Is Port of Tauranga (NZSE:POT) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Port of Tauranga Limited (NZSE:POT) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Port of Tauranga

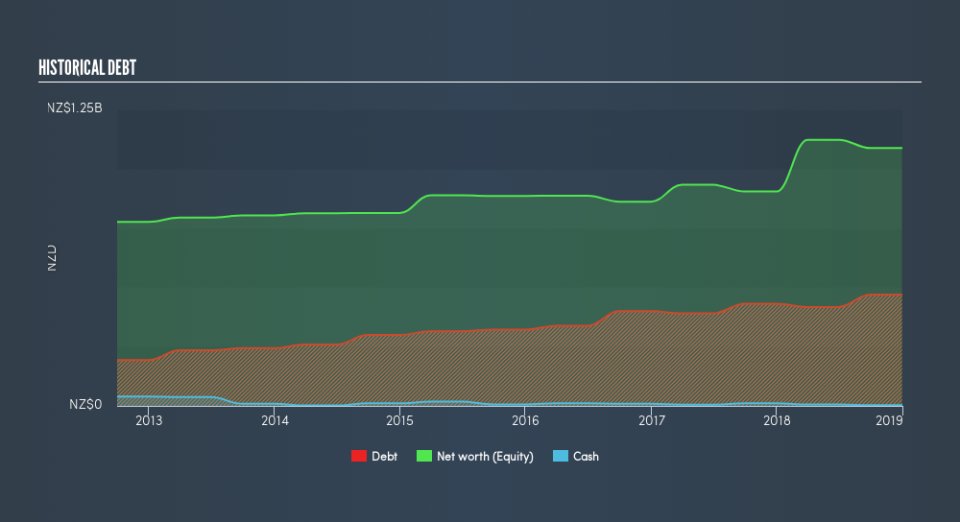

What Is Port of Tauranga's Debt?

The image below, which you can click on for greater detail, shows that at December 2018 Port of Tauranga had debt of NZ$469.1m, up from NZ$431.0m in one year. Net debt is about the same, since the it doesn't have much cash.

How Healthy Is Port of Tauranga's Balance Sheet?

According to the last reported balance sheet, Port of Tauranga had liabilities of NZ$321.5m due within 12 months, and liabilities of NZ$259.8m due beyond 12 months. On the other hand, it had cash of NZ$3.19m and NZ$58.0m worth of receivables due within a year. So it has liabilities totalling NZ$520.1m more than its cash and near-term receivables, combined.

Of course, Port of Tauranga has a market capitalization of NZ$4.09b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With net debt to EBITDA of 2.9 Port of Tauranga has a fairly noticeable amount of debt. On the plus side, its EBIT was 7.6 times its interest expense, and its net debt to EBITDA, was quite high, at 2.9. One way Port of Tauranga could vanquish its debt would be if it stops borrowing more but conitinues to grow EBIT at around 10%, as it did over the last year. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Port of Tauranga's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Port of Tauranga's free cash flow amounted to 36% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Port of Tauranga's interest cover was a real positive on this analysis, as was its EBIT growth rate. On the other hand, its net debt to EBITDA makes us a little less comfortable about its debt. It's also worth noting that Port of Tauranga is in the Infrastructure industry, which is often considered to be quite defensive. Considering this range of data points, we think Port of Tauranga is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. Over time, share prices tend to follow earnings per share, so if you're interested in Port of Tauranga, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.