Russian Oil Embargo: Europe Faces Manageable Cost Squeeze; Russia’s Long-run Growth Prospects Worsen

The embargo agreed by the EU comes as Russia’s war in the Ukraine and the war’s impact on aggravating inflation have already diminished the region’s growth prospects for this year and next. We revised down growth projections for the EU’s central and eastern Europe region to 2-3% for 2022, from a December forecast of 4.6%. Similarly, growth in Germany is projected to moderate to 2.3% this year (our December forecast for this year was 4.4%), recovering to only 3% in 2023.

Downside risks to said macro views remain high in case of further intensification of inflationary pressure or evidence that core inflation has become further entrenched. Further significant fiscal support near term is likely even though most governments have already announced budgetary support measures to help cushion households and businesses from rising energy prices and broader inflationary pressure.

The EU’s move increases risk that Russia will expand economic retaliatory measures

The EU’s move significantly increases risk that Russia will expand economic reprisal against EU member states, including through further interruption of energy supplies before the EU’s boycott takes on full effect.

Medium run, pressure on public finances, already stretched by the pandemic crisis, will rise as governments foot part of the bill for the building of alternative energy infrastructure, from storage facilities to new renewable and nuclear generating capacities to natural gas distribution networks.

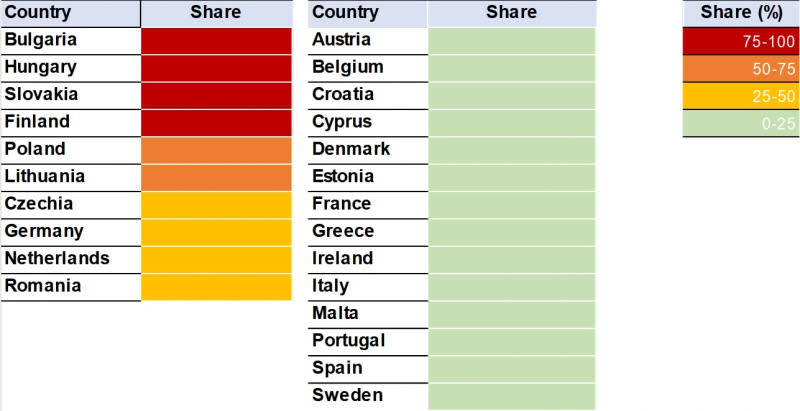

A temporary exemption for the Druzhba pipeline through central and eastern Europe illustrates difficulties of finding a consistent EU approach under current EU rules when individual countries are particularly dependent upon Russian energy (Figure 1). While this reduces overall effectiveness of sanctions, it does not signal a broader lack of political commitment on the part of the EU as three quarters of Russian oil imports to the EU will be impacted immediately, rising to 90% by end-2022.

Reaching agreement will prove even more challenging when gas embargos are considered.

Figure 1. The reliance on Russian oil varies across the EU

Share (%) of Russia in national extra-EU imports of oil, 2021

Energy crisis highlights urgency for the EU of creating an energy union for its member states

The energy crisis highlights an urgency for the EU of creating an energy union for its member states to better coordinate countries’ energy policies and enhance energy security. This, however, will prove challenging given differing starting points in terms of an underlying energy mix.

Europe has relatively good oil-import, transport and storage infrastructure and crude is more easily sourced from other regions given international oil markets are more liquid than natural gas markets. Cutting reliance on Russian oil imports is therefore easier than cutting natural gas.

Improved diversification of energy supplies and climate agenda ought to enhance EU energy security

Longer term, the improved diversification of energy supplies coupled with realisation of an ambitious climate change agenda ought to help enhance the EU’s energy security and sustainability of energy supplies.

For Russia, the embargo could drive oil prices even higher, but any export gains will be partially offset by the steep discounts Russian oil producers will have to offer to buyers located in Asia – principally in China and India – in order to compensate for risk of secondary sanctions and cost of developing new infrastructure.

For Europe, completely replacing Russia is out of reach any time soon

A complete replacement of the European market for Russia is out of reach any time soon, especially given EU and UK plans to ban Russian oil insurance. Firstly, Russia’s energy infrastructure is predominantly geared towards the west. Immediate expansion of pipeline oil supplies to China is limited due to capacity constraints.

Secondly, oil has historically been much more important than gas for Russia’s state finances, hence greater effectiveness from an EU perspective of an oil rather than a gas embargo. Last year, oil and gas together generated 36% of Russian federal budget revenue (and 48% over the first four months of this year), with oil accounting for 80% of this total. The embargo raises costs for Russia’s energy sector and real economy not least in terms of rouble convertibility longer run.

Nevertheless, Russia has generated more export revenue from gas than oil since escalation of this war due to soaring gas prices and discounts on Russian crude – income which could be, moving ahead, used to support the domestic economy. In the first four months of 2022, Russia’s federal budget collected 50% of RUB 9.5trn (or USD 132bn) in oil and gas revenue planned for the year.

For a look at all of today’s economic events, check out our economic calendar.

Levon Kameryan is Associate Director in Sovereign and Public Sector ratings at Scope Ratings GmbH. Eiko Sievert, Director in Sovereign and Public Sector ratings at Scope Ratings, contributed to writing this commentary.

This article was originally posted on FX Empire

More From FXEMPIRE:

Ireland sticking to forecast for budget deficit this year -minister

Silver Weekly Price Forecast – Silver Markets Continue to Be Choppy

S&P 500 Weekly Price Forecast – The S&P 500 Continues to Show Caution

Amazon’s CEO of Worldwide Consumer to step down after 23 years

Gold Weekly Price Forecast – Gold Markets Continue to Show Volatility