Most Shareholders Will Probably Find That The CEO Compensation For Equity Commonwealth (NYSE:EQC) Is Reasonable

Despite Equity Commonwealth's (NYSE:EQC) share price growing positively in the past few years, the per-share earnings growth has not grown to investors' expectations, suggesting that there could be other factors at play driving the share price. The upcoming AGM on 23 June 2021 may be an opportunity for shareholders to bring up any concerns they may have for the board’s attention. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

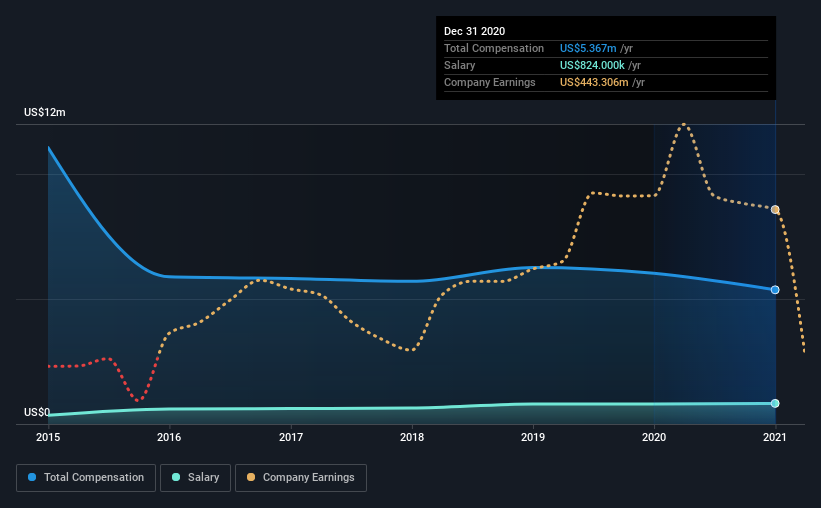

See our latest analysis for Equity Commonwealth

How Does Total Compensation For David Helfand Compare With Other Companies In The Industry?

Our data indicates that Equity Commonwealth has a market capitalization of US$3.4b, and total annual CEO compensation was reported as US$5.4m for the year to December 2020. Notably, that's a decrease of 11% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$824k.

On comparing similar companies from the same industry with market caps ranging from US$2.0b to US$6.4b, we found that the median CEO total compensation was US$5.3m. So it looks like Equity Commonwealth compensates David Helfand in line with the median for the industry. Furthermore, David Helfand directly owns US$23m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2020 | 2019 | Proportion (2020) |

Salary | US$824k | US$800k | 15% |

Other | US$4.5m | US$5.2m | 85% |

Total Compensation | US$5.4m | US$6.0m | 100% |

Talking in terms of the industry, salary represented approximately 15% of total compensation out of all the companies we analyzed, while other remuneration made up 85% of the pie. Although there is a difference in how total compensation is set, Equity Commonwealth more or less reflects the market in terms of setting the salary. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Equity Commonwealth's Growth

Equity Commonwealth's funds from operations (FFO) took a hit this year, falling to -US$702k from US$75m last year. It saw its revenue drop 41% over the last year.

A lack of improvement is not good to see. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Equity Commonwealth Been A Good Investment?

With a total shareholder return of 21% over three years, Equity Commonwealth shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

While it's true that shareholders have owned decent returns, it's hard to overlook the lack of earnings growth and this makes us question whether these returns will continue. Shareholders should make the most of the coming opportunity to question the board on key concerns they may have and revisit their investment thesis with regards to the company.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 3 warning signs for Equity Commonwealth you should be aware of, and 1 of them can't be ignored.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.