Is Shougang Concord Century Holdings (HKG:103) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Shougang Concord Century Holdings Limited (HKG:103) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Shougang Concord Century Holdings

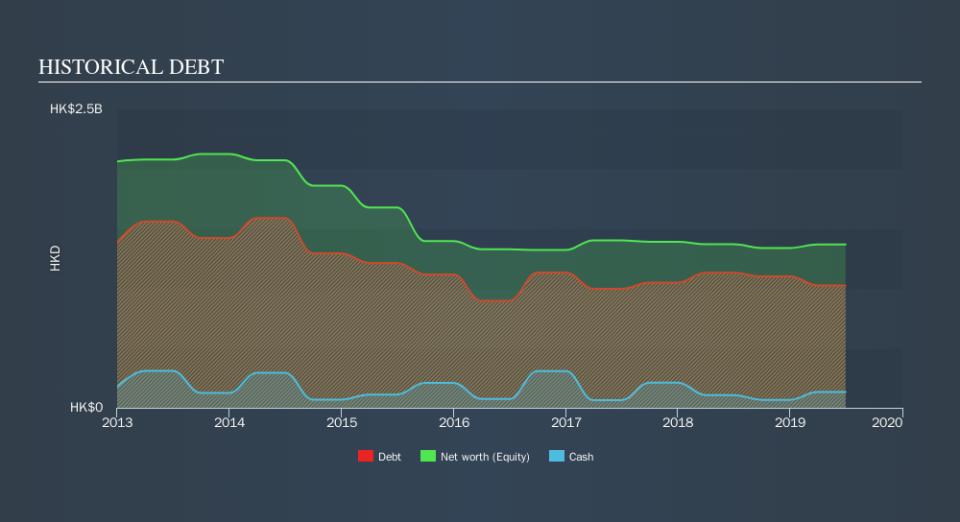

What Is Shougang Concord Century Holdings's Debt?

As you can see below, Shougang Concord Century Holdings had HK$1.03b of debt at June 2019, down from HK$1.13b a year prior. However, it also had HK$131.7m in cash, and so its net debt is HK$893.7m.

A Look At Shougang Concord Century Holdings's Liabilities

The latest balance sheet data shows that Shougang Concord Century Holdings had liabilities of HK$1.67b due within a year, and liabilities of HK$240.3m falling due after that. Offsetting these obligations, it had cash of HK$131.7m as well as receivables valued at HK$1.60b due within 12 months. So it has liabilities totalling HK$186.0m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of HK$282.7m, so it does suggest shareholders should keep an eye on Shougang Concord Century Holdings's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Shougang Concord Century Holdings's debt to EBITDA ratio (3.6) suggests that it uses some debt, its interest cover is very weak, at 2.5, suggesting high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. One redeeming factor for Shougang Concord Century Holdings is that it turned last year's EBIT loss into a gain of HK$133m, over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Shougang Concord Century Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, Shougang Concord Century Holdings generated free cash flow amounting to a very robust 100% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

Shougang Concord Century Holdings's interest cover and net debt to EBITDA definitely weigh on it, in our esteem. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Shougang Concord Century Holdings is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.