Is Nobina (STO:NOBINA) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Nobina AB (publ) (STO:NOBINA) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Nobina

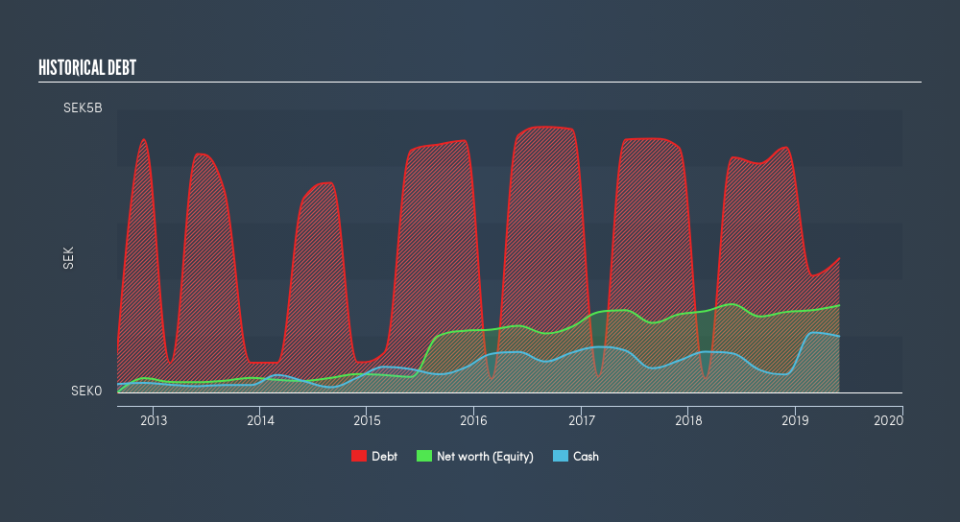

How Much Debt Does Nobina Carry?

You can click the graphic below for the historical numbers, but it shows that Nobina had kr1.70b of debt in May 2019, down from kr4.15b, one year before. However, it also had kr992.0m in cash, and so its net debt is kr704.0m.

How Healthy Is Nobina's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Nobina had liabilities of kr3.21b due within 12 months and liabilities of kr4.82b due beyond that. Offsetting these obligations, it had cash of kr992.0m as well as receivables valued at kr802.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by kr6.24b.

Given this deficit is actually higher than the company's market capitalization of kr4.81b, we think shareholders really should watch Nobina's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Looking at its net debt to EBITDA of 0.50 and interest cover of 5.0 times, it seems to us that Nobina is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. If Nobina can keep growing EBIT at last year's rate of 14% over the last year, then it will find its debt load easier to manage. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Nobina's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Nobina generated free cash flow amounting to a very robust 97% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

When it comes to the balance sheet, the standout positive for Nobina was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. To be specific, it seems about as good at staying on top of its total liabilities as wet socks are at keeping your feet warm. Looking at all this data makes us feel a little cautious about Nobina's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. We'd be motivated to research the stock further if we found out that Nobina insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.