Is Navamedic (OB:NAVA) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Navamedic ASA (OB:NAVA) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Navamedic

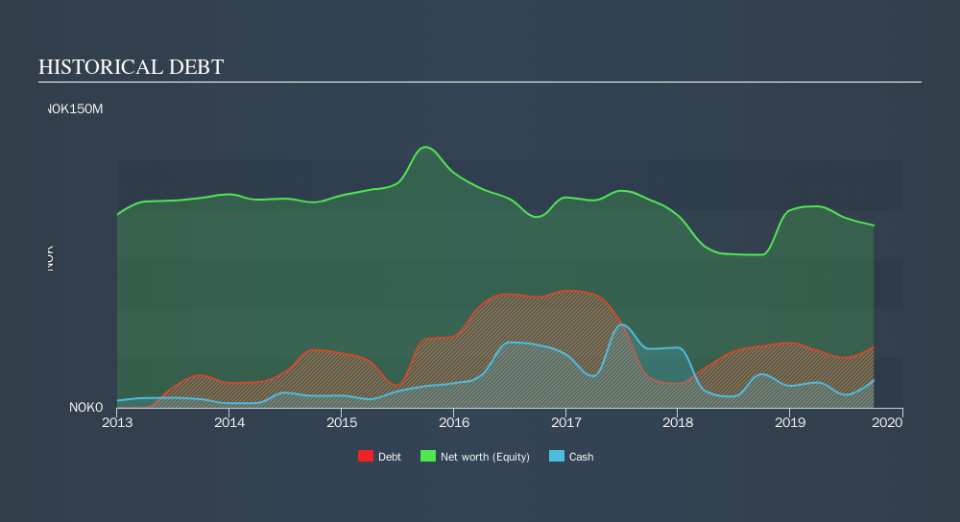

What Is Navamedic's Net Debt?

As you can see below, Navamedic had kr28.8m of debt at September 2019, down from kr31.0m a year prior. However, because it has a cash reserve of kr13.8m, its net debt is less, at about kr15.0m.

How Healthy Is Navamedic's Balance Sheet?

The latest balance sheet data shows that Navamedic had liabilities of kr126.7m due within a year, and liabilities of kr9.40m falling due after that. Offsetting these obligations, it had cash of kr13.8m as well as receivables valued at kr36.0m due within 12 months. So its liabilities total kr86.3m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Navamedic is worth kr217.4m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Navamedic will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Navamedic wasn't profitable at an EBIT level, but managed to grow its revenue by9.0%, to kr193m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Navamedic had negative earnings before interest and tax (EBIT), over the last year. Indeed, it lost kr9.7m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. We would feel better if it turned its trailing twelve month loss of kr1.3m into a profit. So we do think this stock is quite risky. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Navamedic insider transactions.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.