Should You Be Pleased About The CEO Pay At Water Oasis Group Limited's (HKG:1161)

Alan Tam became the CEO of Water Oasis Group Limited (HKG:1161) in 2017. First, this article will compare CEO compensation with compensation at similar sized companies. After that, we will consider the growth in the business. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

See our latest analysis for Water Oasis Group

How Does Alan Tam's Compensation Compare With Similar Sized Companies?

According to our data, Water Oasis Group Limited has a market capitalization of HK$538m, and paid its CEO total annual compensation worth HK$6.0m over the year to September 2019. We think total compensation is more important but we note that the CEO salary is lower, at HK$4.3m. We examined a group of similar sized companies, with market capitalizations of below HK$1.6b. The median CEO total compensation in that group is HK$1.8m.

Next, let's break down remuneration compositions to understand how the industry and company compare with each other. On a sector level, around 80% of total compensation represents salary and 20% is other remuneration. Water Oasis Group does not set aside a larger portion of remuneration in the form of salary, maintaining the same rate as the wider market.

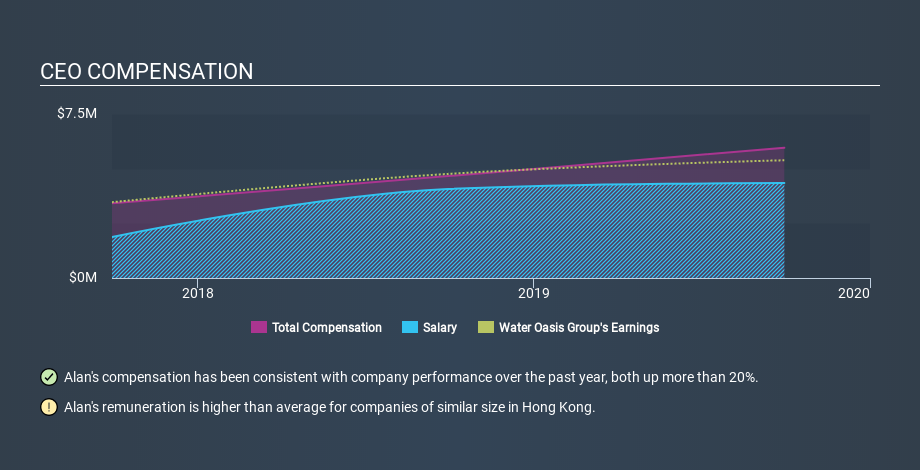

As you can see, Alan Tam is paid more than the median CEO pay at companies of a similar size, in the same market. However, this does not necessarily mean Water Oasis Group Limited is paying too much. We can better assess whether the pay is overly generous by looking into the underlying business performance. You can see a visual representation of the CEO compensation at Water Oasis Group, below.

Is Water Oasis Group Limited Growing?

Over the last three years Water Oasis Group Limited has seen earnings per share (EPS) move in a positive direction by an average of 34% per year (using a line of best fit). Its revenue is up 7.9% over last year.

This shows that the company has improved itself over the last few years. Good news for shareholders. It's nice to see a little revenue growth, as this is consistent with healthy business conditions. We don't have analyst forecasts, but shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Water Oasis Group Limited Been A Good Investment?

With a total shareholder return of 20% over three years, Water Oasis Group Limited shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

We compared total CEO remuneration at Water Oasis Group Limited with the amount paid at companies with a similar market capitalization. We found that it pays well over the median amount paid in the benchmark group.

However we must not forget that the EPS growth has been very strong over three years. We also think investors are doing ok, over the same time period. So, considering the EPS growth we do not wish to criticize the level of CEO compensation, though we'd recommend further research on management. Moving away from CEO compensation for the moment, we've identified 3 warning signs for Water Oasis Group that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.