Marvel Decor (NSE:MDL) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Marvel Decor Limited (NSE:MDL) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Marvel Decor

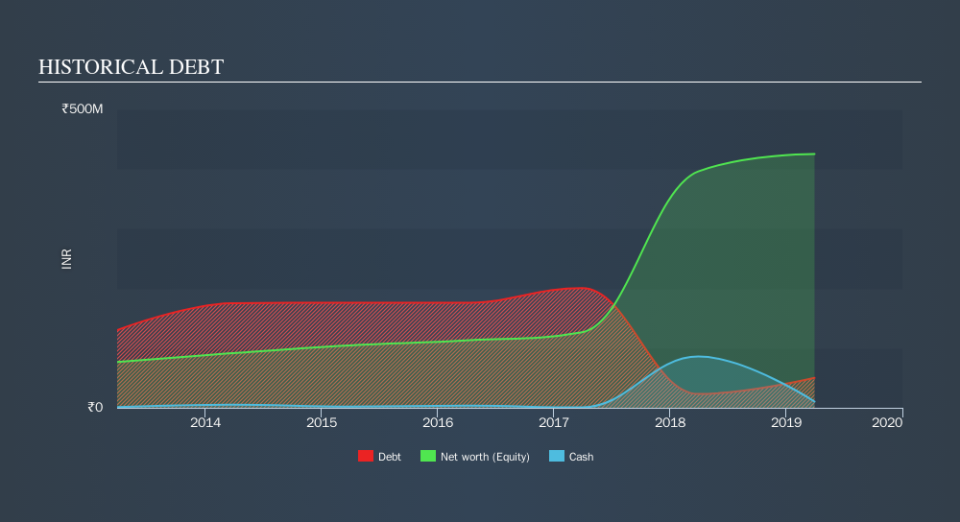

What Is Marvel Decor's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Marvel Decor had ₹50.2m of debt, an increase on ₹23.1m, over one year. However, it also had ₹10.4m in cash, and so its net debt is ₹39.8m.

How Healthy Is Marvel Decor's Balance Sheet?

The latest balance sheet data shows that Marvel Decor had liabilities of ₹129.1m due within a year, and liabilities of ₹32.4m falling due after that. Offsetting this, it had ₹10.4m in cash and ₹47.5m in receivables that were due within 12 months. So its liabilities total ₹103.6m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Marvel Decor is worth ₹289.7m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Marvel Decor has a low net debt to EBITDA ratio of only 0.55. And its EBIT covers its interest expense a whopping 42.2 times over. So we're pretty relaxed about its super-conservative use of debt. On the other hand, Marvel Decor's EBIT dived 17%, over the last year. If that rate of decline in earnings continues, the company could find itself in a tight spot. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Marvel Decor will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Marvel Decor saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Marvel Decor's EBIT growth rate and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But on the bright side, its interest cover is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Marvel Decor stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. Over time, share prices tend to follow earnings per share, so if you're interested in Marvel Decor, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.