Is Storytel AB (publ) (STO:STORY B) A Financially Sound Company?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

While small-cap stocks, such as Storytel AB (publ) (STO:STORY B) with its market cap of kr5.9b, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Since STORY B is loss-making right now, it’s essential to evaluate the current state of its operations and pathway to profitability. Let's work through some financial health checks you may wish to consider if you're interested in this stock. However, this is not a comprehensive overview, so I suggest you dig deeper yourself into STORY B here.

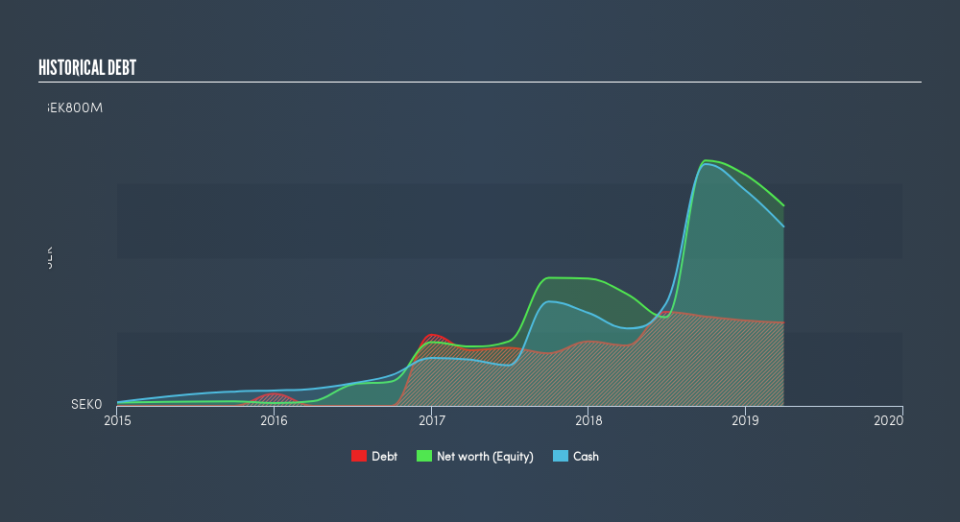

STORY B’s Debt (And Cash Flows)

STORY B has built up its total debt levels in the last twelve months, from kr163m to kr225m , which includes long-term debt. With this rise in debt, STORY B's cash and short-term investments stands at kr484m , ready to be used for running the business. We note it produced negative cash flow over the last twelve months. For this article’s sake, I won’t be looking at this today, but you can examine some of STORY B’s operating efficiency ratios such as ROA here.

Does STORY B’s liquid assets cover its short-term commitments?

At the current liabilities level of kr473m, the company has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 1.95x. The current ratio is calculated by dividing current assets by current liabilities. Usually, for Media companies, this is a suitable ratio since there's a sufficient cash cushion without leaving too much capital idle or in low-earning investments.

Is STORY B’s debt level acceptable?

With debt reaching 42% of equity, STORY B may be thought of as relatively highly levered. This is somewhat unusual for small-caps companies, since lenders are often hesitant to provide attractive interest rates to less-established businesses. Though, since STORY B is currently unprofitable, there’s a question of sustainability of its current operations. Running high debt, while not yet making money, can be risky in unexpected downturns as liquidity may dry up, making it hard to operate.

Next Steps:

STORY B’s high cash coverage means that, although its debt levels are high, the company is able to utilise its borrowings efficiently in order to generate cash flow. This may mean this is an optimal capital structure for the business, given that it is also meeting its short-term commitment. Keep in mind I haven't considered other factors such as how STORY B has been performing in the past. You should continue to research Storytel to get a more holistic view of the small-cap by looking at:

Future Outlook: What are well-informed industry analysts predicting for STORY B’s future growth? Take a look at our free research report of analyst consensus for STORY B’s outlook.

Historical Performance: What has STORY B's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.