Mordovia Energy Retail Company (MCX:MRSB) Takes On Some Risk With Its Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Mordovia Energy Retail Company Public Joint-Stock Company (MCX:MRSB) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Mordovia Energy Retail Company

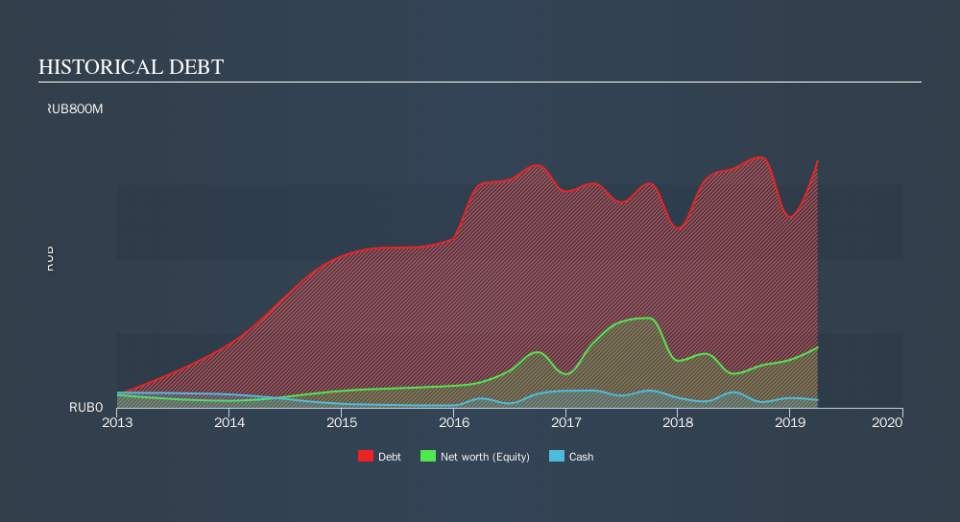

What Is Mordovia Energy Retail Company's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Mordovia Energy Retail Company had ₽661.8m of debt, an increase on ₽611.3m, over one year. On the flip side, it has ₽21.1m in cash leading to net debt of about ₽640.7m.

How Strong Is Mordovia Energy Retail Company's Balance Sheet?

We can see from the most recent balance sheet that Mordovia Energy Retail Company had liabilities of ₽1.24b falling due within a year, and liabilities of ₽1.96m due beyond that. On the other hand, it had cash of ₽21.1m and ₽976.5m worth of receivables due within a year. So it has liabilities totalling ₽245.4m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Mordovia Energy Retail Company has a market capitalization of ₽509.8m, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn't worry about Mordovia Energy Retail Company's net debt to EBITDA ratio of 4.8, we think its super-low interest cover of 1.7 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. One redeeming factor for Mordovia Energy Retail Company is that it turned last year's EBIT loss into a gain of ₽88m, over the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is Mordovia Energy Retail Company's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Considering the last year, Mordovia Energy Retail Company actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

On the face of it, Mordovia Energy Retail Company's net debt to EBITDA left us tentative about the stock, and its interest cover was no more enticing than the one empty restaurant on the busiest night of the year. But at least its EBIT growth rate is not so bad. It's also worth noting that Mordovia Energy Retail Company is in the Electric Utilities industry, which is often considered to be quite defensive. Overall, we think it's fair to say that Mordovia Energy Retail Company has enough debt that there are some real risks around the balance sheet. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check Mordovia Energy Retail Company's dividend history, without delay!

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.