Morgan Stanley Bullish on These 2 Stocks for at Least 40% Upside; Here’s Why

Inflation has been making headlines all year, and rightly so; it’s at 40-year high levels, driven by sharp increases in the prices of gasoline and diesel fuels. But oil and its various refined products have come down in recent weeks, and so – the July inflation numbers weren’t as bad as had been feared. The overall year-over-year price increase for the month came to 8.5%, still awful, but less than the 8.7% economists had been predicting. Markets these days are rallying in response.

Whether this rally will be long-lasting or ephemeral is up in the air, and depends much on how economic indicators develop through the rest of the year, but for now, Wall Street’s top investment firms are busy picking out stocks that are poised for wins no matter what. So let’s follow one of these major banks, Morgan Stanley, and find out what stocks its analysts are choosing.

Just in recent days, that firm’s analysts have tapped two stocks they see with double-digit upside for the coming months, on the order of 40%, or more. Using TipRanks' database, we've pulled up the latest details on these Morgan Stanley choices. Let's find out what the analysts have to say.

DraftKings (DKNG)

First up is DraftKings, a leader among online fantasy sports league and sports betting venues. The company stands at the cutting edge of online sports and betting activities, offering its users a range of products including the best in fantasy sports leagues, comprehensive sportsbook betting, online casino gaming, and even a marketplace for NFTs.

Given the popularity of both sports and betting, it should come as no surprise that DraftKings saw its revenues rise in the most recent quarter. The top line for 2Q22 was reported at $466 million, for a year-over-year gain of 57%. This result was driven by the company’s B2C activity, which grew 68% year-over-year to reach $455 million.

DraftKings’ solid revenues found support from the drill downs in regard to users. A key metric, monthly unique payers (MUPs) saw 30% y/y growth to reach 1.5 million. A related metric, the ARPMUP, or average revenue per MUP, also grew 30% y/y and hit $103. These gains indicate success in both customer acquisition and retention, as well as success in promoting customer engagement.

Morgen Stanley's Ed Young feels that DraftKings is fully capable of continuing its recent growth, and writes: “We continue to believe DKNG is executing on its plan of narrowing EBITDA losses and moving towards profitability as more states mature and generate positive contribution profit… Management mentioned on the call its continued growth in users and having seen no material impact on the business from macro-economic conditions. In our view, online gambling is a proven profitable business globally and we think it is nascent enough in the US that the broader economic outlook will have minimal near-term impact on the industry."

"We also think the company's greater emphasis on cost control is a welcome shift in tone, albeit this shift remains in its early stages. We expect the prospects for CA legalization (ballot 8 Nov) and its potential ramifications on capital requirements to remain a key catalyst for the stock,” the analyst added.

To this end, Young puts an Overweight (i.e. Buy) rating here, and a $30 price target that indicates the chance of ~47% upside in the year ahead. (To watch Young’s track record, click here)

Overall, this stock keeps a Moderate Buy consensus rating from the Street, based on 16 analyst reviews that include 9 to Buy and 7 to Hold. The shares are priced at $20.40 and their average price target, at $23.07, suggests ~13% upside this year. (See DraftKings stock forecast on TipRanks)

Guardant Health (GH)

The second stock on Morgan Stanley's radar is Guardant Health, a biotech company that’s taking a unique approach to the sector. Rather than work on new therapeutic agents or medications, Guardant has focused its research and development efforts on the development of new blood tests and lab methodology for the improvement of diagnosis and treatment in precision oncology. In short, the company recognizes that proper treatment requires early and accurate diagnostics – and it is working on tests that will allow drug companies to create better targeted therapies. To date, Guardant boasts that more than 9,000 doctors have used more than 200,000 of its blood tests.

Guardant currently has a portfolio of tests and test kits available for patients with both early and late stage cancers, and for cancer screening. The company’s two leadings tests are the Guardant360 CDx, the first complete genomic test approved by the FDA, able to provide doctors with full genomic results for all solid cancers via a simple blood draw; and the Guardant360 TissueNext, a simplified biopsy test used when tissue testing is more appropriate than blood draws. Guardant’s tests have found widespread acceptance from medical professionals, providers, and payers, and are broadly covered by Medicare and private payers, which combined represent a potential patient base some 200 million strong.

Guardant hasn’t rested on its laurels, and is developing new tests and new test procedures. The company is currently conducting the ECLIPSE clinical trial, a study of the Shield blood test for the detection of early stage colorectal cancer. The company expects to have initial data readouts – and to make the PMA submission to the FDA – from ECLIPSE later this year.

Medical testing is big business, and Guardant’s Q2 revenue came in at $109.1 million, for a 19% year-over-year increase. The company indicated that clinical and biopharma volumes drove the revenue gains; clinical testing was up 40% and biopharma use up 65% y/y. Guardant reported having $1.2 billion in cash and liquid assets available as of the end of 2Q22.

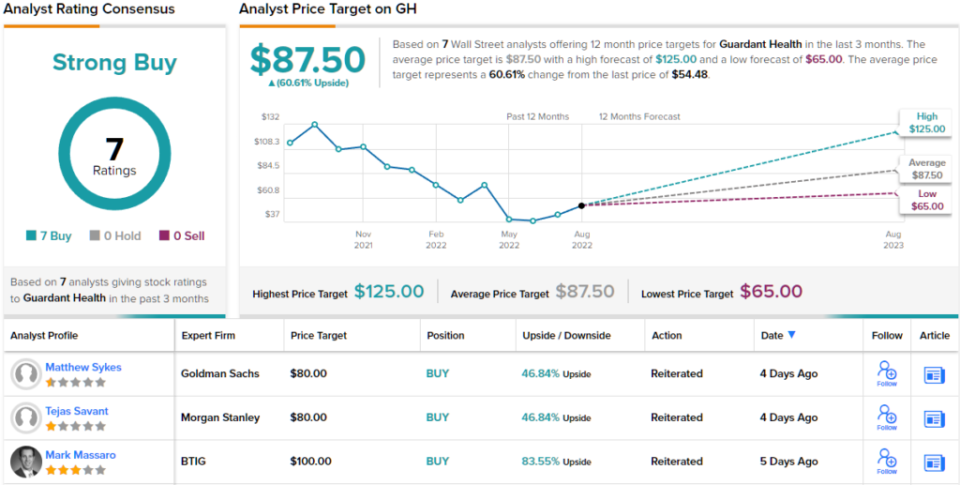

Covering this stock for Morgan Stanley, analyst Tejas Savant comes down firmly with the bulls, writing: “GH remains extremely well positioned in the attractive liquid biopsy vertical, with room for multiple competitors in the space in light of the low levels of penetration today, in our view. While near-term, we see building evidence of clinical utility and adoption set to drive additional payor coverage for G360, we see GH rapidly transitioning into a platform play offering both tissue and liquid biopsy testing... We view current levels as affording a highly opportunistic entry point for patient investors.”

In line with his bullish stance, Savant rates GH a Buy, and his $80 price target implies room for ~47% upside potential in the next 12 months. (To watch Savant’s track record, click here)

The Street’s opinion on this test-oriented biotech is clear: all 7 of the recent analyst reviews are positive, giving GH shares a unanimous Strong Buy consensus rating. The stock is selling for $54.48 and its average price target of $87.50 implies ~61% upside in the next 12 months. (See Guardant stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.