Natural Gas Services Group, Inc. (NYSE:NGS) Released Earnings Last Week And Analysts Lifted Their Price Target To US$16.00

Natural Gas Services Group, Inc. (NYSE:NGS) just released its first-quarter report and things are looking bullish. Natural Gas Services Group outperformed on both revenues and the expected loss per share, with revenues of US$18m beating estimates by 14%. Statutory losses were US$0.03, 63% smaller thanthe analysts expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

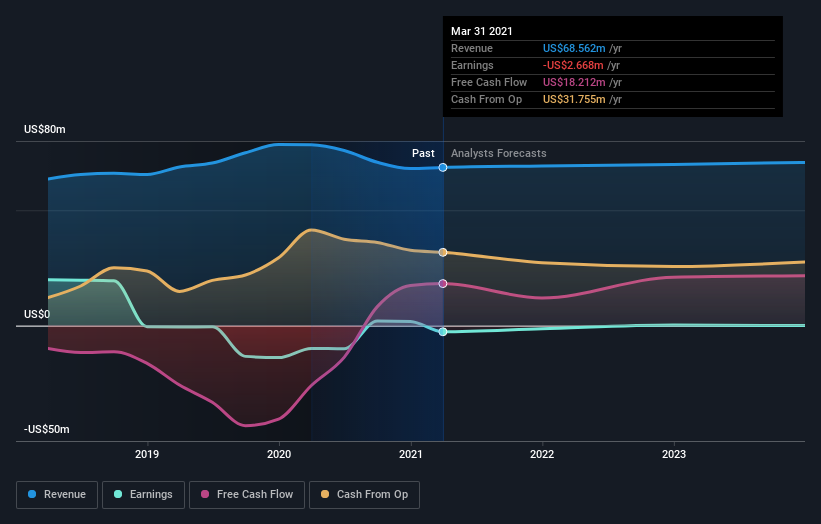

View our latest analysis for Natural Gas Services Group

Taking into account the latest results, Natural Gas Services Group's dual analysts currently expect revenues in 2021 to be US$69.2m, approximately in line with the last 12 months. Losses are predicted to fall substantially, shrinking 50% to US$0.10. Before this latest report, the consensus had been expecting revenues of US$67.1m and US$0.13 per share in losses. So it seems there's been a definite increase in optimism about Natural Gas Services Group's future following the latest consensus numbers, with a notable improvement in the loss per share forecasts in particular.

The consensus price target rose 6.7% to US$16.00, with the analysts encouraged by the higher revenue and lower forecast losses for next year.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's also worth noting that the years of declining sales look to have come to an end, with the forecast for flat revenues to the end of 2021. Historically, Natural Gas Services Group's sales have shrunk approximately 2.1% annually over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 10% annually. So it's pretty clear that, although revenues are improving, Natural Gas Services Group is still expected to grow slower than the industry.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. They also upgraded their revenue estimates for next year, even though sales are expected to grow slower than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Natural Gas Services Group going out as far as 2023, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.