T-Bills Show Wariness About Default Even as Debt Ceiling Talks Progress

- Oops!Something went wrong.Please try again later.

(Bloomberg) -- Treasury bill markets are a long way from sounding the all-clear about the risk of a US default despite the emergence of a more positive tone in negotiations over the statutory debt ceiling between the White House and Congressional leadership.

Most Read from Bloomberg

World’s Biggest Nuclear Plant May Stay Closed Due to Papers Left on Car Roof

Stocks Slide as Sentiment on Global Outlook Sours: Markets Wrap

Securities due in early June — seen as most at risk of non-payment if the US government exhausts its borrowing capacity in the time period Treasury Secretary Janet Yellen has warned about — continue to include a significant yield premium as investors steer clear. Rates on some of those maturing in the early part of the month topped 6% on Tuesday, which is not only above those for later in the summer, but close to 4 percentage points above instruments maturing May 30. Earlier, the Treasury sold its newest 21-day cash management bill at 6.2%.

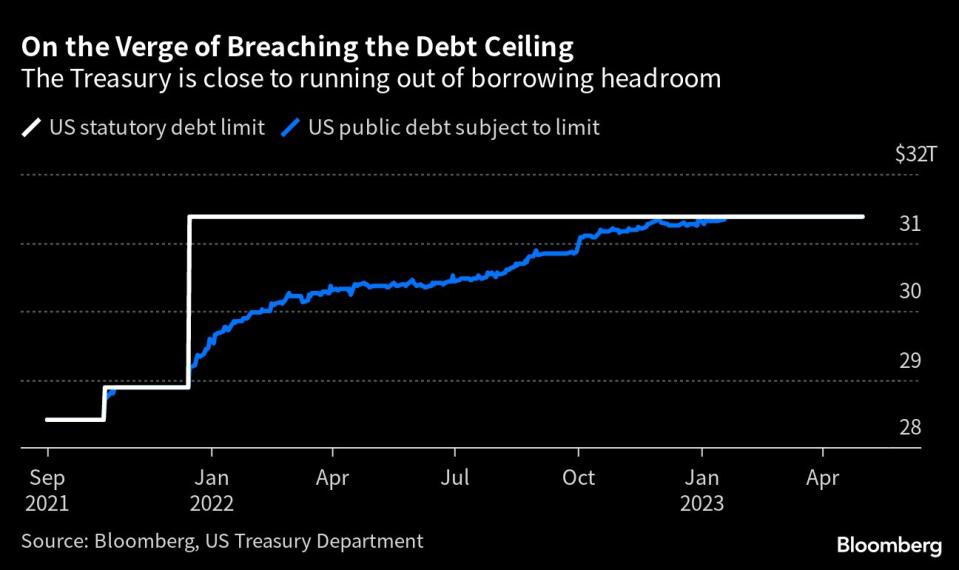

The Treasury Secretary said in a new letter on Monday that it’s now “highly likely” that her department will run out of cash in early June without an extension of the debt ceiling, and repeated her warning that the moment could come as soon as June 1. The Bipartisan Policy Center, meanwhile, said in its latest analysis that there’s an “elevated risk” that the crunch point for the US Treasury will fall between June 2 and 13. That’s in line with Wall Street strategists expectations as to the point when Treasury’s cash pile will be at its lowest ebb.

Debt-limit negotiators are meeting again in Washington Tuesday following a Monday sitdown between President Joe Biden and House Speaker Kevin McCarthy that the Republican described as “productive.” There is, as yet, no deal, but both sides reiterated that “default is off the table,” according to Biden. McCarthy said Tuesday that a deal is possible before June 1.

Still ”even as talks progress, political landmines lay ahead,” Stifel strategist Brian Gardner said in a note to clients. But “even if negotiations stall, the chances of a default on U.S. Treasuries are remote,” he wrote.

From Washington to Wall Street, here’s what to watch to gauge how worried observers should be and when they should be concerned.

The Bills Curve

Investors have historically demanded higher yields on securities that are due to be repaid shortly after the US is seen as running out of borrowing capacity. That puts a lot of focus on the yield curve for bills — the shortest-dated Treasuries. Noticeable upward distortions in particular parts of the curve tend to suggest increased concern among investors that that’s the time the US might be at risk of default. Right now that’s most prominent around early June. At one point, yields on Treasury bills slated to mature June 6 topped 6%, and the debt-ceiling concerns even drove the auction yield on the department’s newest 21-day cash management bill to a remarkable 6.2%. That’s higher even than the four-week bill sale earlier this month that went off at 5.84%, the most elevated yield for any benchmark sale in over two decades.

But it’s not just early June securities that investors are circumspect about. Even if the Treasury can make it past the June danger zone, there are still risks of a default during the US summer if no legislative fix is found.

X-Date Predictions

Underpinning the various moves in debt markets are differing estimates about when the government might exhaust its options to fund itself — commonly referred to as the X-date. While the administration has provided guidance that it might fall short as soon as June, prognosticators across Wall Street have also been running the numbers based on government cash flows and expectations around taxes and spending. Most strategists have pulled forward their baseline estimates to align more with forecasts out of Washington, although some remain hopeful that the Treasury might be able to stretch its resources until late summer.

The Cash Balance

The US government’s ability to pay its debts and meet its spending obligations ultimately comes down to whether it has enough cash. So the amount sitting in its checking account is crucial. That figure fluctuates daily depending on spending, tax receipts, debt repayments and the proceeds of new borrowing. If it gets too close to zero for the Treasury’s comfort that could be a problem. The amount of money the US government has to pay its bills rose on Friday and Monday, providing a modicum of respite as it seeks to eke out funding until a solution can be found to the ongoing debt-limit impasse, but the broad trend has been for the total to dwindle. Focus will also be on the so-called extraordinary measures that the Treasury is using to eke out its borrowing capacity. The government has already used up more than two thirds of these accounting gimmicks and had $92 billion up its sleeve as of the middle of last week.

Insuring Against Default

Beyond T-bills, one other key area to watch for insight on debt-ceiling risks is what happens in credit-default swaps for the US government. Those instruments act as insurance for investors in cases of non-payment. The cost to insure US debt is now higher than the bonds of — among others — Greece, Mexico and Brazil, which have defaulted multiple times and have credit ratings many rungs below that of the US.

(Updates pricing, adds details on auction and cash balance.)

Most Read from Bloomberg Businessweek

The Man Who Spends $2 Million a Year to Look 18 Is Swapping Blood With His Father and Son

Maasai Are Getting Pushed Off Their Land So Dubai Royalty Can Shoot Lions

©2023 Bloomberg L.P.