Read This Before Buying InterDigital, Inc. (NASDAQ:IDCC) For Its Dividend

Could InterDigital, Inc. (NASDAQ:IDCC) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

With a 2.4% yield and a nine-year payment history, investors probably think InterDigital looks like a reliable dividend stock. While the yield may not look too great, the relatively long payment history is interesting. The company also returned around 14% of its market capitalisation to shareholders in the form of stock buybacks over the past year. Some simple analysis can reduce the risk of holding InterDigital for its dividend, and we'll focus on the most important aspects below.

Explore this interactive chart for our latest analysis on InterDigital!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Looking at the data, we can see that 559% of InterDigital's profits were paid out as dividends in the last 12 months. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. InterDigital paid out 1128% of its free cash flow last year, which we think is concerning if cash flows do not improve. Paying out such a high percentage of cash flow suggests that the dividend was funded from either cash at bank or by borrowing, neither of which is desirable over the long term. Cash is slightly more important than profit from a dividend perspective, but given InterDigital's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

With a strong net cash balance, InterDigital investors may not have much to worry about in the near term from a dividend perspective.

Consider getting our latest analysis on InterDigital's financial position here.

Dividend Volatility

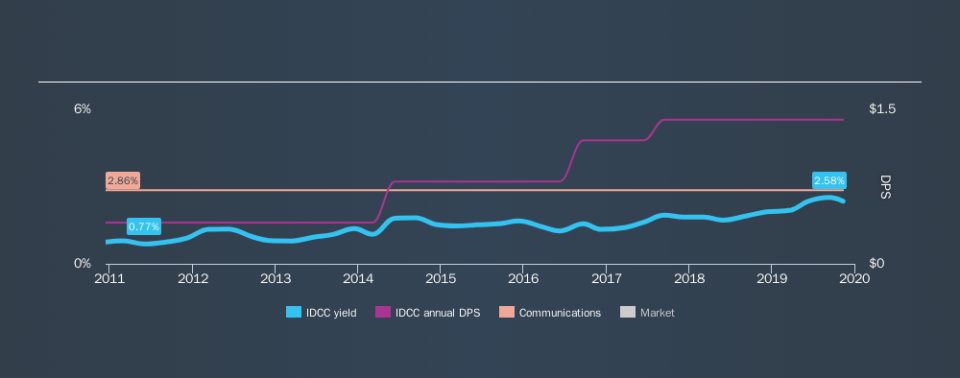

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. The first recorded dividend for InterDigital, in the last decade, was nine years ago. The dividend has been quite stable over the past nine years, which is great to see - although we usually like to see the dividend maintained for a decade before giving it full marks, though. During the past nine-year period, the first annual payment was US$0.40 in 2010, compared to US$1.40 last year. Dividends per share have grown at approximately 15% per year over this time.

InterDigital has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

Dividend Growth Potential

Dividend payments have been consistent over the past few years, but we should always check if earnings per share (EPS) are growing, as this will help maintain the purchasing power of the dividend. Over the past five years, it looks as though InterDigital's EPS have declined at around 23% a year. A sharp decline in earnings per share is not great from from a dividend perspective, as even conservative payout ratios can come under pressure if earnings fall far enough.

Conclusion

To summarise, shareholders should always check that InterDigital's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. InterDigital paid out almost all of its cash flow and profit as dividends, leaving little to reinvest in the business. Second, earnings per share have been in decline, and the dividend history is shorter than we'd like. Using these criteria, InterDigital looks quite suboptimal from a dividend investment perspective.

Given that earnings are not growing, the dividend does not look nearly so attractive. Very few businesses see earnings consistently shrink year after year in perpetuity though, and so it might be worth seeing what the 5 analysts we track are forecasting for the future.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.