AT&T Has Become a New Kind of Media Giant

AT&T was not actually acquired by a company called Game of Thrones Corp. earlier this year, though consumers could be forgiven for wondering. AT&T cell phone stores across the land seemed to have been taken over by a vaguely medieval industrial behemoth that had filled them with the heraldry of House Lannister, House Stark, and other Westerosi factions, plus costumes, weapons, and GOT-emblazoned smartphone cases, wireless chargers, and water bottles. Viewers of March Madness on AT&T-owned TBS saw slightly weird GOT-themed promos for the college basketball tournament and GOT-themed tweets (“Send a raven—they’re on to the #Elite8. #MarchMadness”). Another sign of GOT’s ascendance: The Iron Throne itself—or rather, a seven-foot-high, 310-pound replica of it—sits prominently in the lobby of AT&T headquarters in Dallas.

AT&T chief Randall Stephenson walks past that throne every day, but he doesn’t think much about the Lord of the Seven Kingdoms. In his world, Game of Thrones symbolizes something else: the first faint glimmers of how his costly vision for AT&T will work. Using company properties to publicize the show’s final-season premiere on AT&T-owned HBO is a minor example of the synergies he foresees; AT&T wireless customers with top-tier plans can also get HBO for free, for example. That’s a result of another titanic battle, the end in February of AT&T’s fight with the U.S. Department of Justice to win legal clearance to fully integrate operations with the Time Warner A-list media properties AT&T had agreed to buy more than two years earlier: most prominently, HBO, Warner Bros., CNN, TBS, and TNT.

Stephenson’s strategy is breathtaking in scale and scope, the largest transformation underway at any company in the Fortune 500. AT&T’s main traditional competitor, Verizon, has chosen an entirely different path, and Stephenson’s new rivals are in markedly different businesses. Back when AT&T was Ma Bell, after all, it was proudly staid, reliable, and boring. Stephenson marvels, “I spend as much time thinking about Amazon and Netflix as I do thinking about Verizon and Comcast now.”

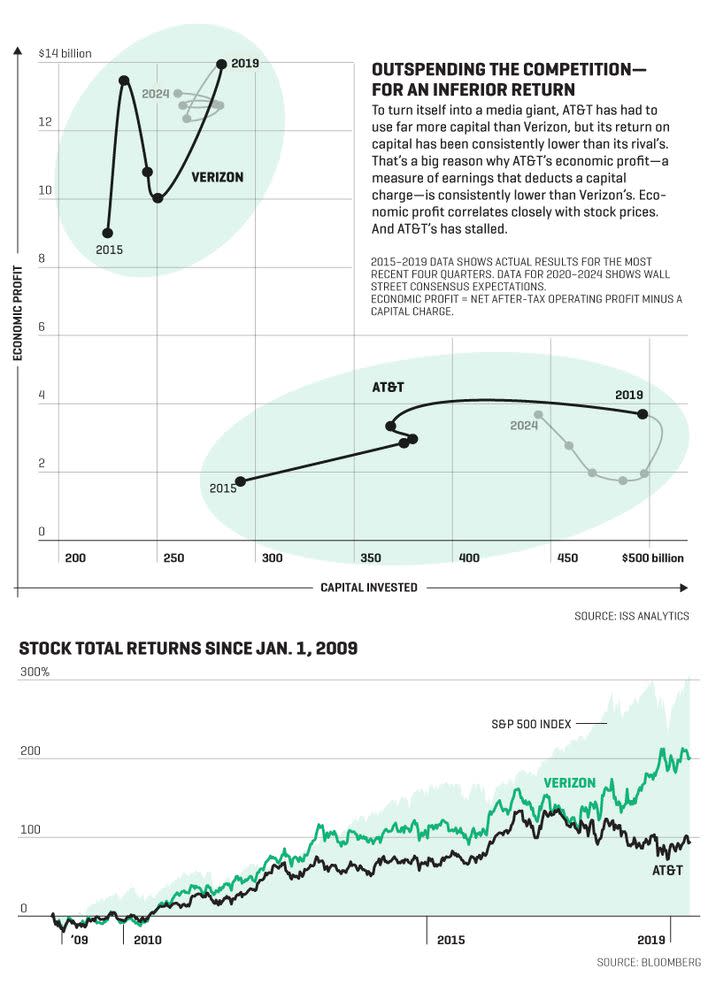

Stephenson also must think about the phone business, though, because it remains his biggest business by far—and it’s not growing, putting AT&T’s stock price and its financial future under pressure. That explains the company’s buying spree—and its massive debt load. Buying DirecTV in 2015 for $67 billion and Time Warner in 2018 for $104 billion has made AT&T the most heavily indebted nonfinancial company in America. Including lease obligations, which the accountants say must now be counted as debt, the company owes over $200 billion. That’s about the size of the external debt of Taiwan. Such massive debt merely matches Stephenson’s audacity. “AT&T’s ambition in acquiring Time Warner goes far beyond transforming a storied American company,” says Craig Moffett, a longtime telecom analyst and an AT&T critic. “Its goal is nothing less than a complete reinvention of the media ecosystem.”

Whatever the outcome of the strategy, Stephenson owns it. He has been CEO since 2007, and now, at age 59, he has time to see it through. How his gigantic bet turns out will define his career and determine the future of one of America’s most distinguished corporate names and largest companies, No. 9 on the Fortune 500. Right now, AT&T’s stalled stock price suggests that investors are far from convinced.

The grand vision begins with combining all the major elements of the media and telecom businesses, which no company has ever done before. Time Warner’s film and TV studios make some of the most successful and honored entertainment anywhere. Its cable networks—including TBS, TNT, CNN, Cartoon Network, and Turner Classic Movies—are distribution powerhouses. DirecTV carries those networks and others into homes through its satellite system. Add in AT&T’s wireless and landline customers, and Stephenson boasts that AT&T has “170 million distribution points we can push this through.”

With such a combination of media assets, the theory goes, AT&T can achieve unprecedented advantages. It can differentiate its fast-commoditizing wireless network by offering customers deals on its proprietary content. It can expose its content to vast audiences through all its networks. Because it collects staggering volumes of customer data through its wired, wireless, and satellite networks, it can enable advertisers to target their messages with new precision and, in some cases, even track customers who have seen specific ads and thus gauge how the ads performed—services for which advertisers will gladly pay a big premium.

The immediate next step in the transformation, likely the biggest and most visible step, will be to introduce a video-on-demand Internet streaming service—a Netflix competitor—in this year’s fourth quarter. AT&T says the new service eventually will include original content, HBO, movies from multiple studios, and library content from HBO and Warner Bros.

Making that all happen is the job of John Stankey, a 34-year phone company man who’s now in charge of the former Time Warner, rechristened WarnerMedia. At the heart of the grand plan, he says, is something the old phone company wouldn’t have known much about: emotion. Cell phones have become so indispensable that people are emotionally attached to them, and “our ability to now place content with that connectivity is another way to keep it emotionally relevant,” says Stankey, sitting in a sunlit conference room on the executive floor of the Time Warner Center in Manhattan.

Stankey is acutely aware that he’s jumping into a market suddenly swarming with competitors who know a lot about connecting emotionally with consumers. Disney will launch its Disney+ streaming service on Nov. 12, and investors were so wowed by an April 11 announcement that they bid the stock up 12% the next day. Apple, with its 1.4 billion devices worldwide, will debut a streaming service this fall. And Comcast, with 31 million cable and broadband customers plus ownership of NBC and Universal Studios, plans to enter the streaming fray next year. Netflix and Amazon, girding for the onslaught, are well fortified with tens of millions of streaming customers each and prodigious data on all of them.

How many subscription streaming services can survive? “I think it’s someplace between 10 and two, and it’s probably on the lower side of that scale,” Stankey says. “A good outcome for a company like ours is that there are four or five. I think we’ve got a position where we can be one of those.”

Whether that expectation is realistic remains to be seen. “We know that Netflix has the highest satisfaction score of any U.S. TV [streaming] service, with Amazon and [Disney-controlled] Hulu close behind, placing all three in relatively secure positions,” notes Toby Holleran of Ampere Analysis. “This makes Disney+ most likely to displace the niche streaming services.”

But in AT&T’s synergistic vision, subscription revenue is just one of the ways the company plans to profit from its expensively acquired content. An important benefit, seemingly mundane, is reducing churn in wireless subscribers. Even a little churn—AT&T’s was 1.67% last year—is a big problem when you’ve got 153 million subscribers, says John Donovan, who runs AT&T’s wireless, DirecTV, wired broadband, and business services units—79% of the company’s $171 billion in 2018 revenue (which included Time Warner as of June 15, 2018). “Ten basis points of churn is a billion dollars,” he says, and company research shows that giving customers the right exclusive content on their phones can slow churn significantly. A customer might say, “ ‘This thing’s awesome. My spouse took me out shopping, and I sat and watched football.’ It only takes one impactful video viewing per month for someone to say, ‘I am never giving up AT&T on this phone,’” Donovan says. And when that happens, “you have 30 basis points less churn—3 billion bucks. It’s real money.”

Adding strength to the whole proposition is AT&T’s unique aggregate customer data trove and its value in addressable advertising over DirecTV and AT&T’s direct-to-consumer streaming services; ads can also be directed less precisely through the former Turner networks. “Say you and your neighbor are both DirecTV customers and you’re watching the same live program at the same time,” says Brian Lesser, who oversees the vast data-crunching operation that supports this kind of advertising at AT&T. “We can now dynamically change the advertising. Maybe your neighbor’s in the market for a vacation, so they get a vacation ad. You’re in the market for a car, you get a car ad. If you’re watching on your phone, and you’re not at home, we can customize that and maybe you get an ad specific to a car retailer in that location.”

Such targeting has caused privacy headaches for Yahoo, Google, and Facebook, of course. That’s why AT&T requires that customers give permission for use of their data; like those other companies, it anonymizes that data and groups it into audiences—for example, consumers likely to be shopping for a pickup truck—rather than targeting specific individuals. Regardless of how you see a directed car ad, say, AT&T can then use geolocation data from your phone to see if you went to a dealership and possibly use data from the automaker to see if you signed up for a test-drive—and then tell the automaker, “Here’s the specific ROI on that advertising,” says Lesser. AT&T claims marketers are paying four times the usual rate for that kind

of advertising.

Combine all the elements that Stephenson has assembled, and “AT&T can no longer be called a telecom company,” says Moffett. Stephenson doesn’t object to the characterization. He now calls AT&T “a modern media company.”

For most of his career, Stephenson never imagined he’d be doing anything like any of this. He was born in Oklahoma City and started working for Southwestern Bell Telephone in 1982, when he was still in college. After getting a master’s degree in accounting at the University of Oklahoma in 1986, he became a fast-rising star in finance jobs at Southwestern Bell, at one point being posted to Mexico City to oversee the company’s stake in Telmex, where he worked closely with another big investor, eventual billionaire Carlos Slim. In 2005, Southwestern Bell (renamed SBC) bought AT&T, the remnant left after the 1984 breakup. The combined companies took the AT&T name, one of the best known and most valuable in America. Two years later, at age 47, Stephenson became CEO.

Today he occupies an understated fourth-floor office in AT&T’s high-rise in the heart of old downtown Dallas, kitty-corner from the 1912 Adolphus Hotel and a block down from the original Neiman Marcus store. Until recently, he recalls, remaking the media industry in the way he’s now attempting to do was supposed to be technologically impossible. “I remember in the early 2000s asking, ‘Do you ever think voice will just move off those landlines and onto mobile predominantly?’ and a lot of people said, ‘No way. There just isn’t enough capacity, not enough spectrum.’ And lo and behold, look what happened.” When he later asked about accessing the Internet through the cell network, “it was the exact same reply: ‘No way! It can never happen.’ And along came the iPhone. Then we asked, ‘What is now becoming the most desired application on these devices?’ Video. ‘And could you ever accommodate video?’ ‘No, there’s no way.’ ”

He was learning a lesson: When the engineers tell you it’s impossible, don’t believe them. “Full video transportability we just believed was going to be important,” he recalls. Crucially, he also decided he wanted to do more than just offer a wireless network that could handle video; he wanted to offer video itself. But there was a problem: “We couldn’t get the rights to do any of it.” The solution: “DirecTV was available,” and like cable companies, it had rights to carry a lot of video programming. So AT&T bought DirecTV in 2015, and “within months we were able to take that full portfolio of content that DirecTV had the rights to, and we were porting it to the mobile device.”

Buying rights merely whetted Stephenson’s appetite. Thinking about the future, his team concluded that if the coming 4G and 5G networks would be mainly vehicles for delivering video, then “controlling your destiny to some degree would be really important—that is, owning premium content,” he says. “And that’s what took us down this path of desiring to own a big portfolio of premium content.” It was a $104 billion decision.

The future was particularly appealing to Stephenson because the past, AT&T’s phone business, had been looking so bleak. Lost in the drama over the Time Warner acquisition is AT&T’s financial reality: Though it generates tons of cash, its overall business is in decline. Operating revenues in wireless and landline phones and broadband plus DirecTV, accounting for 71% of the total, were all lower last year than they were two years earlier, despite a robust economy. What’s worse, the declines are accelerating unexpectedly. Wall Street has been lowering its consensus forecast of AT&T’s 2019 Ebitda, a measure of operating cash flow that subtracts debt-service and other expenses, for years. The latest forecast, including a full year of WarnerMedia results, is less than the consensus forecast from mid-2016, before a possible Time Warner deal had ever been mentioned.

Even while shrinking, the company’s core businesses produced some $44 billion of cash last year after all the bills had been paid—that is, AT&T had almost a billion dollars coming in the door each week. Last year it spent about $21 billion of it on capital investments, mainly building and maintaining its nationwide wireless network, upgrading it to 5G, and installing fiber for home and business customers in much of the country. It sent another $13 billion to shareholders as dividends; at the recent stock price of about $30, the dividend yield is 6.7%, one of the most generous dividends paid by any major company in America. (High yields are the result of big payouts and low stock prices, a reflection of a lack of investor confidence.)

In fact, AT&T’s stock price was recently no higher than where it was eight years ago. Concern about the debt is a big part of the reason. The day after AT&T closed on its purchase of Time Warner last June, Moody’s downgraded AT&T’s debt rating to two notches above junk. The rating agency’s rationale was enough to chill any AT&T stockholder’s blood: “Moody’s continues to believe AT&T will need to reduce its cash dividends in order to remain competitive with its new peer group that includes other media and technology giants, many of which have very lean balance sheets.” (AT&T expects to pay down debt with excess cash and is looking to sell assets worth up to $8 billion for the same reason.)

Prior to buying Time Warner, the danger for AT&T was that its revenue declines would accelerate in the age of wireless video. All the previous uses of the cell network—talking, texting, accessing the Internet—are active uses in which customers create their own experiences. Video is different. It’s passive; someone else creates the experience, and if it’s good enough, customers will pay for it beyond what they’re already paying for connectivity. Stephenson and his team feared that the value in the business of wireless connectivity could migrate from the owner of the network to the owner of the content. That’s why he framed the purchase of Time Warner as necessary for AT&T to control its destiny.

Investors aren’t buying it. Their unwillingness to price the stock higher than it was in 2011 reflects weak confidence in the company’s growth. In fact, the stock was much higher in the summer of 2016, hitting $43 not long before the deal for Time Warner was announced that October. Most Wall Street analysts now rate the stock a “hold” at around $30.

Skeptics contend that AT&T’s strategy is not a well-conceived long-term plan so much as a response to near-term problems. “They’re buying sales growth, not generating sales growth organically,” notes Bennett Stewart, a senior adviser to the shareholder advisory firm ISS. It had long seemed unlikely that antitrust authorities would let AT&T buy another phone company, so it has been forced to look elsewhere for acquisitions. “The DirecTV deal was never driven by an analysis of what AT&T needed in order to succeed, but rather by what the company would be allowed to buy,” argues Craig Moffett, the Wall Street analyst. “That’s a terrible way to approach strategy.”

Moffett even questions the need for AT&T to own content at all. “Did that mean that they planned to make Time Warner content exclusive to AT&T distribution? No. They promised not to” during the antitrust trial. He questions the whole concept of synergies from combining Warner content with AT&T distribution, such as offering HBO free to wireless customers with top-tier plans. “AT&T’s strategy for delivering an integrated offering to consumers has heretofore amounted to simple discounting, and to devastating effect,” he says. Moffett also doubts AT&T can achieve the $1.5 billion in annual cost savings it has promised investors. John Stephens, AT&T’s chief financial officer, says those cost-saving plans “remain on target.”

Another skeptic believes AT&T wasn’t rigorous enough in thinking it all through. Making a vertical acquisition in order to control your destiny isn’t necessarily a bad idea, says Roger Martin, a longtime strategy consultant who has advised Verizon in the past. “If you can buy into a part of the industry upstream or downstream and you can have competitive advantage there, it’s kind of a no-brainer,” he says. The key is whether you can acquire a company that holds true competitive advantage—“because if you can’t, it’ll just be the anchor around your neck.”

It’s clear to Martin that WarnerMedia cannot hold a competitive advantage in content creation. “Others are dropping unprecedented levels of spending into the business,” he says. Analysts estimate Disney will spend $21 billion on content this year, Netflix $15 billion, and AT&T $14 billion. (None of the companies will comment on those estimates.) “If you’re AT&T, where do you stand?” Martin asks. “You’re spending less on content than Netflix and Disney, and you won’t beat Verizon on 5G. Where does that leave you?” The answer, he believes, is the dreaded locale identified by strategy authority Michael Porter as the worst place for any company to be strategically: caught in the middle.

Even Warren Buffett quails at the prospect of competing in such a powerful field of rivals. “Everybody has just got two eyeballs, and they’ve got x hours of discretionary time … maybe four or five hours a day,” he said recently at a charity event, speaking generally about the entertainment industry. “You’ve got some very, very, very big players that are going to fight over those eyeballs. The eyeballs aren’t going to double. You have very smart people with lots of resources trying to figure out how to grab another half-hour of your time.” His assessment: “I would not want to play in that game myself. That’s too tough for me.”

Any business that Buffett wants to avoid sounds unpromising, but Stephenson rejects the legendary investor’s premise. Acknowledging that “there are only 16 waking hours in the day,” he says, “Well, we haven’t filled up the 16 hours yet.” He nods toward his office window over Commerce Street with its busy traffic, which he says will ease when 5G networks enable autonomous cars. “When you have the lion’s share of those cars autonomous, for the average person that’s another two hours of availability of screen time, consuming video.”

The larger reality, the fact that makes one’s head spin trying to grasp AT&T’s future, is the long-heralded arrival of what for years the telecom industry called “convergence.” Virtually all data—a text, your location history, a CT scan, Casablanca—is digital and available almost instantly to almost anyone, anywhere, anytime. Any company can start a streaming service, and any consumer can watch it. It’s an endlessly, constantly fluid environment to a degree that has never existed before.

That reality may comfort Stephenson as he faces the many skeptics. Their logic is moored to old assumptions about a world that no longer exists, one could argue. He may find further comfort in knowing he can combine WarnerMedia’s killer content with something no other media company has or is likely to have, a nationwide wireless network that will be 5G in a few years. But three other wireless networks (two, if Sprint and T-Mobile merge) are available for rent, and in a fluid, digital world, who knows what Buffett’s “very smart people with lots of resources” might do?

The uncertainties, the challenges, and the competition all seem daunting. But it’s possible, maybe necessary, to take a different attitude. “It’s not daunting—it’s exciting,” says Donovan, Stephenson’s lieutenant who runs AT&T’s nonmedia operations. “These are the best of times. The greatest gift that Randall has given to this corporation is the inspiration of knowing that people believe that it’s difficult, believe that we may be wrong. It’s so amazing to wake up and say, ‘We have all these tools and weapons, and the world thinks we might be wrong.’ That is motivation.”

It’s a cheerful, hopeful perspective. But Donovan and his boss know AT&T isn’t the only content-plus-distribution army with powerful weapons. Come to think of it, it calls to mind the twisted, bloody plotlines in a certain medieval fantasy series. Except for AT&T, the stakes are quite real.

A version of this article appears in the June 2019 issue of Fortune with the headline “AT&T’s Heavy Lift.”

More must-read stories from Fortune:

—The 2019 Fortune 500 list demonstrates the prize of size

—Fortune 500 CEO Survey: The results are in

—What the Fortune 500 would look like as a microbiome

—The Occidental-Anadarko merger reveals the crude truth about oil prices

—Why the giants among this year’s Fortune 500 should intimidate you

Catch up with Data Sheet, Fortune‘s daily digest on the business of tech.