Yahoo Autos

Yahoo Autos Mr. Musk and His Ever-Expanding Empire: Why Is Tesla So Loved by Wall Street?

From the February 2018 issue

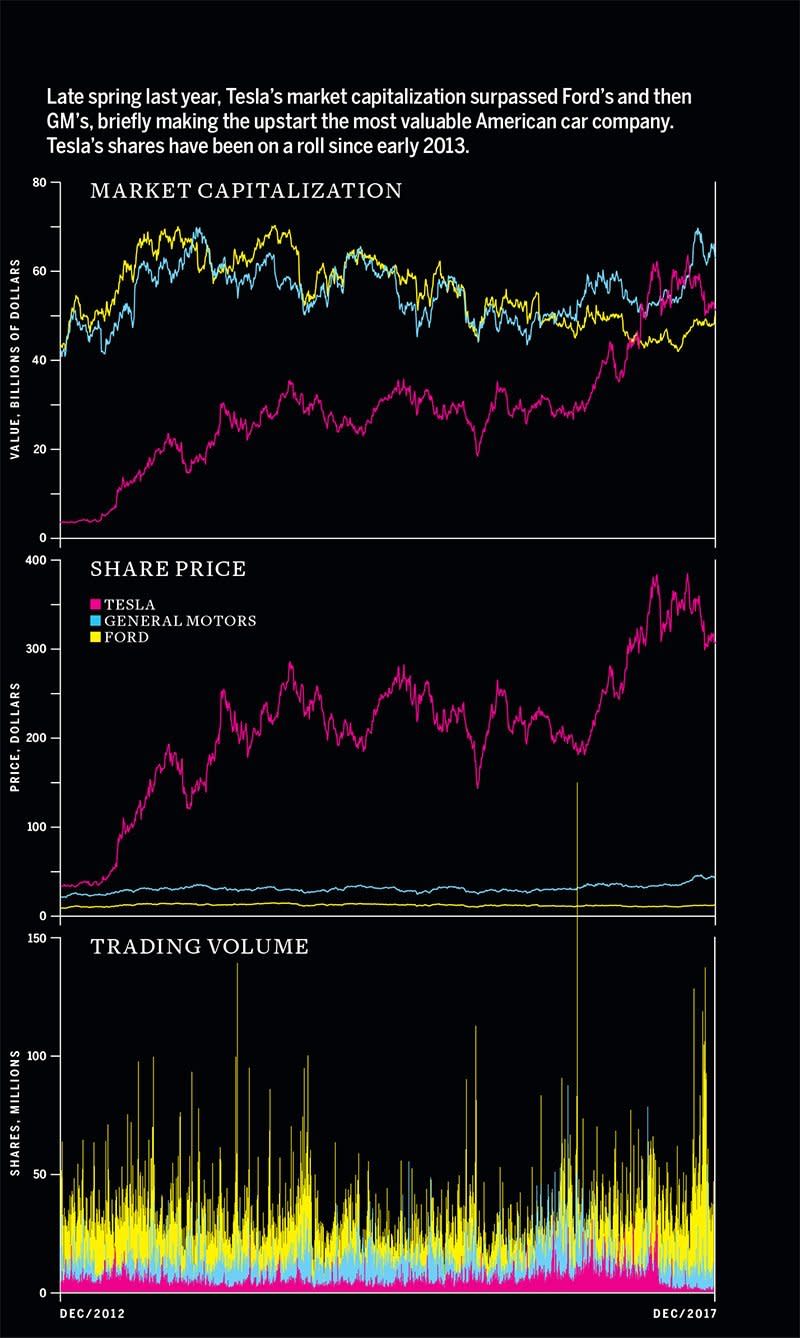

In 2013, two finance professors, Bradford Cornell of the California Institute of Technology and Aswath Damodaran of New York University’s Stern School of Business, started to notice something screwy happening on the NASDAQ, the world’s second-largest stock exchange. Shares in Tesla (TSLA) were exploding, even though the fledgling electric-vehicle manufacturer was selling fewer than 2000 cars a month in the 1.3 million-a-month U.S. auto market. For most of the two-plus years since Tesla’s June 2010 initial public offering, the carmaker’s stock had waddled around in the $22-to-$35 range. On March 19, 2013, TSLA began to go up—and it kept rising.

Over the next six months, it would jump to $180. Less than a year later, it would reach $291. Ford’s stock wouldn’t hit $19 during this period, and GM’s peaked at $41. Fiat Chrysler flirted with $8 but never quite got there. Meanwhile, Tesla’s market capitalization—the price of the stock multiplied by the number of shares issued—surpassed Fiat’s. (It would later briefly eclipse the other Big Three automakers, too.) Trading volume spiked as well, with tens of millions of shares changing hands some days.

Many investors look at Tesla more as a technology company than as a manufacturer, and tech companies are generally valued more highly than carmakers. Still, Cornell and Damodaran set to find out how market sentiment might be affecting Tesla’s stock price. They looked at Tesla’s returns for every trading day between March 22, 2013, and February 26, 2014, as well as news about the company during that period, including reports of how much money the company was making—or, as was most often the case, how much it was losing. “If the market is rational and relatively efficient, then the run-up in the price of Tesla stock . . . should be the result of information that arrives during that time period,” Cornell and Damodaran wrote in a paper they posted online in April 2014. And yet, “there is no new-product introduction. There is no proposed acquisition or other transaction. There is no announcement of significant new technology . . . In fact, in several cases, the main news story was the rise in the stock price itself.” Tesla shares have not fallen below $141 since, reaching a high of $389 in September 2017.

“I have tremendous admiration for Tesla,” says Mark Yusko, CEO and chief investment officer of Morgan Creek Capital Management, a financial consulting firm in Chapel Hill, North Carolina. “Their products are beautiful; they created this brand of luxury. I have admiration for them pushing the technology. But the stock is one of the most egregious examples of overvaluation.”

For years, auto execs have gnashed their teeth over how a company, which sells a volume of vehicles that amounts to a rounding error in Detroit, has seen its stock rise more than 900 percent while the NASDAQ rose by 60. Ford’s stock is flat, while the Dow Jones and S&P 500 each climbed more than 130 percent. Even though GM, with the Chevrolet Bolt, beat Tesla to releasing a sub-$40,000 electric car that can go 200 miles on a charge—a threshold for EVs going mainstream—GM’s shares have also failed to keep pace with the broader market since Tesla first went public. TSLA has a few true believers in the financial industry who think it is fairly valued or could go even higher, but Yusko is just one of many portfolio managers, stock pickers, finance professors, and industry analysts at investment banks who balk at its valuation.

Mike Zavislan won’t say on the record how much money he lost last year betting against Tesla, but it’s a lot. Much more than you will make at your job this year, probably. But he’s not worried. “I could give you a thousand reasons why Tesla’s overvalued,” he says. Zavislan is so confident the stock is going to fall that he holds what are known as naked call options, which expose him to losing an unlimited amount of money if TSLA should go above his $500 call price and stay there instead.

Zavislan maintains an unusual perspective on the question of why Tesla’s price has become decoupled from all the metrics that stock pickers have traditionally considered in valuing a company. He’s not just a guy with an Ameritrade account; he owns a used-car dealership in Pueblo, Colorado. So he’s not going to argue that the stock’s price-to-book ratio is bad or give you his opinion on whether the company’s supposed cost advantage in batteries is going to last. He’ll tell you about how snow gets in the cabin when the falcon-wing rear doors on the Model X open, or that dealers have trouble valuing used Teslas when they hit the trade-in market. “All these things that people don’t know yet are gonna come out, and when they do, that stock’s gonna go down,” he says. A Tesla spokesperson declined to comment on the company’s valuation, the role of investor sentiment in its stock price, or the resale value of its vehicles.

Zavislan points out that Tesla stopped guaranteeing a resale value on vehicles purchased after July 1, 2016, a promise the company had initially said was “backed personally by Tesla CEO Elon Musk.” This program was intended to assure buyers of a pricey vehicle with no track record of reliability that they’d be able to unload their cars for a decent price after a few years. The move to lift the guarantee freed up some cash and improved Tesla’s balance sheet, making the stock more attractive, but it also meant used-car dealers would have a harder time pricing the vehicles and may be less likely to risk taking them off the hands of owners shopping for a new car. “A lot of dealers don’t know how to handle Teslas,” Zavislan says.

Caltech’s Cornell also shorts Tesla’s stock but through the hedge fund he runs, SMBP, which has developed a computer program to crawl Tesla’s website, recording the new and pre-owned inventory listed there to speculate about its sales. “Xs and the Model S appear to be plateauing,” Cornell says, “both new and used.” Tesla, however, reported a 4.5 percent increase in third-quarter deliveries in 2017 compared with the previous year. Unlike every other volume carmaker, Tesla does not issue monthly U.S. sales reports, but rather makes quarterly delivery statements that include foreign sales.

Finance pros have other reasons for believing TSLA can’t maintain its run. The traditional method of ascribing value to a stock involves projecting the amount of cash the company is going to earn and discounting that back to present value. That allows analysts to predict the company’s price-to-earnings ratio (P/E), which is the cost of a share relative to the company’s per-share profits. The formula is expressed like this: P/E = stock price/(company profits/number of outstanding shares). It’s a key metric that stock pickers look at in deciding whether to invest in a company or whether it’s time to sell.

The S&P 500’s historic P/E is around 15; today, it’s around 25. Most of the time, Tesla doesn’t have a P/E ratio because the company has no earnings. But in those quarters when Tesla has been profitable, its P/E has neared 1400. (Although the accounting practices behind that “profitability” are hotly disputed among investors.) Selling only a few thousand cars a month, Tesla has weak cash flow. While other companies trade at many multiples of the market average or else lose money, one of two things is generally true of them: Either they have robust cash flow—a lot of money is coming in, but they don’t turn a profit because they’re investing it back into the business—or their stock sooner or later falls back to earth. The prime example of the former is Amazon; for examples of the latter, think of any company that saw growth during the internet bubble circa 1998–2000.

Cornell points out that analysts can justify any share price if they’re willing to tweak the numbers infinitely. “If you project high enough profit margins for Tesla and enough sales 5 or 10 years down the road, you can rationalize almost any value,” he says. Nevertheless, the exercise is typically more of an effort to estimate the company’s potential to generate revenue, and anyway, what an analyst can plausibly rationalize eventually reaches a limit. Yusko has calculated that to justify a stock price of $350, Tesla would need to have 100 percent market share in cars costing $50,000 and up, which seems beyond reckoning.

“Let’s kick it off with Mars, okay?”

The occasion was Tesla’s conference call with industry analysts last February to report earnings for the fourth quarter of 2016. The earnings call is an invisible dance that execs at publicly traded companies perform to please their patrons—institutional investors who pour billions into their stock—and analysts whose ratings can erase billions in company value overnight. The speaker was Adam Jonas, a Morgan Stanley analyst and prominent Tesla bull. Tesla had missed analysts’ consensus earnings forecast by 60 percent. Others, later in the call, took the opportunity to ask its execs why a software update for the Model S and Model X had been delayed and how the company intended to increase production of the forthcoming Model 3. But Jonas wanted to know whether Musk would potentially be taking time away from Tesla to focus on his aerospace company, SpaceX, in the event that the new administration is in favor of accelerating a manned mission to Mars, which NASA says isn’t happening for another two decades. Yusko says that SpaceX lends sexiness to Tesla, helping its stock price. “A guy who can talk about going to Mars and not be roundly ridiculed, that’s impressive,” he says. “People want to believe.”

It’s part of Tesla’s aura, which analysts and academics agree is a significant driver of its stock price. Musk’s uncanny ability to generate news with his tweets is rivaled only by Donald Trump’s. “Tesla is arguably the most followed stock in popular media outside of maybe Apple,” says Brad Erickson, an industry analyst at KeyBanc Capital Markets. “People hear about it all the time on TV; Elon Musk is in the news 14 times a day. It’s a very available narrative to follow, and clearly that’s compelling a lot of people to buy the stock.”

Unlike the pros, “retail” investors—part-timers or hobbyists who manage their own portfolios, some even earning a living doing it—tend to be more swayed by buzz than fundamentals, market watchers agree. Their trading can initiate a phenomenon known as “seeding the clouds,” where buying prompts computers that trade based on algorithms to get in on the action, driving the price higher. Professionals who are shorting the stock then need to cover their bets by buying shares, pushing the price up even higher. Essentially, movement in price alters the behavior of market participants, lifting the stock in a reflexive cycle.

So why might Jonas be interested in diverting attention from Tesla’s car business? Morgan Stanley is one of the companies that issued Tesla stock in 2016, generating significant revenue via underwriter fees for the investment bank. Six months after the “Mars” earnings call, Morgan floated bonds to raise more cash for Tesla, bringing in revenue for the bank, too. (Morgan Stanley spokesperson Euna Cook said, “Our research is independent of all our other businesses,” and declined comment on the intent of Jonas’s question about Mars.) Because the business of selling Teslas generates so little cash, the company finances itself largely through the sale of such bonds as well as through its high stock price.

Tesla’s boosters in the financial sector give a lot of reasons why the stock is worth $350 or even more. In August, Bill Selesky of Argus Research set a price target of $444. “These guys could be making serious money in 2021,” he says. “My price target rationale is using a multiple of 2020 earnings of about 20 times.” He thinks it makes sense, given the changes that are coming to the auto industry precipitated by automation.

"Scaling from making a few really, really nice $100,000 cars to actually making a mass-market car–it’s really hard." —Mark Yusko, Morgan Creek Capital Management

Indeed, many market observers see Tesla differently than other car manufacturers since its vehicles are designed with an automated future in mind. Delphi Automotive’s chief technology officer, Glen De Vos, recently gave a talk explaining how the supplier was beginning to help OEMs transition to designing cars as a software-defined platform, necessitated by the coming automation revolution. De Vos asserted that every time an automotive feature is introduced—from the radio to anti-lock brakes to telematics—traditional carmakers simply tack on a new electronic control unit and connect everything with a spaghetti of copper wire. With automated vehicles, though, manufacturers need a simpler, more energy-efficient architecture to consolidate the vehicle’s computing power and allow the software to be managed independently of the underlying hardware. “The company that’s closest to this, quite frankly, is Tesla,” De Vos said. “They’re demonstrating the power and value of doing this type of architecture.”

A former GM analyst agrees with De Vos that Tesla will dominate the automation revolution. David Keith, now assistant professor of system dynamics at MIT Sloan School of Management, sees the company as a tech disrupter that will flatten existing operators in its field. “Incumbents struggle to survive when a disruptive technology comes along,” says Keith, who drives a Tesla. “I could give you any number of examples of this: Nokia and BlackBerry when the iPhone came along; Blockbuster with Netflix.”

But market research and consulting firm Navigant Research recently put out a report ranking GM and Ford as far better “equipped to be the leaders in developing complete automated driving stacks.” Tesla lagged Detroit’s behemoths in the sales, marketing, and distribution category, as well as in staying power and, surprisingly, technology. “I think Ford and GM are much more interesting investments,” said Yusko in August, as Tesla was struggling to launch its new Model 3.

He’s not alone. Analyst ratings as of December 1 were 11:2 “buy” versus “sell” on GM and 5:2 on Ford, according to the Wall Street Journal’s rolling survey, and many of the Detroit bulls specifically cite the dinosaurs’ potential to excel in electric- and automated-vehicle production. Asset management and investment advisory firm Guggenheim Investments upgraded its rating on GM stock to “buy” on November 20, citing the company’s confidence in “launch[ing] a ride-hailing fleet of robo-taxis before 2020,” providing a “sizable earnings opportunity from mobility services for GM over the next 5 to 10 years.” Sure enough, 10 days later, GM announced it would become a competitor to Uber and Lyft before 2019, with its automated vehicles undercutting human-driven ride sharing on price by 40 percent. Similarly, Deutsche Bank’s market research division bumped its rating on GM from “neutral” to “buy” in November: “In an upside scenario, this stock could more than double,” wrote analysts Rod Lache and Shreyas Patil. Ford has also received market accolades: Standpoint Research recommends buying Ford, expecting it “to be a leader in the growing electrified-vehicle market.” (Standpoint, incidentally, rates Tesla stock as a “sell.”)

Even the strongest Tesla bulls acknowledge that earnings need to come eventually for the stock price to make sense. The company’s boosters in the green community have bought into Musk’s vision of radically transforming our greenhouse-gas-intensive infrastructure, putting a Tesla Powerwall battery in every garage, connected to SolarCity roof tiles on one end and a Tesla vehicle on the other. “Think AAPL,” as (at least) one Tesla investor put it on Twitter, referencing Wall Street’s other darling, Apple. Or maybe Tesla will succeed by licensing its automated-car technology and battery-management software to companies that have a century’s more experience with what much of Silicon Valley regards as the mundanity of making things. (Tesla declined to comment on whether it has such plans.) At least there’s a model for that: Qualcomm’s patents make possible virtually every cellular data transmission in the world outside of China. (Actually those, too, the company claims.) Or is the Tesla semi-truck Musk unveiled in November more than sleight of hand, an actual harbinger of how the company will be like GE or BASF, less a consumer-facing brand than a supplier? Or will Tesla simply succeed at what hasn’t been done in half a century—starting a major car brand that lasts?

For now, at least, financial analysts rely on huge sales of the Model 3 in their estimates to make their spreadsheets work. Jonas has said that by 2040, there will be 32 million Teslas on the road, so the valuation of the stock ought to be based on that. Yet the company revealed in October that although it had hoped to be making 5000 Model 3s a week by the end of 2017, it had managed to manufacture just 260 in the entire third quarter, with reports indicating that the company was building them partly by hand.

“Scaling from making a few really, really nice $100,000 cars to actually making a mass-market car—it’s really hard,” says Yusko. Cornell thinks there are just too many things that can go wrong for Tesla to become a mass-market automaker. “They’ve gotta get this Model 3 out, it’s gotta be as popular as everyone is hoping, they’ve gotta produce it at a good margin, they’ve gotta service it, they’ve gotta have charging centers,” he says. “There’s just a million things that have to go right, and the market seems to be so taken with the company that it assumes all of them are going to happen.”

If all these things do go right, the skeptics who shorted the stock could be hurting. “All the stock really needs is for the Model 3 to be awesome,” says Erickson. “If that car is awesome, the stock can probably continue to work.”