Nordstrom (JWN) Q3 Earnings Lag Estimates, Revenues Beat

Nordstrom, Inc. JWN reported third-quarter fiscal 2021 results, wherein the bottom line missed the Zacks Consensus Estimate while the top line beat the same. Both the metrics rose year over year. The results gained from improved merchandise, innovative brand partnerships, solid e-commerce growth and sturdy performance at its Nordstrom banner store. The company is making efforts to optimize inventory levels and improve Nordstrom Rack’s performance.

It is progressing well with the merchandising strategy and has recently partnered with Fanatics and ASOS in a bid to offer a broader assortment in new and existing categories. The ASOS brand will now be available on nordstrom.com and in two stores. The company intends to expand in-store ASOS offering with a market rollout launch this spring. Nordstrom is on track with plans to integrate the network of stores and digital platforms for this year’s holiday season.

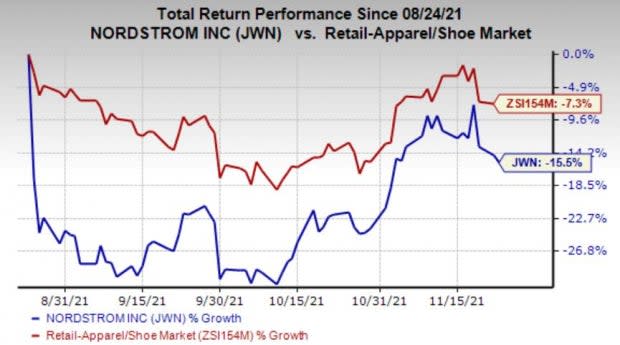

JWN slumped more than 23% in the after-market session on Nov 23. This might be due to supply-chain disruptions, high labor costs and weakness in its Nordstrom Rack off-price stores. Consequently, the Zacks Rank #3 (Hold) stock has declined 15.5% in the past three months, underperforming the industry’s fall of 7.3%.

Image Source: Zacks Investment Research

Quarterly Highlights

Nordstrom posted adjusted earnings of 39 cents per share, up 77.3% from the year-ago reported figure of 22 cents. Yet, the metric missed the Zacks Consensus Estimate of 56 cents per share.

Total revenues grew 17.7% year over year to $3,637 million and beat the Zacks Consensus Estimate of $3,536 million. This marked the fifth straight quarter of sequential top-line growth. Net sales jumped 18% year over year to $3,534 million, while the metric declined 1% from third-quarter fiscal 2019. Credit Card net revenues grew 18.4% from the prior-year quarter to $103 million.

For third-quarter fiscal 2021, net sales for the Nordstrom brand rose 11% year over year to $2,343 million and improved 3% from third-quarter fiscal 2019. Better store traffic and increased consumer spending aided quarterly growth. Strength in home, active, designer, and beauty categories remained upsides, with products including dresses, men's suiting and dress shirts, dress shoes, and makeup witnessing a sequential improvement.

Sales for the Nordstrom Rack brand advanced 35% year over year to $1,191 million but declined 8% from third-quarter fiscal 2019. This was mainly due to low inventory levels in premium brands and core categories such as women's apparel and shoes. Nordstrom Rack is known for offering premium brands at affordable prices. That said, management is making efforts to strengthen Rack's brand awareness and drive traffic. The company launched a new marketing campaign, namely More Reasons to Rack, in September. It expects gains from this endeavor in the fiscal fourth quarter, with a significant improvement in first-half fiscal 2022.

Nordstrom also remains focused on improving supply chain and inventory, accelerating delivery speed, expanding in-store shopping as well as other omni-channel capabilities like same-day and next-day pickup along with increasing labor and fulfillment velocity and throughput in distribution and fulfillment centers to drive top-line growth at both Nordstrom and Nordstrom Rack.

Digital sales fell 12% year over year but rose 20% from the third quarter of fiscal 2019. For the fiscal third quarter, digital sales represented 40% of net sales compared with 54% in the year-ago period.

Nordstrom's gross profit margin expanded 230 basis points (bps) year over year to 35% for the reported quarter. This substantial growth resulted from lower markdowns and leverage from higher net sales. The metric also expanded 80 bps from third-quarter fiscal 2019 on the back of reduced buying and occupancy costs as well as improved merchandise margins.

Ending inventory grew 13% from third-quarter fiscal 2019, owing to forward receipts in order to support early holiday sales and partly offset supply chain backlogs.

Selling, general and administrative (“SG&A”) expenses — as a percentage of sales — expanded 230 bps year over year to 34% for the fiscal third quarter due to higher labor cost, which was somewhat offset by robust sales growth. The metric also expanded 260 bps from third-quarter fiscal 2019 due to higher fulfillment and labor costs, offset by gains from the resetting of cost structures in 2020.

Earnings before interest and taxes (“EBIT”) of $127 million reflected growth of 19.8% from $106 million in the year-ago quarter. The increase was mainly the result of higher sales volume and expanded merchandise margins, which somewhat offset elevated labor cost. EBIT declined $66 million from third-quarter fiscal 2019 due to higher fulfillment and labor costs, offset by gains from the resetting of cost structures in 2020.

Other Financials

Nordstrom ended third-quarter fiscal 2021 with a strong balance sheet. Available liquidity as of Oct 30, 2021 was $867 million, including $267 million of cash and cash equivalents. It had long-term debt (net of current liabilities) of $2,851 million and total shareholders’ equity of $359 million.

As of Oct 30, 2021, the company provided $277 million of net cash for operating activities and spent $361 million as capital expenditure.

Nordstrom, Inc. Price, Consensus and EPS Surprise

Nordstrom, Inc. price-consensus-eps-surprise-chart | Nordstrom, Inc. Quote

Fiscal 2021 Outlook

Despite persistent supply chain issues and higher labor cost, management retained its fiscal 2021 view. The company continues to anticipate revenue growth of more than 35%. It still expects an EBIT margin of 3-3.5% compared with the previously mentioned 3%. Nordstrom predicts supply chain disruptions to persist in the next year.

For the fiscal fourth quarter, the company envisions significant gross margin improvement on a two-year basis driven by lower promotional activity and higher regular price sell-through. SG&A expense related to fulfillment and labor costs is likely to remain high in the fiscal fourth quarter.

Here's How Other Stocks Fared

We have highlighted three top-ranked stocks in the Retail - Wholesale sector, namely, Boot Barn Holdings BOOT, Tractor Supply Company TSCO and Costco COST.

Boot Barn Holdings — the lifestyle retailer of western and work-related footwear, apparel and accessories — currently sports a Zacks Rank #1 (Strong Buy). Shares of the company have rallied 48.5% in the past three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Boot Barn Holdings’ sales and earnings per share (EPS) for the current financial year suggests growth of 54.4% and 183.3%, respectively, from the year-ago period. BOOT has a trailing four-quarter earnings surprise of 35.3%, on average.

Tractor Supply Company, a rural lifestyle retailer in the United States, presently carries a Zacks Rank #1. The company has a trailing four-quarter earnings surprise of 22.8%, on average. Shares of the company have gained 18.6% in the past three months.

The Zacks Consensus Estimate for Tractor Supply Company’s sales and EPS for the current financial year suggests growth of 19% and 23.9%, respectively, from the year-ago period. TSCO has an expected EPS growth rate of 9.6% for three-five years.

Costco, which operates membership warehouses, carries a Zacks Rank #3 at present. The company has a trailing four-quarter earnings surprise of 7.7%, on average. Shares of Costco have gained 19.6% in the past three months.

The Zacks Consensus Estimate for Costco’s sales and EPS for the current financial year suggests growth of 9.6% and 9.7%, respectively, from the year-ago period. COST has an expected EPS growth rate of 8.7% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tractor Supply Company (TSCO) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research