Omeros (NASDAQ:OMER) Shareholders Have Enjoyed A 42% Share Price Gain

While Omeros Corporation (NASDAQ:OMER) shareholders are probably generally happy, the stock hasn't had particularly good run recently, with the share price falling 15% in the last quarter. But at least the stock is up over the last five years. In that time, it is up 42%, which isn't bad, but is below the market return of 129%.

Check out our latest analysis for Omeros

Omeros isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually expect strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last 5 years Omeros saw its revenue grow at 27% per year. Even measured against other revenue-focussed companies, that's a good result. It's nice to see shareholders have made a profit, but the gain of 7% over the period isn't that impressive compared to the overall market. That's surprising given the strong revenue growth. It could be that the stock was previously over-priced - but if you're looking for underappreciated growth stocks, these numbers indicate that there might be an opportunity here.

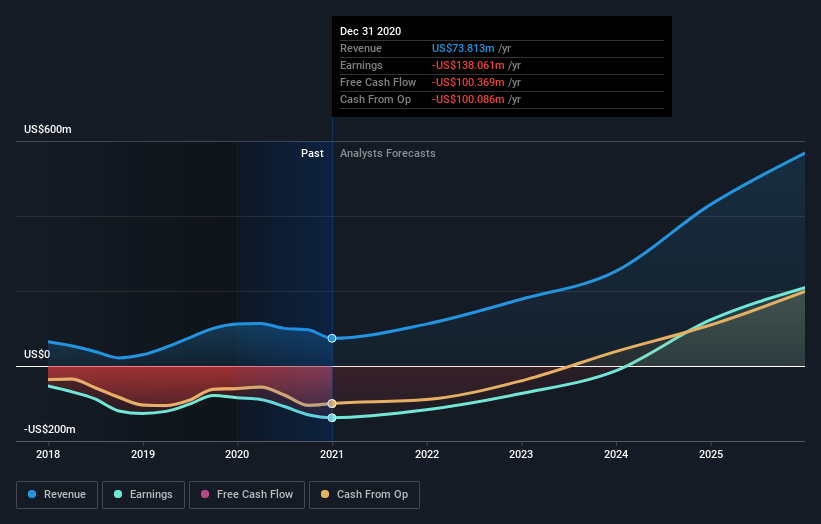

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

This free interactive report on Omeros' balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Omeros shareholders gained a total return of 6.5% during the year. Unfortunately this falls short of the market return. If we look back over five years, the returns are even better, coming in at 7% per year for five years. It's quite possible the business continues to execute with prowess, even as the share price gains are slowing. It's always interesting to track share price performance over the longer term. But to understand Omeros better, we need to consider many other factors. Take risks, for example - Omeros has 4 warning signs (and 1 which shouldn't be ignored) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.