Is Now The Time To Put Plaza Retail REIT (TSE:PLZ.UN) On Your Watchlist?

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

In contrast to all that, I prefer to spend time on companies like Plaza Retail REIT (TSE:PLZ.UN), which has not only revenues, but also profits. Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

Check out our latest analysis for Plaza Retail REIT

Plaza Retail REIT's Earnings Per Share Are Growing.

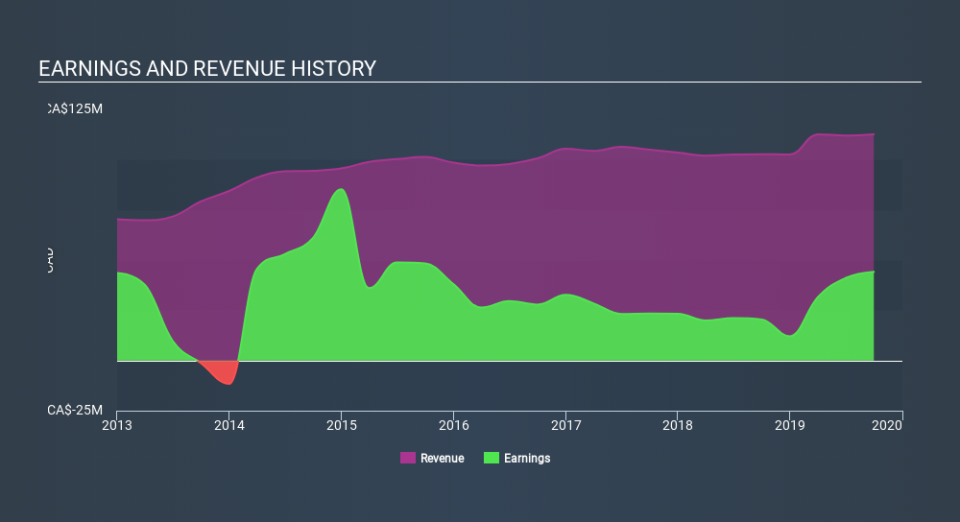

If a company can keep growing earnings per share (EPS) long enough, its share price will eventually follow. That means EPS growth is considered a real positive by most successful long-term investors. Over the last three years, Plaza Retail REIT has grown EPS by 14% per year. That growth rate is fairly good, assuming the company can keep it up.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. Plaza Retail REIT shareholders can take confidence from the fact that EBIT margins are up from 52% to 56%, and revenue is growing. Ticking those two boxes is a good sign of growth, in my book.

In the chart below, you can see how the company has grown earnings, and revenue, over time. For finer detail, click on the image.

While profitability drives the upside, prudent investors always check the balance sheet, too.

Are Plaza Retail REIT Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Any way you look at it Plaza Retail REIT shareholders can gain quiet confidence from the fact that insiders shelled out CA$528k to buy stock, over the last year. And when you consider that there was no insider selling, you can understand why shareholders might believe that lady luck will grace this business. We also note that it was the President, Michael Zakuta, who made the biggest single acquisition, paying CA$92k for shares at about CA$4.19 each.

The good news, alongside the insider buying, for Plaza Retail REIT bulls is that insiders (collectively) have a meaningful investment in the stock. To be specific, they have CA$38m worth of shares. That shows significant buy-in, and may indicate conviction in the business strategy. Those holdings account for over 7.9% of the company; visible skin in the game.

While insiders are apparently happy to hold and accumulate shares, that is just part of the pretty picture. That's because on our analysis the CEO, Michael Zakuta, is paid less than the median for similar sized companies. I discovered that the median total compensation for the CEOs of companies like Plaza Retail REIT with market caps between CA$264m and CA$1.1b is about CA$1.4m.

The Plaza Retail REIT CEO received total compensation of just CA$400k in the year to December 2018. That looks like modest pay to me, and may hint at a certain respect for the interests of shareholders. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of a culture of integrity, in a broader sense.

Should You Add Plaza Retail REIT To Your Watchlist?

One important encouraging feature of Plaza Retail REIT is that it is growing profits. On top of that, we've seen insiders buying shares even though they already own plenty. That makes the company a prime candidate for my watchlist - and arguably a research priority. Now, you could try to make up your mind on Plaza Retail REIT by focusing on just these factors, or you could also consider how its price-to-earnings ratio compares to other companies in its industry.

As a growth investor I do like to see insider buying. But Plaza Retail REIT isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.