A Rising Share Price Has Us Looking Closely At China Health Group Inc.'s (HKG:8225) P/E Ratio

China Health Group (HKG:8225) shares have had a really impressive month, gaining 42%, after some slippage. But shareholders may not all be feeling jubilant, since the share price is still down 36% in the last year.

Assuming no other changes, a sharply higher share price makes a stock less attractive to potential buyers. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). So some would prefer to hold off buying when there is a lot of optimism towards a stock. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

View our latest analysis for China Health Group

How Does China Health Group's P/E Ratio Compare To Its Peers?

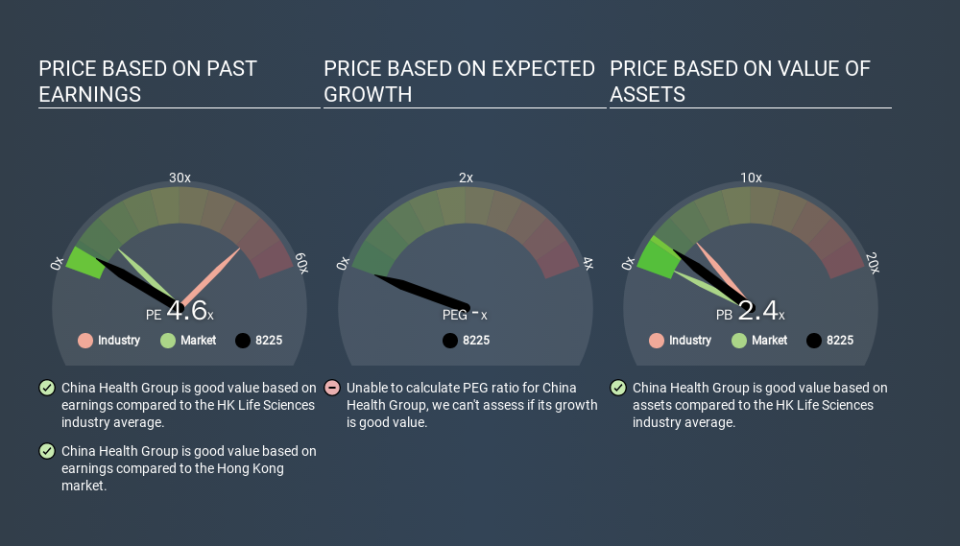

We can tell from its P/E ratio of 4.60 that sentiment around China Health Group isn't particularly high. The image below shows that China Health Group has a lower P/E than the average (49.4) P/E for companies in the life sciences industry.

This suggests that market participants think China Health Group will underperform other companies in its industry. Many investors like to buy stocks when the market is pessimistic about their prospects. It is arguably worth checking if insiders are buying shares, because that might imply they believe the stock is undervalued.

How Growth Rates Impact P/E Ratios

Earnings growth rates have a big influence on P/E ratios. Earnings growth means that in the future the 'E' will be higher. And in that case, the P/E ratio itself will drop rather quickly. Then, a lower P/E should attract more buyers, pushing the share price up.

China Health Group's earnings per share fell by 33% in the last twelve months.

Remember: P/E Ratios Don't Consider The Balance Sheet

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. That means it doesn't take debt or cash into account. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

China Health Group's Balance Sheet

Since China Health Group holds net cash of CN¥459k, it can spend on growth, justifying a higher P/E ratio than otherwise.

The Bottom Line On China Health Group's P/E Ratio

China Health Group's P/E is 4.6 which is below average (10.2) in the HK market. The recent drop in earnings per share would almost certainly temper expectations, but the net cash position means the company has time to improve: if so, the low P/E could be an opportunity. What we know for sure is that investors are becoming less uncomfortable about China Health Group's prospects, since they have pushed its P/E ratio from 3.2 to 4.6 over the last month. For those who like to invest in turnarounds, that might mean it's time to put the stock on a watchlist, or research it. But others might consider the opportunity to have passed.

Investors have an opportunity when market expectations about a stock are wrong. If the reality for a company is not as bad as the P/E ratio indicates, then the share price should increase as the market realizes this. We don't have analyst forecasts, but shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Of course you might be able to find a better stock than China Health Group. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.