The Shady Crypto Startup Selling ‘Shares’ in Celebs

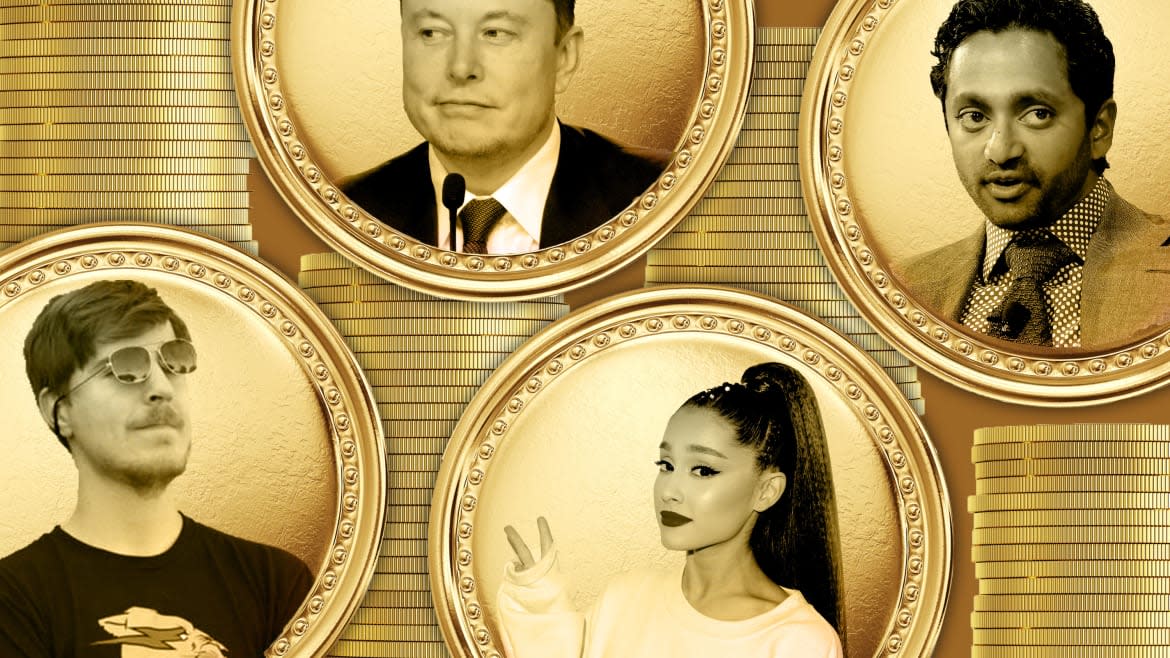

In late March, a 23-year-old named Alex Masmej logged on to Twitter to learn he had been turned into a currency. On a new social-networking platform called BitClout, anyone with access to bitcoin could, in just a few steps, buy something called the “alexmasmej” coin. A handful of people already had—there were about 24 coins in circulation. By BitClout’s metric, a piece of Alex cost about $250.

This was not an entirely new experience for Masmej. Last year, after losing his job in the pandemic, he’d minted his own coin called the $ALEX token, selling what amounted to shares in his life. The first $ALEX investors to help Masmej raise $20,000 would get 15 percent of his income for the next three years; at times, they could vote on his everyday decisions. In concept, the BitClout coin was similar, but with a key difference: He’d had nothing to do with it.

“BitClout does not ask for consent,” Masmej told the Daily Beast. “[It] is trading on your name without you knowing… People really don’t like this, and that makes sense because it seems almost illegal.”

The platform, which has become a source of anger and bemusement in the pockets of the internet that pay attention to new crypto projects, operates sort of like a monetized Twitter. BitClout lets people speculate on prominent social-media figures, buying personalized tokens that theoretically rise and fall in value with the person’s popularity. The combination of hype technology and celebrity proved attractive to investors, raising over $165 million from Andreessen Horowitz, the Winklevoss twins, and Reddit co-founder Alexis Ohanian. But the project’s critics, of which there are many, see it as a dystopian ploy to commodify human interaction, in the mode of a “Yelp for people.”

Masmej wasn’t the only one to find himself minted into money. When BitClout launched out of private beta on March 24, some 14,000 users had pre-made profiles on the platform, copied from their Twitter accounts and converted into markets for individualized coins, nearly all without approval. Elon Musk, the top-ranked token on the website, runs for about $77,000; Ariana Grande goes for just under $25,000. Donald Trump, who places slightly below Barstool Sports’ Dave Portnoy (about $17,000), trades for nearly $15,700.

Masmej found the platform funny, but others were not as entertained. The crypto-focused law firm Anderson Kill sent BitClout a cease-and-desist on behalf of a product manager at the token exchange Radar Relay, calling for his likeness to be removed from the site. “It is well established that a person or company cannot knowingly use ‘another’s name, voice, signature, photograph or likeness… for purposes of advertising or selling... without such person’s prior consent,” the letter reads, citing the right of publicity under California Civil Code 3344. The account was removed, but users can still technically buy its coin by searching for the original username.

The premise of BitClout is fairly straightforward. Traders exchange bitcoin for the site’s native currency, BitClout, which they must spend to register an account, send messages, or post. They can also use the currency to buy “Creator Coins,” which are individualized tokens issued for prominent personalities. The more people buy a given Creator Coin, the more its value rises, and vice-versa. “It’s literally tokenized clout,” said Brian Fakhoury, a crypto investor who has written about the platform. “The more clout you have, the more your thing is worth.”

The site is set up to capitalize on the clout of its users, requiring the most well-known accounts to engage in a bit of unpaid advertising. Figures like Masmej, whose profiles were pre-made on the site, can claim their accounts and issue tokens on their own behalf—but only if they buy BitClout and tweet about the platform. Very few people have done this. One source who reviewed the website’s backend said about 80 profiles on the platform had been claimed.

Should I claim my Bitclout?

— Snoop Dogg (@SnoopDogg) April 7, 2021

Just joined #BitClout! Excited to be a part of a new platform in the crypto space. Follow me at: https://t.co/XMkeLVV5oC

BC1YLiySbpLp3y6q279SQXPgLZPqQoMxKHE9ToqDFk56jE9kwbF4gXE— Tiffany Ariana Trump (@TiffanyATrump) April 7, 2021

BitClout’s launch arrived on the heels of the craze over NFTs, or “non-fungible tokens,” cryptographic units of data stored on a blockchain that can be minted in a range of formats—Jack Dorsey turned his first tweet into an NFT; Kings of Leon released an album as one—and sold off for increasingly outrageous prices. BitClout operates on a similar premise: minting tokens that market hype as a way to directly pay creators. But while NFTs are not mutually interchangeable—the owner of Dorsey’s tweet NFT cannot trade it for another version—BitClout is. Like a dollar, the token can be exchanged for other BitClout. It’s a fungible token.

“The underlying force of NFTs is the exact same thing that drives BitClout,” Fakhoury said. “But it’s the same thing at the end of the day. They’re kind of worthless assets that people give value to for no underlying reason.”

Between NFTs, now BitClout, sometimes I wonder if we’re living in a simulation 🤖 Things will only get weirder from here .. 👽

— Abigail Ratchford (@AbiRatchford) April 3, 2021

When it launched, BitClout’s creator tried to remain anonymous, identifying himself only as “Diamondhands”—a slang term for someone who holds on to their financial position fiercely—in the mold of bitcoin’s pseudonymous inventor, Satoshi Nakamoto. But the attempt at secrecy crumbled quickly, when industry insiders pointed to a man named Nader Al-Naji, who later confirmed his identity to the trade publication Decrypt. (Al-Naji did not respond to The Daily Beast’s request for comment.)

A former Google engineer from Alexandria, Virginia, Al-Naji made a splash in the crypto-world back in 2018 with a project called Basis. The idea was to create what’s called a “stable coin”—a token whose value is pegged to a more reliable currency, like the U.S. dollar—but to establish that stability with an algorithm, rather than backing it with actual money. Al-Naji raised a record $133 million in seed funding, but the concept proved unsustainable. After the Securities and Exchange Commission got involved, Basis shut down and returned its remaining money to investors.

The failure left Al-Naji with a mixed reputation: a founder who stumbled, but didn’t steal. And yet the launch of BitClout, which one investor described to Decrypt as “fucked up,” has struck many as a scam. The biggest red flag, beyond the glaring consent issue, is that while users can put money into BitClout, they cannot get it out. Traders send bitcoin to a single account run by the BitClout team—the exact ownership of which remains unknown—but it’s a one-way transaction. The currency does not trade on any exchanges and there’s no way to cash out on the website.

Anyone looking to actually profit from their trades on BitClout has to take more surreptitious measures. Aravind Karthigeyan, a high-school student and moderator of a BitClout subreddit, told The Daily Beast he’s gotten around this by reselling his tokens at a discount to individual buyers on the messaging app, Telegram.

For James Prestwich, a crypto engineer and founder who has been publicly critical of BitClout, this represents a clear indication that the currency is a shitcoin—crypto jargon for a scam. “The only way to get bitcoin or dollars out is to find another person and to negotiate a bespoke deal with them,” he said. “So BitClout users, once they get in, they’re trapped. There’s no way out.”

“There is a secondary market that’s developed on Telegram. On Telegram, OTC (over-the-counter) BitClout is usually a 40 to 50 percent discount,” Prestwich said. “So if you want to get out, you’re taking a 40 percent haircut, and the only way to do it is to manually send the BitClout to someone and hope they pay you.”

Critics have also cast doubt on the platform’s security. “They are very opaque,” Masmej said, “It’s very hard to get to the BitClout website… and even then, it’s really hard on the platform to know how much they’re getting in fees or what exactly to do to sign up. We have to pay bitcoin, but we don’t really know what it’s for. I think a lot of communities in crypto are really pissed off.”

Most crypto projects issue users a “private key”—often a long phrase or string of random characters—to access their accounts. Unlike a password, private keys can’t be changed. The risk is that if someone else figures out a private key, the user can’t make a new one to keep them out of the account. “If somebody gets your private key, you literally can’t do anything with your account,” Fakhoury said. “It is just forever compromised.”

BitClout also issues private keys, but when users log in, it caches the keys in whatever browser they’re using. As a result, the keys are more vulnerable to theft—if the user clicks on a scammy phishing link and signs in, their key could be stolen. “There’s a big security risk in the private keys just sitting directly in your browser,” Fakhoury said.

For Prestwich, the more jarring revelation was that BitClout also stores the keys on its own server, uploading the data after every transaction. “It’s not just that they’re insecurely storing keys, but they’re sending them to themselves,” Prestwich said. “They could take all of the BitClout at any time or make arbitrary purchases on your behalf. Any BitClout you have, any employee that has access to that server can take it at any time.”

Rather than launching the platform on a ready-made blockchain like the bitcoin-rival ethereum, which has templates for minting new tokens using its own infrastructure, BitClout chose to develop its protocol from scratch. As a result, it was not initially a blockchain—where multiple servers run the same algorithm and register transactions simultaneously—but a single block or “node” operated off one server.

In its white paper, BitClout claims that other users are running nodes. And the project maintains that it is open-source, meaning anyone interested could theoretically download the source code, create a node of their own, and extend the chain. But BitClout’s creator has not released the source code. “There does seem to be a blockchain there,” Prestwich said, “a poorly constructed, poorly thought out blockchain. I would suspect that there are other people who have a close relationship with BitClout who are running other nodes.”

As an investor, Fakhoury was skeptical of the project’s execution, but found the concept exciting.

“I think it’s a genius idea,” he said. “BitClout just opened Pandora’s box. It opens the door to now ‘Oh, I see this YouTuber is getting popular. I know they’re gonna get more popular now and I have a way to financially benefit from that.’”

Masmej, who has not claimed his profile because he only uses ethereum, said his peers were less impressed. “I asked my friends in crypto and they were like ‘Dude, this is a chain for boomers,’” he said. “They are only on bitcoin, this is not going to work, and they are impersonating people’s Twitter accounts.’”

Prestwich agreed: “This is not the cool, hot crypto-startup. This is people who are part of the establishment trying to imitate some of the hot crypto-startups in order to make money.”

Got a tip? Send it to The Daily Beast here

Get our top stories in your inbox every day. Sign up now!

Daily Beast Membership: Beast Inside goes deeper on the stories that matter to you. Learn more.