet the ebb and flow of projects and capacity in the coming months.

09:25 AM

Kwarteng scraps Industrial Strategy Council – Sky

Kwasi Kwarteng - Jack Taylor/Getty Images

Business secretary Kwasi Kwarteng has scrapped the Industrial Strategy Council, which was created less than three years ago to advise the Government on industrial strategy, Sky News reports.

Sky News has learnt that Mr Kwarteng, who took over from Alok Sharma earlier this year, notified the 16 members of the Industrial Strategy Council on Wednesday that their services were no longer required.

He said the government had “decided to mark a departure from the Industrial Strategy brand”, implying that the department he runs – Business, Energy and Industrial Strategy – is likely to face yet another renaming in the coming months.

The Industrial Strategy Council, which was launched in November 2018 by Greg Clark, the then business secretary, is chaired by Andy Haldane, the Bank of England's chief economist.

Just days ago, members of the ISC gave evidence to MPs on the BEIS Select Committee, with Mr Haldane saying ministers must intervene in key domestic industries to boost the recovery and create a more self-reliant economy after Covid.

As my colleagues Tim Wallace and Tom Rees reported on Tuesday:

Speaking just weeks after the Government set out plans for a major new subsidies regime, Mr Haldane raised the prospect of more muscular intervention in the economy to prevent UK-based companies being taken over by foreign rivals - using vaccine maker AstraZeneca as an example.

Online gambling operator Entain has become the latest company pledging to hit net zero, aiming to eradicate net greenhouse gases across its supply chain and main operations by 2035 at the latest.

The FTSE 100 group, formerly known as GVC Holdings, reported a pre-tax profit of £174.7m for 2020, improving from a £154.4m loss the year before.

Entain said its online business saw an “exceptionally strong performance” during the year as a lot of locked-down people turned to only gambling for entertainment. Online net gaming revenues rose 27pc during the year, bringing the group to 20 consecutive quarters of double-digit growth.

In the UK, its Foxy Bingo brand performed particularly strongly.

We have a number of growth opportunities that will continue to drive the Group's performance and increase our scale. These include delivering on our clear ambition to be the leading operator in the US through BetMGM, growing in our core markets, entering into new regulated markets - both organically and via M&A – and expanding to reach new audiences.

08:51 AM

Melrose beats estimates despite swing to loss

Melrose Industries has risen this morning after beating expectations in its full-year results, despite swinging to a chunky loss.

The FTSE 100 turnaround specialist posted a statutory loss before tax of £523m for 2020, compared to a £55m profit the prior year.

It said trading was at the “top end” of management expectations during the second half of 2020, with non-aerospace divisions seeing revenue growth pick up during the six month to the end of December.

Melrose warned no recovery has been seen in the civil aerospace market, warning this “is not expected to change in 2021”. The division’s sales plunged 27pc last year.

Chair Justin Dowley said:

Whilst the Covid-19 crisis has had a major detrimental effect this year, Melrose has generated record cash flows and continued to invest to improve our businesses. All of this positions the Group well for a good recovery and strong performance in the future.

Royal Bank of Canada’s Mark Fielding said Melrose had made a “strong finish” to 2020, saying the group appeared to have “good momentum” outside of aerospace.

08:31 AM

Pound flat

The pound has shaken off a dip earlier in the day to trade basically flat, with investors still digesting Rishi Sunak’s latest Budget announcement.

08:22 AM

Sage launches £300m share buyback programme

IT group Sage has announced a it will begin a share buyback programme of up to £300m, which will run until early September at the latest.

The FTSE 100 group said:

The share buyback programme is consistent with the Group's disciplined approach to capital allocation, and reflects the sale proceeds from recent disposals and strong ongoing cash generation. The Group continues to have considerable financial flexibility to drive the execution of its growth strategy, supported by its robust financial position.

The group previously scrapped a £250m buyback programme last April in the face of the pandemic. Only £6m of purchases had been completed before the programme was frozen.

Morgan Stanley will act as brokers.

Stifel’s George O’Connor said the plans signal “that better times lie ahead”.

08:07 AM

FTSE dips at open

The FTSE has fallen slightly at the open, amid a wider moderate sell-off across European equities. The damage being done isn’t as extreme as what we saw in the US and Asian overnight, but it looks like things are firmly risk-off at the moment.

Bloomberg TV - Bloomberg TV

07:56 AM

Aviva exits Italy

Insurer Aviva has announced the sale of its Italian business for €873m, continuing a series of divestments aimed at strengthening its UK focus.

Its Italian life insurance business went to CNP Assurances for €543m, while its general insurance business was sold to Allianz for €330m.

Including the previous sale of Aviva Vita to UBI Blance, the FTSE 100 company said it will realise over €1.3bn in cash from its Italian exit.

Chief executive Amanda Blanc said:

Since I announced our new strategy in August last year, we have announced seven divestments that will generate over £5bn of cash proceeds. This rapid progress allows us to focus on transforming and growing our already strong businesses in the UK, Ireland and Canada.

The sales are expected to complete in the second half of 2021, pending regulatory approvals.

Aviva also released full-year results today, which I’ll get onto shortly.

07:46 AM

Deliveroo will make £8bn float in London

Will Shu - Aurelien Morissard/IP3/Getty Images

Deliveroo this morning selected London for its £8bn stock market floatation in a boost to Britain's plans to lure tech companies to the City.

My colleague Michael Cogley reports:

The food-delivery start-up, which was founded in the capital eight years ago by Will Shu, said the decision had “underscored” its commitment to the UK.

Mr Shu will make use of so-called “dual-class” shares should the company push ahead with its initial public offering.

The share structure, which was proposed by Lord Hill in a review on the City’s listing criteria this week and endorsed by Chancellor Rishi Sunak yesterday, allows founders to keep control of their companies when deciding on big decisions like mergers and takeovers.

Good morning. The FTSE 100 is set to open in the red as a bond sell-off continues to ignite concerns about inflation and weigh on equity markets.

It comes after chancellor Rishi Sunak announced the first corporation tax hike in nearly half a century on Wednesday as the Government looks to repair the public finances.

Asian shares fell on Thursday, tracking a decline on Wall Street as another rise in bond yields rattled investors who worry that higher inflation may prompt central banks to raise ultra-low interest rates.

Japan's Nikkei 225 lost 1.9pc to 29,004.41 and the Hang Seng in Hong Kong dropped 2.5pc to 29,129.81. Australia's S&P/ASX 200 lost 1.1pc to 6,742.90.

The Shanghai Composite index shed 1.9pc to 3,509.58. Investors are anticipating that policies outlined during the annual session of the National People's Congress, a largely ceremonial legislature that convenes on Friday, may point to a tightening of monetary and government stimulus.

South Korea's Kospi lost 1.5pc after the central bank reported the economy contracted in 2020 for the first time since 1998.

Coming up today

Corporate: Galliford Try, Manchester United (Interim results); Admiral Group, Alliance Trust, Aviva, Chemring Group, Coats, Entain, Hunting, John Laing, Meggitt, Melrose Industries, Morgan Advanced Materials, Rathbone Brothers, Rentokil Initial, Schroders, Spire Healthcare, Tyman, Vesuvius, Vistry, William Hill (Full year)

Economics: SMMT new car registrations, construction PMI (UK), retail sales, unemployment (eurozone), jobless claims, factory orders (US)

Jason Fitz and Frank Schwab join forces to recap the draft in the best way they know how: letter grades! Fitz and Frank discuss all 32 teams division by division as they give a snapshot of how fans should be feeling heading into the 2024 season. The duo have key debates on the Dallas Cowboys, New York Giants, New Orleans Saints, Los Angeles Rams, New England Patriots, Las Vegas Raiders and more.

The first electric vehicle I ever drove was a Tesla Roadster in 2011. It was with great anticipation that I slid behind the wheel of the 2025 Acura ZDX Type S. Sure, it's a midsize SUV, but it wears the Type S moniker, a name reserved only for the most fun-to-drive in the Acura stable. On launch, the ZDX will be available in A-Spec and Type S trims -- both of which come equipped with a 102 kWh battery.