Why Putting 20% Down on a Mortgage May Be a Mistake

When you put 20% down on the purchase of a home, you don’t have to borrow as much money as someone whose down payment is only 5% or 10%. And as a result, your monthly mortgage payment may be considerably lower. But 20% down payments, while common, are by no means mandatory or the norm. In fact, the National Association of Realtors says the median down payment in 2020 was just 12%. So if you are hoping to save for retirement in addition to buying a home, you could opt for a 10% down payment and invest the remaining cash. Your monthly payments and interest will be higher, but your invested assets will grow into a substantial nest egg over the next 30 years. Let’s compare how a 10% and 20% down payments could affect your retirement.

If you need to figure out how big your down payment should be, a financial advisor may be able to help you decide.

Parameters of Our Comparison

There are several parameters that we’ll base our analysis on. First, the median sales price of a home in the United States is currently $374,900, but we’ll use a $375,000 property for simplicity’s sake. In both scenarios below we’ll assume you have $75,000 in cash for a down payment and/or investing.

Next, we’ll assume a 3% interest rate for the mortgage, which is more or less the current national average. Our analysis also won’t include property taxes or homeowner’s insurance, but it will include private mortgage insurance. This surcharge, known as PMI, will apply to the mortgage that uses a 10% down payment.

Lastly, we’ll assume that any hypothetical money invested in the stock market will average a 10% annual rate of return, since that’s the approximate historical average of the stock market. We’ll also assume monthly compounding.

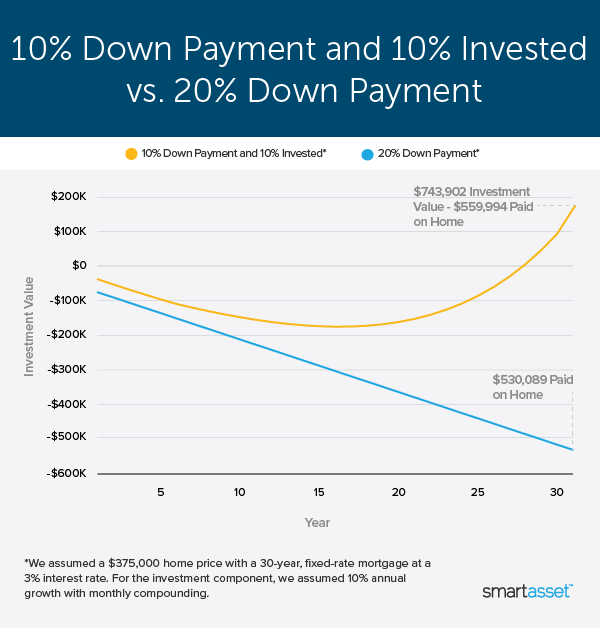

On the outset, if you just consider costs over time, it may seem that the 20% down option is the winner, as shown in the comparison chart below. But it’s more nuanced a decision than that.

Option 1: Put Down the Full 20%

By opting for a 20% down payment ($75,000), you will pay less in interest and avoid PMI, resulting in lower monthly payments. After 30 years of making regular monthly payments, you will have spent a total of $530,089 (remember, this excludes property taxes and homeowner’s insurance).

See the breakdown below:

30-Year Outlook for 20% Down Payment Home Price Down Payment Loan Amount Monthly Payment Total PMI Paid Interest Paid Over 30 Years Total Investment $375,000 $75,000 $300,000 $1,265 $0 $155,089 $530,089 Option 2: Put 10% Down and Invest the Rest

Putting 10% down on a $375,000 home means taking out a larger mortgage ($337,500) and also paying $175 per month in PMI. The PMI payments will eventually end, but they will total more than $10,000. After 30 years of making regular monthly payments, you will have spent a total of $559,994.

See the breakdown below:

Cost of Mortgage With 10% Down Payment Home Price Down Payment Loan Amount Monthly Payment Total PMI Paid Interest Paid Over 30 Years Total Investment $375,000 $37,500 $337,500 $1,598 $10,519 $174,475 $559,994

By putting 10% down instead of 20%, you’ll have an extra $37,500 to invest in the stock market. Here’s a look at how that money could grow over a 30-year period (the SmartAsset Investment Calculator compounds interest monthly):

Retirement Savings Principal Investment Monthly Contributions Term Total $37,500 $0 30 years $743,902

Even without making monthly contributions to your brokerage account, putting 10% down and investing the remaining $37,500 will result in a sizable nest egg by the time your mortgage is fully paid. Assuming a 10% annual rate of return, the $37,500 would grow to $743,902 after 30 years. It’s important to note that while this hypothetical 10% rate of return is based on historical average of the S&P 500, investment returns have been even more robust in recent years. In fact, the benchmark’s total returns have exceeded 11% in nine of the last 12 years, including 31.5% in 2019.

Below, you can see another way of comparing the two scenarios. Yes, the smaller down payment of 10% means the mortgage ultimately costs you more over the life of the loan – about $30,000 more, between PMI and higher mortgage payments. But if the $37,500 you put in the stock market grows at the historic average of 10% per year, it will turn into nearly $750,000 by the time you finish paying off your mortgage. While both of these scenarios end with a fully paid-off house, of course, the person who chose to invest half the down payment ends up with more money in his investment account than he ultimately paid for the home.

The Verdict

The answer appears fairly obvious. Putting 10% down and investing the remaining 10% seems a far better financial move in the long run than putting 20% down, right? Not so fast.

While the 20% down payment will result in less interest paid over the life of the mortgage, it also will also mean lower monthly payments ($333 less per month). Rather than spend that extra money, a shrewd investor would use it to build their retirement nest egg. Investing $333 each month would leave you with a whopping $752,742 after 30 years, assuming the same 10% average rate of return. Not only would you save $30,000 in interest and PMI by putting 20% down versus 10%, you would amass an even larger nest egg by investing your monthly savings.

So that settles it, right? Not exactly.

There’s an even savvier option. While putting less than 10% down would leave you paying PMI each month, that surcharge would presumably disappear once you’ve paid the equivalent of your 20% down payment. In our example, your monthly PMI would be $175. After approximately five years of making monthly payments, you would reach the 20% equity threshold and PMI would disappear, leaving you with an extra $175 every month.

At this point, your initial $37,500 investment would have grown to $61,699 in the market. Contributing the $175 that you were using to pay PMI each month would supercharge your savings, helping it grow to $976,097 by the time the mortgage is paid off. Even though your mortgage would cost you an extra $30,000, this option nets nearly $1 million in retirement savings, by far the largest net egg.

Bottom Line

Buying a home and saving for retirement don’t need to be mutually exclusive. Whether you choose to make a 20% down payment or put 10% down, there are ways to invest extra cash. In both scenarios, consistently investing money that would otherwise pay for PMI has a huge impact in the long run. The best option we found is to put 10% down, invest the remaining cash and then contribute $175 to your brokerage account each month once PMI is paid off.

Homebuying Tips

Need a mortgage and don’t know where to start your search? SmartAsset can help you find a mortgage rate based on where you’re looking to buy a home, your budget and other factors. Get started now.

A financial advisor can help guide you through major financial decisions, like buying a home. Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

Photo credit: ©iStock.com/Jamakosy, ©iStock.com/pinkomelet, ©iStock.com/dragana991

The post This One Chart Shows Why Putting 20% Down on a Mortgage May Be a Mistake appeared first on SmartAsset Blog.