Rishi Sunak's five-year tax raid after Covid crisis

- Oops!Something went wrong.Please try again later.

Rishi Sunak on Wednesday announced a five-year personal tax raid that will bring in more than £21 billion as the bill for vast Government spending during the Covid pandemic was laid bare.

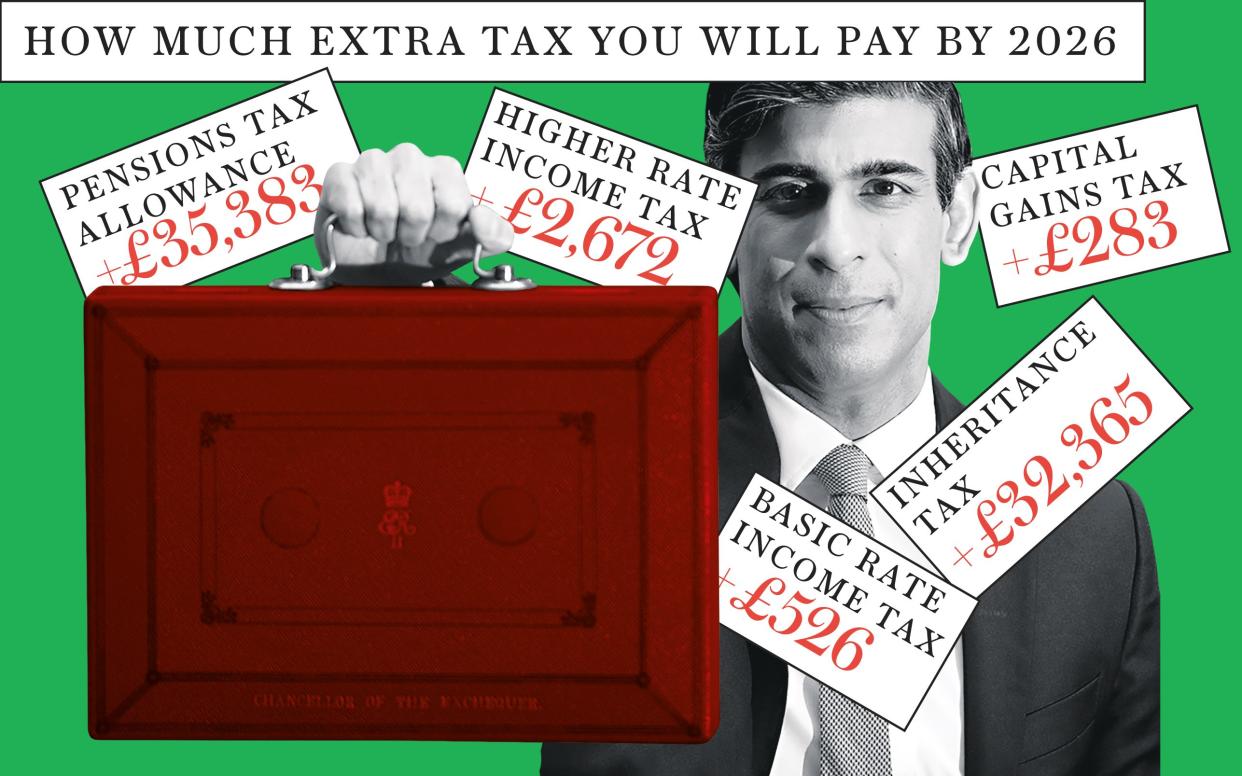

The Chancellor froze thresholds for income tax, inheritance tax, capital gains tax and the pensions lifetime allowance, meaning millions of people will pay more to the Treasury.

Mr Sunak said corporation tax would jump from 19 per cent to 25 per cent in April 2023, although most smaller businesses will be spared the rise.

Revealing his Budget in the House of Commons, he did not hide from the tax hikes, saying: "I recognise they might not be popular. But they are honest." It means Britain now has a tax burden higher than at any time since the 1960s, according to the Office for Budget Responsibility (OBR).

The Government's total Covid economic support was pushed beyond £350 billion as furlough and other major relief schemes were extended to the autumn.

Meanwhile, the UK now has its highest level of borrowing since the Second World War following a 10 per cent shrinking of the economy that was the largest fall in 300 years.

The changes to income tax thresholds mean a basic rate payer will hand over £526 more by 2025-26 than they would have done. A higher rate taxpayer will be paying £2,672 over the five-year period.

Mr Sunak's announcements together amount to the "biggest tax-raising Budget" since 1993, according to influential think tank the Institute for Fiscal Studies (IFS). Paul Johnson, the IFS director, said the Budget confirmed that "we are in a new phase of UK economic history".

Some Conservative MPs warned that the corporation tax rise would stifle investment needed to help the recovery – but, in the hours after the Budget, the Tory backlash in public was limited.

Mark Harper, the chairman of the Covid Recovery Group, told the Commons: "The tax rises in this Budget are going to leave us with the highest tax burden in my lifetime, since before I was born.

"But I hope they will be temporary, that once we have got the public finances back into shape then the Chancellor, as he himself says, is a low-tax Conservative, he'll be able to look to continue increasing public spending in line with the growth of the economy – but also be able to reduce taxes so people can keep more of their hard-earned income, which is central to being a Conservative."

The tax raid, framed around Mr Sunak "levelling" with voters about the state of the country's finances, was matched with continued high spending to autumn and better economic news.

The Chancellor extended flagship programmes designed to help people through Covid financial hardship to September, including the furlough scheme and the Universal Credit uplift.

The business rates holiday for the retail, hospitality and leisure sectors and a VAT reduction for tourism will now remain for the whole year, although support will taper off.

There was also a boost for home buyers, with the stamp duty freeze extended so deals on the brink of completion do not collapse and mortgage support so people can buy a home with a deposit of just five per cent of the sale price.

Some £65 billion in new measures to protect the economy in response to the pandemic was announced, taking the total cost of Covid economic support to £352 billion.

Justifying the support to people and businesses impacted by Covid-triggered lockdowns, Mr Sunak said: "I said I would do whatever it takes, I have done and I will do so."

There were optimistic signs amid grim figures showing the huge hit the pandemic has had on British economy, in part due to the rapid Covid vaccine rollout. Independent fiscal watchdog the Office for Budget Responsibility (OBR) said the economy will return to its pre-Covid level by the middle of next year, six months earlier than forecast.

"The rapid rollout of effective vaccines offers hope of a swifter and more sustained economic recovery," the OBR's economic and fiscal outlook report read.

Unemployment will continue to rise but its rate will peak at 6.5 per cent in late 2021, rather than the 11.9 per cent forecast last summer, meaning 1.8 million fewer people out of work. However, debt is forecast to continue rising, peaking at 97.1 per cent of GDP in 2023-24 before falling a little in the following two years.

In what was at times a sobering message in his Budget speech, Mr Sunak said: "Our borrowing is the highest it has been outside of wartime. It's going to take this country – and the whole world – a long time to recover from this extraordinary economic situation. But we will recover."

The biggest personal tax rise came on income tax. The Chancellor did not raise the rate, which would have broken the Conservatives' 2019 manifesto promise not to raise the rate of income tax, National Insurance and VAT.

Instead, as The Telegraph revealed last month, he chose to freeze the thresholds above which people pay 20 per cent and 40 per cent income tax. The lower threshold will rise to £12,570 and then remain there until April 2026. The higher will rise to £50,270 before also being frozen until that date.

The decision to stop the thresholds rising with inflation means 1.3 million new people will be dragged into the 20 per cent tax band and one million into the 40 per cent band by 2025-26. The move does not break the letter of the Tory manifesto pledge, but leaves the party open to accusations that it breaches its spirit.

Such policies are often described as "stealth" tax raids because the tax rate is not being raised yet billions of pounds – in this case around £19 billion by 2025-26 – flow into the Treasury, but Mr Sunak told the Commons: "We are not hiding it.

"I am here, explaining it to the House, and it is in the Budget document in black and white. It is a tax policy that is progressive and fair."

On the business front, there were two especially eye-catching measures. Corporation tax will rise from 19 per cent to 25 per cent – the first time the rate has been raised since Dennis Healey did so in his 1974 Budget, according to the OBR.

However, 70 per cent of companies – around 1.4 million – will be unaffected because Mr Sunak is bringing in a new "small profits rate". Businesses with annual profits of £50,000 or less will continue to pay the 19 per cent rate, with only those with a quarter of a million in annual profits paying the 25 per cent rate.

The second big business tax measure is what has been called the "super deduction", designed to trigger a wave of investment by allowing companies investing in new plant and machinery assets to deduct 130 per cent of that investment from their taxable income for the next two years.

David Davis, the Tory MP and former Brexit Secretary, said: "This issue about tax increases is not a Tory ideological issue, it is about what delivers the recovery." He said the corporation tax rise would "suppress investment", adding: "We have to worry about tax increases."

However the Conservative back benches did not erupt in protest during the Commons debate that followed, with many MPs welcoming the package.