Is Stradim Espace Finances (EPA:ALSAS) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Stradim Espace Finances SA (EPA:ALSAS) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Stradim Espace Finances

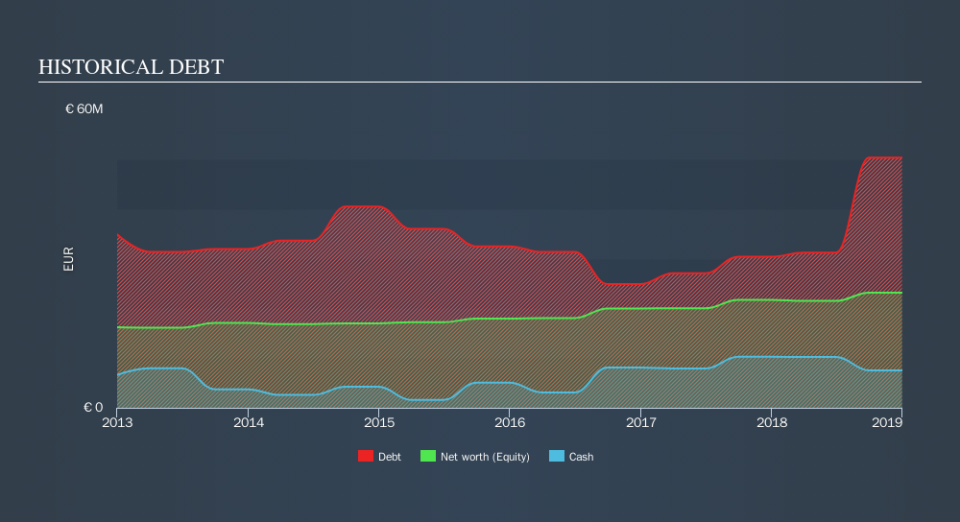

What Is Stradim Espace Finances's Net Debt?

As you can see below, at the end of December 2018, Stradim Espace Finances had €50.3m of debt, up from €31.2m a year ago. Click the image for more detail. However, because it has a cash reserve of €7.53m, its net debt is less, at about €42.8m.

A Look At Stradim Espace Finances's Liabilities

Zooming in on the latest balance sheet data, we can see that Stradim Espace Finances had liabilities of €110.4m due within 12 months and liabilities of €51.5m due beyond that. Offsetting these obligations, it had cash of €7.53m as well as receivables valued at €63.8m due within 12 months. So its liabilities total €90.5m more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the €26.3m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet." So we'd watch its balance sheet closely, without a doubt After all, Stradim Espace Finances would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Strangely Stradim Espace Finances has a sky high EBITDA ratio of 15.9, implying high debt, but a strong interest coverage of 18.6. This means that unless the company has access to very cheap debt, that interest expense will likely grow in the future. If Stradim Espace Finances can keep growing EBIT at last year's rate of 19% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But it is Stradim Espace Finances's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Stradim Espace Finances actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

We feel some trepidation about Stradim Espace Finances's difficulty level of total liabilities, but we've got positives to focus on, too. For example, its interest cover and conversion of EBIT to free cash flow give us some confidence in its ability to manage its debt. Looking at all the angles mentioned above, it does seem to us that Stradim Espace Finances is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. Over time, share prices tend to follow earnings per share, so if you're interested in Stradim Espace Finances, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.