Quest Diagnostics' (DGX) Base Business Grows Despite Margin Woes

Quest Diagnostics Incorporated DGX has been gaining from strong year-over-year growth in its base business, signifying industry-wide recovery. The company raised the lower end of its revenue view and upped the earnings expectations, instilling optimism. However, market headwinds and stiff competition remain concerns. The stock currently carries a Zacks Rank #3 (Hold).

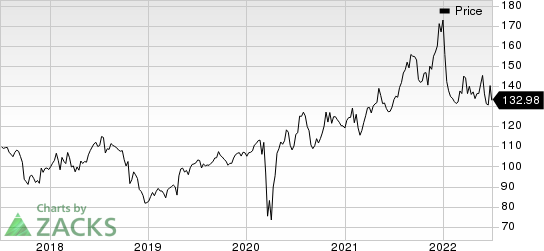

Over the past year, Quest Diagnostics has outperformed its industry. The stock has gained 3.5% against a 40% decline of the industry.

Quest Diagnostics posted better-than-expected first-quarter earnings. The company noted that its base business showcased strong year-over-year growth during the quarter. Quest Diagnostics specifically noted that it has continued to make progress in its base business, executing its two-point strategy to accelerate growth and drive operational excellence. Quest Diagnostics’ health plan revenues without COVID-19 grew faster than its overall base business growth in the quarter. With a bullish expectation for the remainder of 2022, the company raised its full-year guidance.

In terms of the Protecting Access to Medicare Act (“PAMA”), the company earlier noted that it is optimistic about the recent MedPAC report mandated under the LAB Act. This MedPAC report found it feasible to change the CMS data collection process to a statistically valid sample of private payer rates for independent labs, hospital labs and physician office labs. Earlier, during its fourth-quarter earnings call, the company noted that the delay of the 2022 PAMA cuts announced last year was a good outcome for industry and Medicare beneficiaries. Earlier, PAMA cuts of nearly $80 million were expected in 2022, but are now delayed by a year until 2023.

Quest Diagnostics Incorporated Price

Quest Diagnostics Incorporated price | Quest Diagnostics Incorporated Quote

Quest Diagnostics’ base testing volumes or base business refers to testing volumes excluding COVID-19 testing. The company’s legacy base business grew more than 6.3% in the first quarter of 2022. The company noted that it has continued to make inroads in Q1 with its health plans, gaining share and increasing revenues faster than the market. Quest Diagnostics’ health plan revenues without COVID-19 grew faster than its overall base business performance in Q1.

The company also has relationships with payers through value-based contracting. Currently, it has about 30% of its health plan revenues tied to value-based elements, and these include patient health outcomes, quality or shared savings. Quest Diagnostics believes it could grow this to about 50% over the next few years.

On the flip side, in the first quarter of 2022, Quest Diagnostics reported revenues missing the Zacks Consensus Estimate. Further, there has been a year-over-year decline in revenues and adjusted earnings due to lower COVID-19 testing demand. According to the company, COVID-19 volumes remained strong early in the first quarter and decreased in February and March, in line with the market.

The year-over-year contraction in margins is also worrying. Gross margin was 36.9%, reflecting a 326-basis-point (bps) contraction from the year-ago figure. Adjusted operating margin of 20.7% showed a 458-bps contraction year over year.

Pressure on volume, owing to a difficult macro-economic situation and pricing, constitutes the primary risk for Quest Diagnostics. Diagnostic information service volume in the first quarter was roughly flat on an organic basis. COVID-19 testing volumes declined through the month of February and into March. Revenue per requisition declined 5.2% due to lower COVID-19 molecular testing volume.

Key Picks

A few better-ranked stocks in the broader medical space that investors can consider are AMN Healthcare Services, Inc. AMN, Novo Nordisk NVO and Omnicell, Inc. OMCL.

AMN Healthcare has a long-term earnings growth rate of 1.1%. The company surpassed earnings estimates in the trailing four quarters, delivering a surprise of 15.6%, on average. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

AMN Healthcare has outperformed its industry in the past year. AMN has gained 18.2% against the industry’s 50.8% fall.

Novo Nordisk has a long-term earnings growth rate of 14.5%. The company surpassed earnings estimates in the trailing four quarters, delivering a surprise of 7.6%, on average. It currently has a Zacks Rank #2 (Buy).

Novo Nordisk has outperformed its industry in the past year. NVO has gained 31.2% against the industry’s 19.3% growth.

Omnicell has an estimated long-term growth rate of 20%. Omnicell’s earnings surpassed estimates in three of the trailing four quarters and missed the same in the other, the average beat being 13.4%. It carries a Zacks Rank #2 at present.

Omnicell has outperformed its industry in the past year. OMCL has lost 17.9% compared with the industry’s 56.3% fall over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Novo Nordisk AS (NVO) : Free Stock Analysis Report

Quest Diagnostics Incorporated (DGX) : Free Stock Analysis Report

Omnicell, Inc. (OMCL) : Free Stock Analysis Report

AMN Healthcare Services Inc (AMN) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research