Sonova Holding (VTX:SOON) Could Easily Take On More Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Sonova Holding AG (VTX:SOON) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Sonova Holding

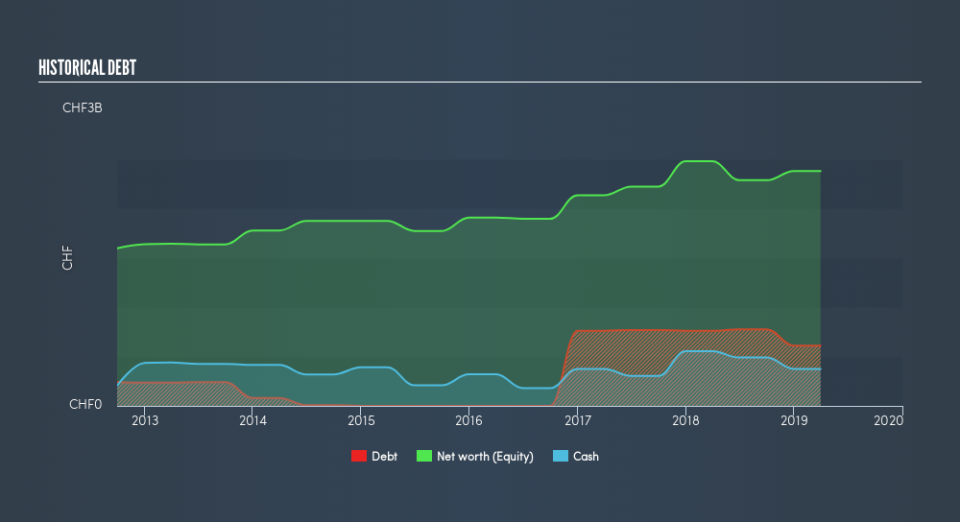

What Is Sonova Holding's Net Debt?

As you can see below, Sonova Holding had CHF609.9m of debt at March 2019, down from CHF759.4m a year prior. However, because it has a cash reserve of CHF374.8m, its net debt is less, at about CHF235.1m.

How Strong Is Sonova Holding's Balance Sheet?

We can see from the most recent balance sheet that Sonova Holding had liabilities of CHF1.03b falling due within a year, and liabilities of CHF886.3m due beyond that. On the other hand, it had cash of CHF374.8m and CHF612.4m worth of receivables due within a year. So it has liabilities totalling CHF929.2m more than its cash and near-term receivables, combined.

Given Sonova Holding has a humongous market capitalization of CHF14.7b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Sonova Holding has a low net debt to EBITDA ratio of only 0.36. And its EBIT covers its interest expense a whopping 5k times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, Sonova Holding grew its EBIT by 9.8% in the last year, making that debt load look even more manageable. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Sonova Holding's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Sonova Holding generated free cash flow amounting to a very robust 86% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that Sonova Holding's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that's just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. We would also note that Medical Equipment industry companies like Sonova Holding commonly do use debt without problems. Considering this range of factors, it seems to us that Sonova Holding is quite prudent with its debt, and the risks seem well managed. So the balance sheet looks pretty healthy, to us. Over time, share prices tend to follow earnings per share, so if you're interested in Sonova Holding, you may well want to click here to check an interactive graph of its earnings per share history.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.