FTSE falls after Biden unveils $1.9 trillion stimulus plan

Louise Moon

·26 min read

Biden Harris - REUTERS/Tom Brenner

Oops!

Something went wrong.

Please try again later.

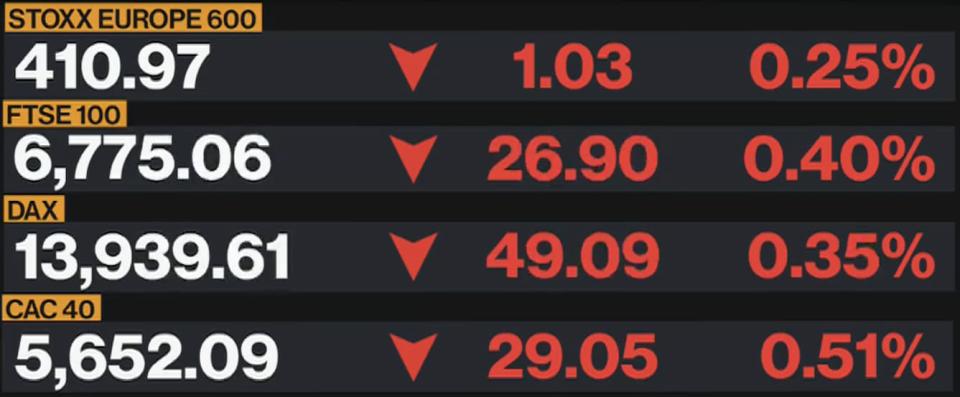

London’s benchmark index shed 1pc on Friday, dropping for the fourth time this week to end the five days down almost 2pc as traders booked profit from gains made in a record start to the year.

UK markets had their best start to the year ever, but the mood shifted to a more quiet tone this week to leave the FTSE 100 ending down 66.3 points yesterday at 6,735.71.

Sentiment was dented by new data showing Britain’s economy contracted 2.6pc in November due to virus curbing measures, to put the economy back on the road to a recession.

This was enough to offset earlier gains on the back of president-elect Joe Biden’s much anticipated $1.9 trillion (£1.4 trillion) stimulus package, which was at the top end of expectations.

Shares of FTSE 250 oilfield services company Petrofac fell to their lowest level since early November last year, shedding 45.9p to 120.8p.

The Serious Fraud Office said late on Thursday that David Lufkin, former global head of sales, had pleaded guilty to three further counts of bribery, as part of an ongoing investigation into Petrofac which it announced in 2017.

Mr Lufkin admitted his role in offering and making corrupt payments to try to win contracts for the firm in the UAE in 2013 and 2014.

He had already pleaded guilty in February 2019 to 11 counts of bribery related to corrupt efforts to win contracts in Iraq and Saudi Arabia and will be sentenced on Feb 11 at Southwark Crown Court.

Petrofac said that “a small number of former Petrofac employees are alleged to have acted together with [Mr Lufkin], although none have been charged.”

It added: “No charges have been brought against any group company or any other officers or employees. No current board member of Petrofac Limited is alleged to have been involved.”

Defence contractor Babcock joined the falls on the domestically focused FTSE 250, due to a pandemic-induced weakness in its aviation business. It reported underlying operating profit declined by a third to £202m in the first nine months of its financial year, while underlying revenue shed 3pc to £3.39bn.

The company said it would not provide full-year guidance as Covid uncertainty has worsened in most of its markets. It fell 43.2p to 220.3p.

David Lockwood, chief executive, said: “While trading in the third quarter has continued to reflect the challenges of the first half and there remain a number of near term uncertainties, the fundamental strengths of the group and the opportunities ahead give us confidence for future years and I look forward to reporting back at the full year results.”

Pharmaceuticals business Indivior gave midcaps some relief and rose 10.3p to 115.3p after raising its sales and profit guidance for the year. It said total net revenue would be between $645m and $650m, against previous guidance of $595m to $620m.

Out of the 15 stocks that rose on the FTSE 100 Aveva was the leader by far, gaining 248p to £38.05.

The engineering and industrial software giant said sales were up 1.5pc in the nine months to the end of December, with recurring revenue up 10pc on the same basis.

Its order pipeline for the rest of the fiscal year looks “solid”, supported by “efficient digital demand generation and several large contract renewals.

Thank you for following along - have a great weekend and see you on Monday!

05:13 PM

Signal experiencing technical difficulties after rise in downloads

Messaging app Signal said it is experiencing technical difficulties and working to restore the service.

The app has seen a rise in downloads after a controversial change in rival messaging app WhatsApp's privacy terms, announced recently. It means users are required to share their data with Facebook and Instagram, prompting a jump to Signal.

Signal is currently one of the top downloaded apps on Apple's app store.

04:58 PM

US stocks continue to lose ground

US stocks are falling for a second day despite a new $1.9tn stimulus package announced by incoming president Joe Biden.

The plan is far from done, as his plan could be watered down under opposition in Congress and there is the possibility taxes could rise to fuel things like benefits and direct payments to households.

Here is how movements stood by around midday in New York, to:

S&P 500: -0.6pc to 3,773.16

Dow Jones: -0.6pc to 30,822.48

Nasdaq: -0.6pc to 13,038.79

Among stocks, Wells Fargo & Co dragged the banking sector after posting uninspiring fourth-quarter results.

Energy and financials pulled the S&P 500 lower, including Exxon Mobil which has dropped 4pc to 48.29 after a report said it is being investigated for overvaluing assets.

04:42 PM

ITV begins to look for a new chairman

ITV

ITV has begun scouring for a new chairman to replace Sir Peter Bazalgette, who will step down next year.

My colleague Ben Woods reports:

The Love Island broadcaster has recruited headhunters from Spencer Stuart to find a successor before he leaves in May 2022.

His departure will bring down the curtain on a near ten-year stint on ITV's board, with three years spent as a non-executive director before replacing Archie Norman as chair.

The move has prompted disappointment from ITV's top investors, reported Sky News, with his departure being driven by corporate governance rules stipulating a chairman should only serve for nine years.

04:29 PM

Standard Chartered to cut hundreds more jobs

SC bank

Standard Chartered is planning further job cuts of several hundred staff globally next month, as the lender continues a restructuring that has been put on hold by the pandemic. It employs 85,000 people around the world.

The London-headquartered bank will focus reductions on the more junior employees, reported Bloomberg.

Standard Chartered, which restarted job cuts in the second half of 2020, is one of a handful of large European banks that have resumed staff reductions in the past months. Others include HSBC and Deutsche Bank.

“A number of roles are being made redundant in line with our commitment to transforming the bank to ensure its future competitiveness, work that has been underway for the last few years,” Standard Chartered said in a statement.

Since July, when it said it was making a small number of roles redundant, senior managers including Didier von Daeniken, the head of its private banking arm, have left.

03:34 PM

Handover

That's all from me for today. My colleague Louise Moon will take over for the rest of the afternoon.

Thanks for following!

03:27 PM

BP board member resigns

BP

BP board member Dame Alison Carnwath has resigned with immediate effect.

My colleague Rachel Milard reports:

The company said she was stepping down for “personal and professional reasons”.

She had been on the board of the FTSE 100 oil and gas giant since May 2018, and was a member of the audit committee.

Carnwath chaired the property developer Land Securities between 2008 and 2018, and has also sat on several boards.

Helge Lund, BP’s chair, said: "On behalf of the board, I would like to thank Alison for the important contribution she has made to BP over the last three years."

03:04 PM

It will cost £100 quid to export your lunch

Filling out the paperwork to get a £2.69 Greggs ham and cheese baguette through customs would take an hour and cost £100, according to an exports firm.

My colleague Alan Tovey reports:

Andrew Iveson, director of Amivet Export, produced mock certificates for the sandwich to highlight the difficulties faced by food exporters after a lorry driver had his lunch seized by Dutch customs officials this week saying it fell foul of new Brexit-related rules.

Mr Iveson said: “This illustrates the farcical situation food exporters are in. For the sandwich we had to download the certificates and fill in six pages to show the traceability of the meat and dairy products they contain, working through vet certificates for the abattoir, the cutting plant, pasteurisation and the hazard charts.

“You can see why a lot of small manufacturers would probably give up.”

Mr Iveson said he wanted to flag the problems in the sector after a video appeared on Dutch TV of a driver having his tinfoil-wrapped ham sandwich confiscated at Holland ferry terminal.

He was told Britain leaving the EU meant he was no longer allowed to bring some foods into Europe, with his request to remove the meat and keep the bread.

A Dutch customs official replied: “No, everything will be confiscated. Welcome to Brexit, sir, I’m sorry.”

Mr Iveson added that the cheese and ham baguette was a “simple example” and that “composite” products are likely to face far more red tape.

“If you have a product with traces of honey, you could find arguing about where the hives were,” he added. Mr Iveson's Cheshire-based company has been providing export advice from qualified vets for 15 years for companies which want to sell meat, dairy and fish products abroad.

He said he had heard "horror stories” about how the new controls are being implemented and was “swamped with a crazy amount of new enquiries from people who have never had to think about this before”.

He added: “We’re being told about different ports of entry interpreting the rules differently, saying you have to fill the forms in different coloured ink, you can’t cross out some sections, that signatures don’t apply and stamps have to be used instead.”

Wall Street opened lower after President-elect Joe Biden announced a new $1.9tn stimulus plan.

US market data - Bloomberg

02:05 PM

Wall Street set to drop at open

With less than half an hour until the US open, Wall Street futures are currently pointing downwards: the S&P 500 is set to drop about 0.5pc at the open, while the tech heavy Nasdaq is set to trade flat. Both indices are trading slightly below record highs.

01:41 PM

Indivior jumps after raising profit and sales forecast

Indivior is leading risers on the FTSE 250 today, after the pharmaceuticals business raised its sales and profit guidance for the full year.

The group said its total net revenue for the year would be between $645m and $650m, versus previous guidance of $595m to $620m. It added:

Based on these preliminary results, the group now expects to deliver adjusted pre-tax income ahead of its previous expectations.

The company said its Sublocade treatment had seen growth of 12pc–18pc in the fourth quarter, with Suboxone also performing resiliently.

01:11 PM

Jack Dorsey: Trump Twitter ban is just the beginning

Jack Dorsey - REUTERS/Toby Melville/File Photo

Jack Dorsey, the boss of social network Twitter, has told staff that efforts to clean up the site will be “much bigger” than just deleting US President Donald Trump's account.

My colleague Matthew Field reports:

The Twitter chief executive told staff that efforts to remove posts and accounts deemed harmful would continue for “the next few weeks and go on beyond the inauguration”.

The leaked remarks follow Tweets earlier this week from Mr Dorsey, who said the banning of President Trump had set a “dangerous precedent” for the site.

A total of 223 jobs have been lost after Marks & Spencer completed its takeover of the stock and marketing assets of clothing brand Jaegar.

Jaegar’s 63 stores and concessions will close permanently, with 22 head office staff and 211 store staff – most of whom were furloughed – set to lose their jobs.

Tony Wright from FRP, which was handling Jaegar’s administration, said:

The transaction with M&S provides a future for this well-known brand and, in competition with a number of bids, has provided the best outcome for creditors. Unfortunately, we will now progress with the permanent closure of the remaining store portfolio and work with the affected staff to access redundancy payment and support.

12:40 PM

JPMorgan posts record profit

JPMorgan boss Jamie Dimon - REUTERS/Jeenah Moon/File Photo

JPMorgan posted a record fourth-quarter profit, sealing 2020 as the best year ever for the US investment bank.

It generated $12.1bn of profit over three months amid a surge in trading and investment banking-related fees.

Chief executive Jamie Dimon said:

While positive vaccine and stimulus developments contributed to these reserve releases this quarter, our credit reserves of over $30 billion continue to reflect significant near-term economic uncertainty and will allow us to withstand an economic environment far worse than the current base forecasts by most economists

JPMorgan’s traders brought in $5.9bn in revenue during the quarter, and the bank release an expectation-busting $3bn of its credit reserves, suggesting a bullish outlook for the coming period.

12:25 PM

Virgin Atlantic sells two planes to fund loan repayment

Virgin Atlantic has sold two of its Boeing 787 jets to fund the repayment of a loan from hedge fund Davidson Kempner Capital Management that underpinned its rescue last year.

Bloomberg has the details:

The planes were bought by Griffin Global Asset Management and Bain Capital Credit, Virgin Atlantic said in a statement Friday. The sale and leaseback deal, which allows the airline to go on operating the aircraft, raised $230 million.

After paying off the balance of the $170 million borrowed from New York-based Davidson Kempner at the height of the coronavirus crisis, Virgin Atlantic will have 70 million pounds ($96 million) left for its own funds.

Khan announces inflation-beating 2.6pc rise in London travel costs

Sadiq Khan - Stefan Rousseau/PA Wire

Sadiq Khan has announced an inflation-busting fare rise for London public transport while delivering a swipe at Boris Johnson's government.

My colleague Oliver Gill reports:

Fares across the capital will increase by 2.6pc from March, 1pc higher than the retail prices index.

The rise was a condition of Westminster agreeing to a £1.8bn bailout of Transport for London last October.

Mr Khan said: “Londoners know that I have done everything possible to make public transport more affordable since I became Mayor – including introducing the unlimited Hopper bus fare and freezing all TfL fares since taking office – saving the average London household over £200.

“Unfortunately this year Ministers insisted on a RPI+1pc fares increase in order for TfL to get the emergency Government support needed as a consequence of the global pandemic.

Petrofac slumps after former executive pleads guilty to bribery offences

Shares in Petrofac have tumbled this morning after David Lufkin, the group’s former head of sales, pleaded guilty to three counts of bribery.

The offences, brought by the Serious Fraud Office, relate to offers and payments made between 2012 and 2018 to influence the award of contracts in the UAE worth about $3.3bn.

They come on top of eleven charges already brought by the SFO, to which Mr Lufkin pleaded guilty in February 2019.

The SFO said its investigation into Petrofac continues.

In a statement, Petrofac said:

Petrofac confirms that no charges have been brought against any Group company or any other officers or employees. A small number of former Petrofac employees are alleged to have acted together with the individual concerned, although none have been charged. No current Board member of Petrofac Limited is alleged to have been involved.

The FTSE 250 company added that it was continuing to engage with the SFO.

Jefferies’ Mark Wilson noted the scandal now covers a greater geographical area, with contracts of a value greater than $7.5bn now affected (compared with more than $4bn before).

11:08 AM

Aveva shares pop as trading improves

Industrial software maker Aveva is leading risers on the FTSE 250 today after reporting revenue growth.

The FTSE 100 group said revenue rose approximately 1.5pc in the nine months to the end of December, with recurring revenue up 10pc on the same basis.

Aveva said its order pipeline for the rest of the fiscal year looks “solid”, supported by “efficient digital demand generation and several large contract renewals, albeit fewer than seen in the third quarter”.

Its board said it remains confident in its full-year outlook, adding that digitalisation across the industrial world leaves it “excited about the significant growth opportunities ahead”.

The company said it expects a takeover of OSIsoft to be completed by early February, with only a foreign investment clearance in the US now needed.

Shares have risen to a three-month high, with Jefferies’ Julian Serafini noting that Aveva had secured a number of three-year contract renewals.

10:40 AM

Court says insurers must cover small business losses

Almost 400,000 small businesses hit by coronavirus lockdowns could be in line for an insurance payout after a Supreme Court ruling on business interruption insurance policies.

My colleague Lucy Burton reports:

The court has “substantially allowed” an appeal brought by the Financial Conduct Authority in a landmark £1.2bn legal battle.

The watchdog last year brought a test case over the wording of business interruption insurance policies, which some insurers argued did not cover the Covid pandemic.

The FCA previously said it was bringing the legal action following “widespread concern” over “the lack of clarity and certainty” for businesses seeking to cover substantial losses incurred by the pandemic and subsequent national lockdown.

European stocks have come off their session lows but remains moderately lower on the day, with a risk-off tone holding across global markets. The pound has dropped 0.4pc against the dollar, erasing yesterday’s gains.

10:01 AM

SFO closes probe into British American Tobacco

The Serious Fraud Office has rolled up a three-year-old probe into reports British American Tobacco has bribed African officials to influence legislation.

In a statement, the investigative body said the case had not met the standards for prosecution, despite an “extensive investigation and a comprehensive review of the available evidence”.

BAT said it was pleased the investigation had been dropped, adding that it: “remains committed to the highest standards in the conduct of its business”.

The SFO said it would “continue to offer assistance to the ongoing investigations of other law enforcement partners”.

09:31 AM

Money round-up

Here are some of the day’s top stories from the Telegraph Money team:

The pound has steadily declined against the dollar this morning amid a general drop in risk appetite following the announcement of Joe Biden’s $1.9 trillion relief package. The dollar has risen against most of its major currency rivals as investors digest the proposals.

08:48 AM

Babcock reports profit drop while Meggit holds steady

Babcock - Will Haigh

Defence contractor Babcock reported falling profits after pandemic-induced weakness in its aviation business continued in its third quarter.

My colleague Simon Foy reports:

Underlying operating profit declined by a third to £202m in the first nine months of its financial year, while underlying revenue fell 3pc to £3.39bn.

The company said it would not provide full-year guidance as Covid uncertainty has worsened in most of its markets.

Chief executive David Lockwood said: “While trading in the third quarter has continued to reflect the challenges of the first half and there remain a number of near term uncertainties, the fundamental strengths of the group and the opportunities ahead give us confidence for future years and I look forward to reporting back at the full year results.”

Meanwhile aerospace parts manufacturer Meggitt said it expects its 2020 results to be in line with previous guidance, adding that the vaccine roll out “provides a supportive backdrop for the recovery” in aviation.

Underlying operating profit for the year is expected to be in the middle of its guidance range of between £180m and £200m, while revenue for 2020 is expected to be around £1.7bn

08:31 AM

Full report: Double-dip fears abound after November contraction

My colleague Tim Wallace has a full report on this morning’s GDP figures. He writes:

Consumer-facing services bore the brunt of the new rules, while the construction and manufacturing industries continued to recover, having learned in the first lockdown how to adjust practices to maintain operations.

The dominant services sector shrank by 3.4pc between October and November, led by a 44pc collapse in output in accommodation and food services, as the battered hospitality industry was forced to close many of its operations again.

European markets have opened lower in the wake of Joe Biden’s stimulus announcement. There’s an element of ‘buy the rumour, sell the fact’ at work here, but markets are likely also pricing in uncertainty about the scale of the plan.

Bloomberg TV - Bloomberg TV

The UK’s better-than-expected GDP figures aren’t likely to be having too much of an impact – they’re old news from a markets perspective, although they may indicate assumptions about the output hit from current lockdowns has been overestimated.

08:09 AM

Gym Group sales cut in half by Covid-19

Sales at the Gym Group plunged by almost half last year after Covid restrictions forced its venues to shut for months.

My colleague Simon Foy reports:

Total revenues plunged by 48pc to £80.5m in 2020, with the company losing 45pc of the trading days in the year due to closure as a result of Government restrictions, it said.

The London-listed fitness operator said memberships declined by more than a quarter to 578,000 during the period.

Chief executive Richard Darwin said: “2020 has been a challenging year for our business, our members and our colleagues. Through the outstanding work of our team we provided a Covid-secure exercise environment for our members and demonstrated the resilience of our business model by trading profitably when gyms have been open.

“At a time when health and fitness has never been more important to the nation, we are ready to emerge from the pandemic and take advantage of the many opportunities available [to] us.”

07:59 AM

UK trade deficit widens

The UK’s trade deficit widened by £0.6bn in November, with a rise in goods important driven mostly but machinery and transport imports underpinning the shift.

Here’s how the three-month trade balance figures look:

The ONS said the jump in imports reflected pre-Brexit jitters, adding:

This increase is consistent with potential stockpiling in preparation for the end of the EU exit transition period. In November, UK carmakers began stockpiling cars and car parts due to uncertainty surrounding UK-EU trade negotiations towards the end of the transition period.

07:47 AM

Food and accommodation output continues to plunge

An industry-by-industry breakdown of November’s output figures showed lockdowns continued to batter the food and accommodation sector, with hotels seeing a drop in reservations and many restaurants and cafes forced to operate on a takeaway-only basis. Output was at less than two-fifths of pre-lockdown levels.

07:34 AM

Reaction: UK economy has developed some lockdown ‘immunity’

November’s comparatively small contraction shows the UK economy has developed “a fair bit of immunity to lockdowns”, says Paul Dales from Capital Economics, which he said should be enough to avoid a double-dip recession. He added:

As long as GDP didn’t fall by 1.0pc m/m or more in December, then the economy wouldn’t have contracted in Q4 as a whole. January’s third lockdown, during which the schools are closed too, will take the level of GDP a bit lower than in November.

But the growing immunity of the economy to lockdowns is encouraging, means that vaccines may allow it to get back to its pre-crisis peak earlier than most had assumed and supports our view that the Bank of England won’t need to resort to negative interest rates.

Samuel Tombs from Pantheon Macroeconomics said the “relatively modest” fall showed that many businesses have adapted well to lockdown conditions. He warned figures for the current period will be more painful:

GDP will be significantly lower in January than in November, because schools have shut during this lockdown and mobility data suggest that fewer people are leaving their home. In addition, manufacturing output likely will fall sharply in January, as the Brexit deadline on December 31 created a strong incentive for overseas customers to bring forward orders to Q4. Nonetheless, most businesses should have fared as well as they did in November.

Pantheon Macroeconomics - Pantheon Macroeconomics

07:26 AM

Consumer facing companies take heaviest hit

The ONS’s breakdown of services output shows consumer-facing services companies were once again the biggest lockdown victim, as people sought to avoid face-to-face interactions and maybe retailers were forced to close their doors.

As this chart shows, consumer-facing services output dropped sharply in November, while the rest of the services sector dipped only slightly:

07:14 AM

Construction output climbs as services struggle

A sector-by-sector breakdown shows UK construction output climbed during November, with builders feeling little impact from the new wave of lockdowns.

Meanwhile, manufacturing and services both saw a dip in output, with the dominant services sector taking the heaviest hit. Its output is currently 9.9pc below February 2020’s levels.

The Office for National Statistics said:

There were falls in output in all 14 services sub-sectors between October and November 2020. The largest contributor to this fall was accommodation and food service activities, followed by wholesale and retail trade, other service activities and arts, entertainment and recreation, because of the reintroduction of restrictions in some parts of the UK. These four sectors accounted for nearly 80pc of the fall in services.

07:07 AM

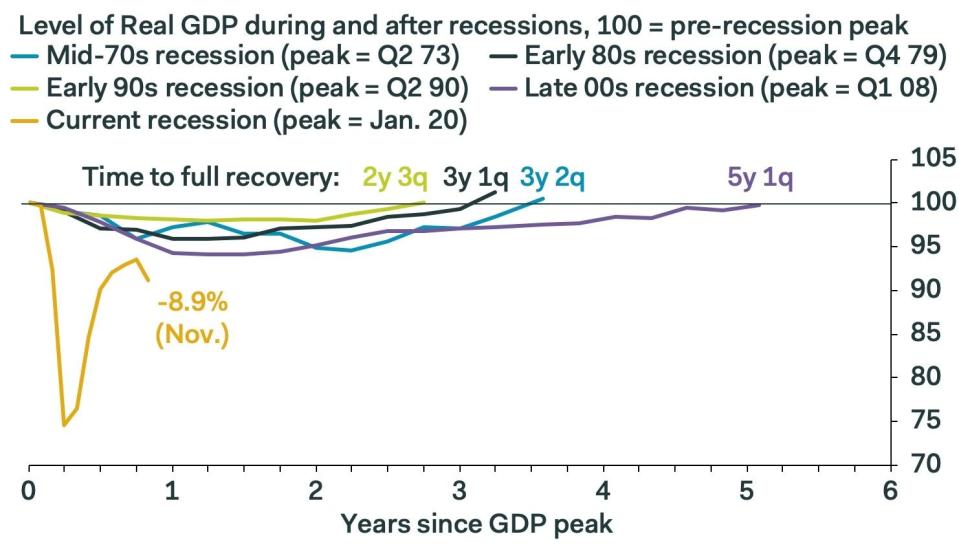

Output at 2013 levels

November’s 2.6pc contraction put UK GDP back at levels last seen in 2013, and almost 9pc below its pre-lockdown peak, as this timeline shows:

07:01 AM

GDP shrank 2.6pc in November

UK GDP shrank by just 2.6pc in November, a result of the the economic damage cause by the second wave of national lockdowns. The drop is smaller than expected, however, and may mean a new quarterly contraction is avoided (although it still looks likely). October’s growth was also revised up, to 0.6pc.

06:56 AM

What economists expect today

After six months of continued but waning growth, November is likely to mark a break point for the UK’s economic recovery, with output expected to drop 4.6pc.

England was in lockdown throughout the month, with tighter restrictions in Scotland, Northern Ireland and Wales also overlapping.

The drop will be nowhere like as severe as the falls seen in March and April: several sectors, such as manufacturing, education and construction, were left comparatively untouched this time around.

November’s drop might also offer a flavour of the size and shape of hit UK GDP is currently taking.

After tepid growth in October, and renewed restrictions in late December, November‘s probable drop is likely to seal Britain into an overall fourth quarter contraction – the ‘double dip’ that has been feared.

06:48 AM

Agenda: November contraction expected

Good morning. European markets are set to dip at the open today, as investors ‘sell the fact’ of President Joe Biden’s $1.9 trillion stimulus package.

But first up, at 7am, we have UK GDP figures for November, which are set to show the second wave of national lockdowns caused a sharp contraction in output.

US equity futures and Treasury yields retreated Friday along with Asian stocks as investors scrutinised President-elect Joe Biden’s much-anticipated $1.9 trillion Covid-19 relief plan. The dollar climbed.

With few surprises to catch investors off guard, attention turned to how much of the package will ultimately get passed by Congress and the possibility that some taxes could rise. Mr Biden’s proposal includes a wave of new spending, more direct payments to households, an expansion of jobless benefits and an enlargement of vaccinations and virus-testing programs.

S&P 500 and European futures slipped and South Korean shares underperformed in Asia. Xiaomi Corp tumbled after the Trump administration blacklisted the Chinese smartphone manufacturer for its military links, along with China National Offshore Oil Corp.

Coming up today

Corporate: Ashmore (Interim results); The Gym Group (Trading statement)

Economics: November GDP, trade balance (UK); trade balance (eurozone); inflation (France, Spain); retail sales, producer prices, industrial production (US)

Jason Fitz and Frank Schwab join forces to recap the draft in the best way they know how: letter grades! Fitz and Frank discuss all 32 teams division by division as they give a snapshot of how fans should be feeling heading into the 2024 season. The duo have key debates on the Dallas Cowboys, New York Giants, New Orleans Saints, Los Angeles Rams, New England Patriots, Las Vegas Raiders and more.

The first electric vehicle I ever drove was a Tesla Roadster in 2011. It was with great anticipation that I slid behind the wheel of the 2025 Acura ZDX Type S. Sure, it's a midsize SUV, but it wears the Type S moniker, a name reserved only for the most fun-to-drive in the Acura stable. On launch, the ZDX will be available in A-Spec and Type S trims -- both of which come equipped with a 102 kWh battery.