Robinson Europe S.A. (WSE:RBS): Commentary On Fundamentals

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

As an investor, I look for investments which does not compromise one fundamental factor for another. By this I mean, I look at stocks holistically, from their financial health to their future outlook. In the case of Robinson Europe S.A. (WSE:RBS), it is a financially-healthy company with a a strong history of performance, trading at a great value. Below is a brief commentary on these key aspects. For those interested in digger a bit deeper into my commentary, take a look at the report on Robinson Europe here.

Good value with proven track record

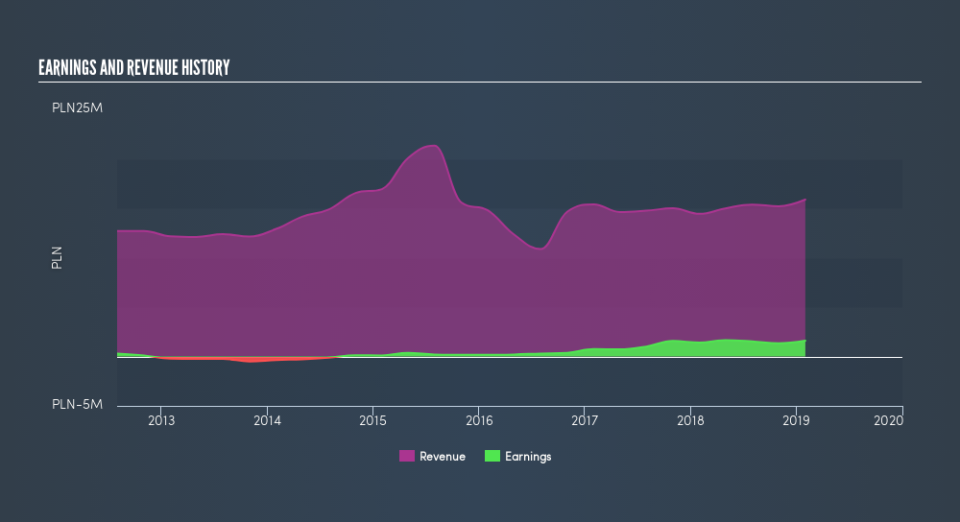

RBS delivered a satisfying double-digit returns of 10.0% in the most recent year Unsurprisingly, RBS surpassed the industry return of 6.4%, which gives us more confidence of the company's capacity to drive earnings going forward. RBS's ability to maintain an adequate level of cash to meet upcoming liabilities is a good sign for its financial health. This indicates that RBS has sufficient cash flows and proper cash management in place, which is an important determinant of the company’s health. With a debt-to-equity ratio of 26%, RBS’s debt level is acceptable. This implies that RBS has a healthy balance between taking advantage of low cost debt funding as well as sufficient financial flexibility without succumbing to the strict terms of debt.

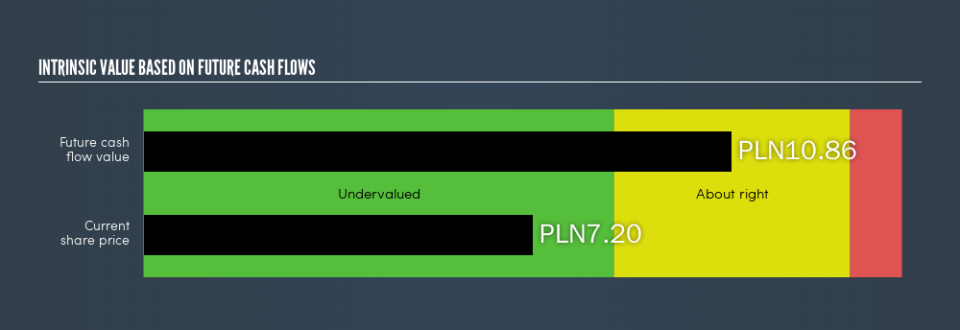

RBS's share price is trading at below its true value, meaning that the market sentiment for the stock is currently bearish. According to my intrinsic value of the stock, which is driven by analyst consensus forecast of RBS's earnings, investors now have the opportunity to buy into the stock to reap capital gains. Compared to the rest of the retail distributors industry, RBS is also trading below its peers, relative to earnings generated. This supports the theory that RBS is potentially underpriced.

Next Steps:

For Robinson Europe, there are three fundamental factors you should further research:

Future Outlook: What are well-informed industry analysts predicting for RBS’s future growth? Take a look at our free research report of analyst consensus for RBS’s outlook.

Dividend Income vs Capital Gains: Does RBS return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from RBS as an investment.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of RBS? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.