Shandong Weigao Group Medical Polymer (HKG:1066) Seems To Use Debt Rather Sparingly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Shandong Weigao Group Medical Polymer Company Limited (HKG:1066) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Shandong Weigao Group Medical Polymer

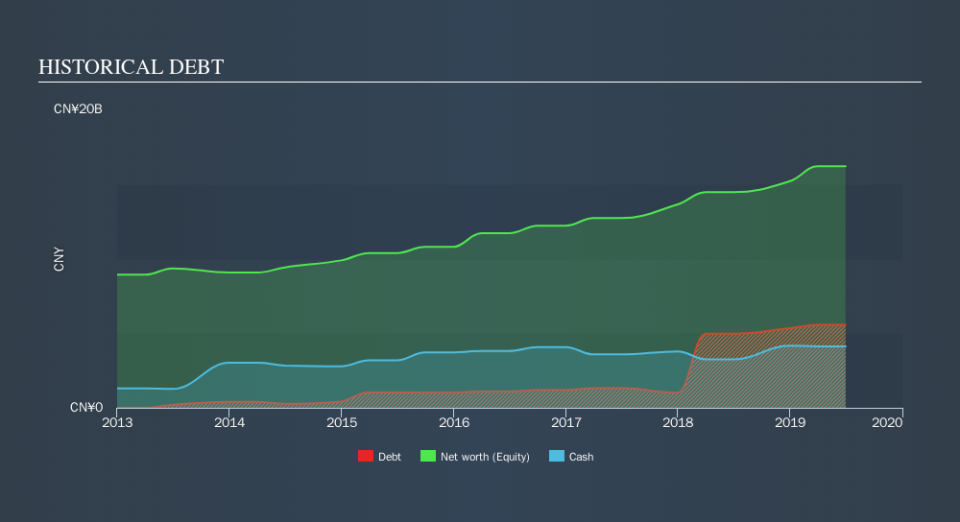

What Is Shandong Weigao Group Medical Polymer's Debt?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Shandong Weigao Group Medical Polymer had CN¥5.57b of debt, an increase on CN¥4.97b, over one year. However, it does have CN¥4.12b in cash offsetting this, leading to net debt of about CN¥1.45b.

A Look At Shandong Weigao Group Medical Polymer's Liabilities

According to the last reported balance sheet, Shandong Weigao Group Medical Polymer had liabilities of CN¥3.90b due within 12 months, and liabilities of CN¥4.96b due beyond 12 months. On the other hand, it had cash of CN¥4.12b and CN¥5.36b worth of receivables due within a year. So it actually has CN¥627.6m more liquid assets than total liabilities.

This state of affairs indicates that Shandong Weigao Group Medical Polymer's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the CN¥34.2b company is short on cash, but still worth keeping an eye on the balance sheet.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Shandong Weigao Group Medical Polymer's net debt is only 0.54 times its EBITDA. And its EBIT easily covers its interest expense, being 18.6 times the size. So we're pretty relaxed about its super-conservative use of debt. Another good sign is that Shandong Weigao Group Medical Polymer has been able to increase its EBIT by 28% in twelve months, making it easier to pay down debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Shandong Weigao Group Medical Polymer's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Shandong Weigao Group Medical Polymer recorded free cash flow worth 51% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Happily, Shandong Weigao Group Medical Polymer's impressive interest cover implies it has the upper hand on its debt. And the good news does not stop there, as its EBIT growth rate also supports that impression! We would also note that Medical Equipment industry companies like Shandong Weigao Group Medical Polymer commonly do use debt without problems. Considering this range of factors, it seems to us that Shandong Weigao Group Medical Polymer is quite prudent with its debt, and the risks seem well managed. So we're not worried about the use of a little leverage on the balance sheet. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Shandong Weigao Group Medical Polymer's earnings per share history for free.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.