Russia’s Assertive Foreign Policy Threatens Longer-term Economic and Reform Outlook

The Russian administration seems to be ignoring a likely short-lived opportunity for simultaneously addressing the nation’s structural economic challenges while also improving economic ties with the EU, Russia’s most important trading partner. Windfall gains from today’s elevated energy prices could have been greater, were the Nord Stream 2 gas pipeline in operation, while the outlook for attracting foreign capital and reducing sanctions risks would also have improved were it not for the crisis surrounding Ukraine.

Russia’s strengthened public finances and accumulation of foreign-exchange and fiscal reserves have enabled a more self-sufficient economy to withstand international sanctions over the recent past and pull through the Covid-19 crisis comparatively well. Higher oil prices have allowed the government to support short-run economic recovery with emergency fiscal stimulus. The Russian economy will grow an above-trend 2.7% in 2022 after an estimated 4.5% in 2021. However, growth projections for this year face substantive downside risk should the Ukraine crisis escalate.

Scope upgraded Russia’s long-term credit rating to BBB+/Stable last year, based on a strengthened sovereign balance sheet against sanction risks.

Rising energy prices might have set scene for better Russia-EU relations

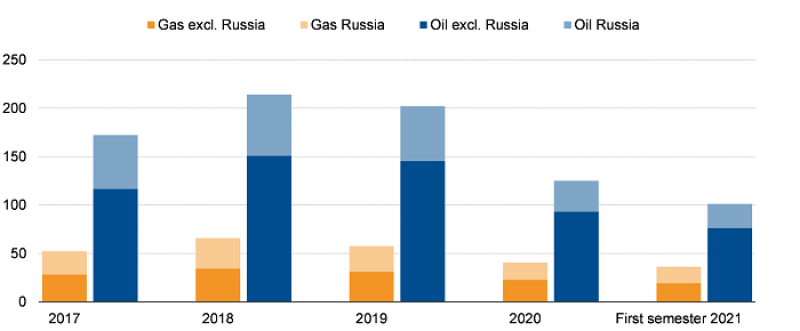

Current high oil and gas prices could have set the stage for improved relations with Europe considering the EU’s current reliance on energy imports from Russia, acknowledging that this geopolitical advantage may diminish over the long term as Europe gradually transitions away from fossil fuels. The planned inclusion of some natural gas in the EU Taxonomy implies that gas will play a larger role as a main transition fuel during the EU’s transition into a low carbon economy.

Instead, Russian policies have helped push energy security and sustainability faster and further up the policy-making agenda in Europe. Thus, the leverage that Russia has long held over Western Europe through the region’s reliance on imports of Russian energy products now could have an earlier expiry date.

Figure 1. EU imports of crude oil and natural gas

EUR bn

Significant potential economic, financial costs for Russia from US, EU tensions

The deterioration in relations with the EU and the US could potentially have significant costs for Russia’s energy sector, banking system and real economy in terms of rouble convertibility as well as for top Russian officials if Washington and Brussels impose tougher sanctions. Such geopolitical and sanction-related risks represent a main constraint on Russia’s credit rating. Existing sanctions and risk of more to come have discouraged foreign investment. Inbound foreign direct investment fell from an annual average of USD 55bn over 2010-13 to around USD 20bn over 2018-21.

The economic context under which Russia is pressing claims on the West has also changed.

First, Russian exports to the EU could be materially affected by the EU’s proposition of a carbon border adjustment mechanism. Mitigating financial consequences of such an EU carbon levy, which might be expanded to include Russian oil and gas, hinges on a lenient approach from Brussels – something that appears unlikely in the current diplomatic climate.

Russia needs to tackle long-term economic, environmental, social challenges

Secondly, the Russian administration’s lack of far-reaching reform to curtail economic reliance on energy exports is one manifestation of an intensification of economic, environmental and social challenges.

Transforming Russia’s economic model requires more than fiscal prudence and protecting the value of the rouble. More profound reform ought to aim at reducing the state’s significant role in the economy, which has discouraged competition and aggravated outstanding inefficiencies in addition to social inequalities, clouding the business climate and discouraging private investment. In the absence of reform, growth potential over the medium run will remain tepid at around 1.5-2% annually, despite comparatively low per capita incomes and significant economic catch-up potential.

Chances that the government embarks on substantive reform near term are low. Reforms are politically costly, if only because of the competitiveness of Russia’s energy sector compared with that of other tradable sectors in the short term.

For further reading, please see: Central & Eastern Europe Sovereign Outlook 2022 (published Dec 2021)

For a look at all of today’s economic events, check out our economic calendar.

By Levon Kameryan, Senior Analyst, Scope Ratings

Levon Kameryan is Senior Analyst in Sovereign and Public Sector ratings at Scope Ratings GmbH

This article was originally posted on FX Empire