The Fed now faces same destination — with a more treacherous path

A version of this post was originally published on TKer.co

For a moment, sentiment toward the economy began to shift bullishly on the heels of economic reports that were stronger than many economists’ expectations.

But all of that came to an end last week as concerns over financial stability emerged in the wake of two bank failures, which in turn put a spotlight on the vulnerabilities of smaller regional banks.

“Our banks analysts see a meaningful increase in funding costs ahead, which will lead to tighter lending standards, slower loan growth, and wider loan spreads,“ Ellen Zentner, chief U.S. economist at Morgan Stanley, wrote on Thursday. “We were already expecting a meaningful slowdown in growth and job gains over the coming months, and the prospect of substantial tightening in credit conditions raises the risk that a soft landing turns into a harder one.“

Economists at Goldman Sachs, JPMorgan, and Wells Fargo were also among those citing similar economic headwinds as they cut their forecasts for growth.

On one hand, these recent developments aren’t good. Jobs will almost certainly be lost as a tighter banking system means financing becomes less accessible.

On the other hand, these effects are arguably of the kind that the Federal Reserve has been aiming for over the past year.

An unplanned path to the same destination 🚧

Over the past year, the Fed has been aggressively tightening monetary policy in its effort to bring down inflation by cooling economic demand. The thinking behind this was that by tightening financial conditions with interest rate hikes, financing costs go up for businesses and consumers, which slows their spending. This eases pressure on supply and, in turn, prices cool.

For more on why the Fed is tightening monetary policy, read: The complicated mess of the markets and economy, explained 🧩

The Fed likely didn’t specifically intend for a big bank to fail, but the risk of such a thing happening was going to be elevated with how monetary policy was being implemented.

So it’s a bit ironic these undesired bank failures seem to be having the desired effect of accelerating the conditions that could ultimately lead to inflation coming down decisively.

“Ongoing pressure could cause smaller banks to become more conservative about lending in order to preserve liquidity in case they need to meet depositor withdrawals, and a tightening in lending standards could weigh on aggregate demand,” Jan Hatzius, chief economist at Goldman Sachs, wrote in a research note on Wednesday.

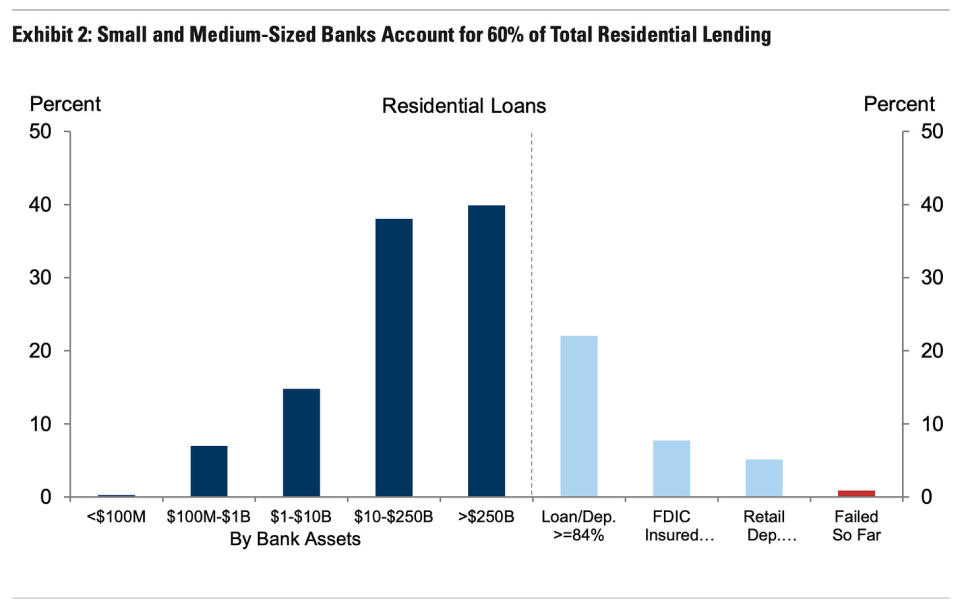

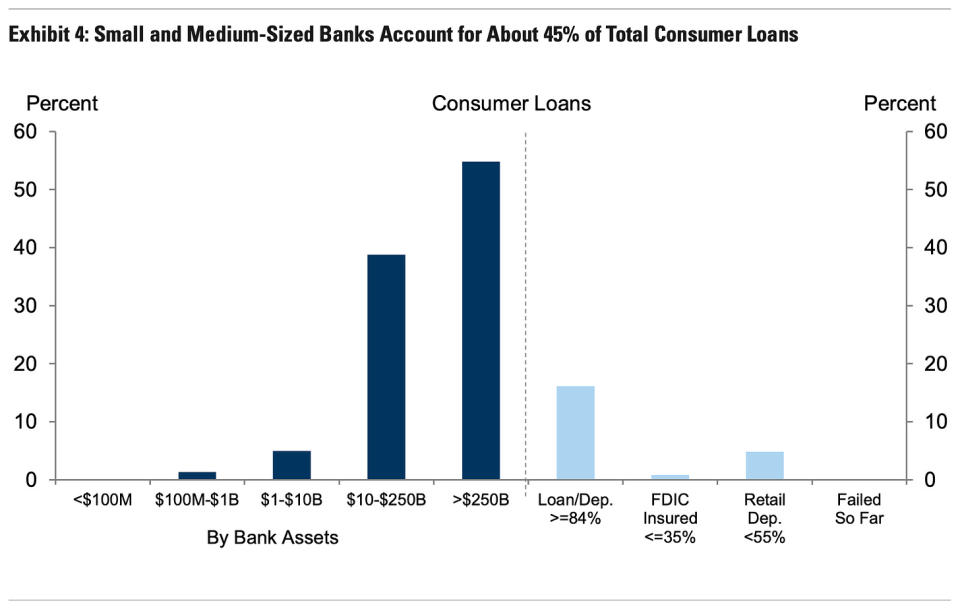

And just because these banks are smaller doesn’t mean they’re small.

“Small and medium-sized banks play an important role in the US economy,” Hatzius added. “Banks with less than $250bn in assets account for roughly 50% of US commercial and industrial lending…”

“…60% of residential real estate lending…”

“…80% of commercial real estate lending…”

“…and 45% of consumer lending.”

As Bloomberg Opinion columnist Conor Sen put it:

Just hypothetically, if it were possible for a large-ish bank to fail and for lending standards/financial conditions to tighten enough to knock 50bps off NGDP growth but no broader contagion, I’d say that helps the Fed achieve its dual mandate.

In other words, the unintended bank failures may be helping the Fed achieve its intended goals. It’s an unplanned path to the same destination.

And not that anyone’s particularly sanguine about what’s happening, but some are less sanguine about this take than others.

“I always laugh when people say, ‘Oh, the Fed’s policies are finally gaining traction,’” Mohamed El-Erian, chief economic adviser at Allianz, told Bloomberg TV on Friday. “Is this the way we want the Fed’s policies to gain traction? By destabilizing the banking system? By creating a credit withdrawal? By having too much damage to the economy and to jobs? You know, that's not how monetary policy is supposed to gain traction, not through financial instability.”

“So yeah, to some extent it does mean that the Fed will end up with lower inflation than would have been otherwise,” El-Erian added. “But the journey there is terrible, and it's unnecessary.”

The risk is that the emerging financial instability causes much more economic damage than what would’ve been necessary to get inflation under control.

How to think about whatever comes next 🤔

It’ll be a month or so before we start getting economic data reflecting the impact of the banking turmoil that began two weeks ago.

With that in mind, approach this week’s review of the macro crosscurrents (below) with a little caution given that most of it reflects economic activity that occurred before last week’s developments.

Neil Dutta, head of economic research at Renaissance Macro, addressed how to interpret the recent economic data in an email on Thursday:

It is true that the latest economic data are stale, but I do not believe that we should ignore the news entirely. The US economy went into this financial market shock with substantial momentum. Core retail sales in February? Strong. Building permits and housing starts? Strong. Initial jobless claims? Low. Nominal growth in Q1 is running between 8 to 9% (Real GDP tracking close to 3.5% with underlying inflation of 5%). That's a pretty sizable buffer. Looking ahead, outside of nonresidential business fixed investment, it is hard to see what goes south. Government spending and inventories have room to add in the months ahead, as an example….

Indeed, while the risk the economy tips into recession has been elevated — something I’ve been noting in TKer’s past weekly review of macro crosscurrents — it continues to be bolstered by massive tailwinds. The question is to what degree these tailwinds subside.

-

Related from TKer:

Reviewing the macro crosscurrents 🔀

There were a few notable data points from last week to consider:

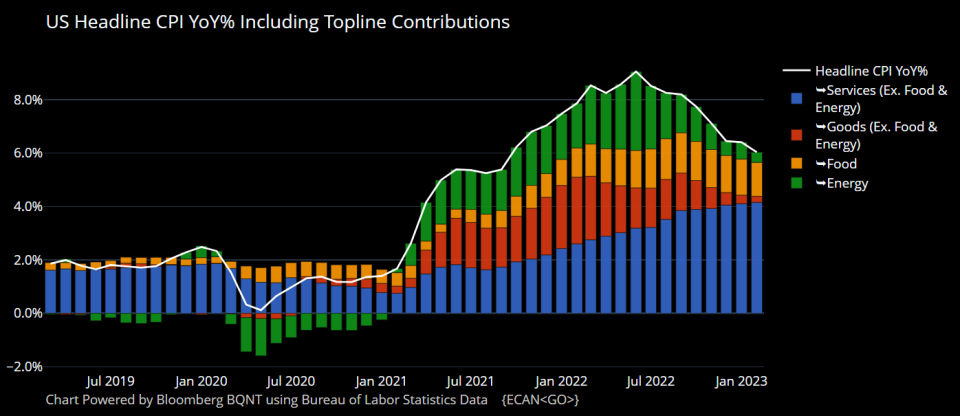

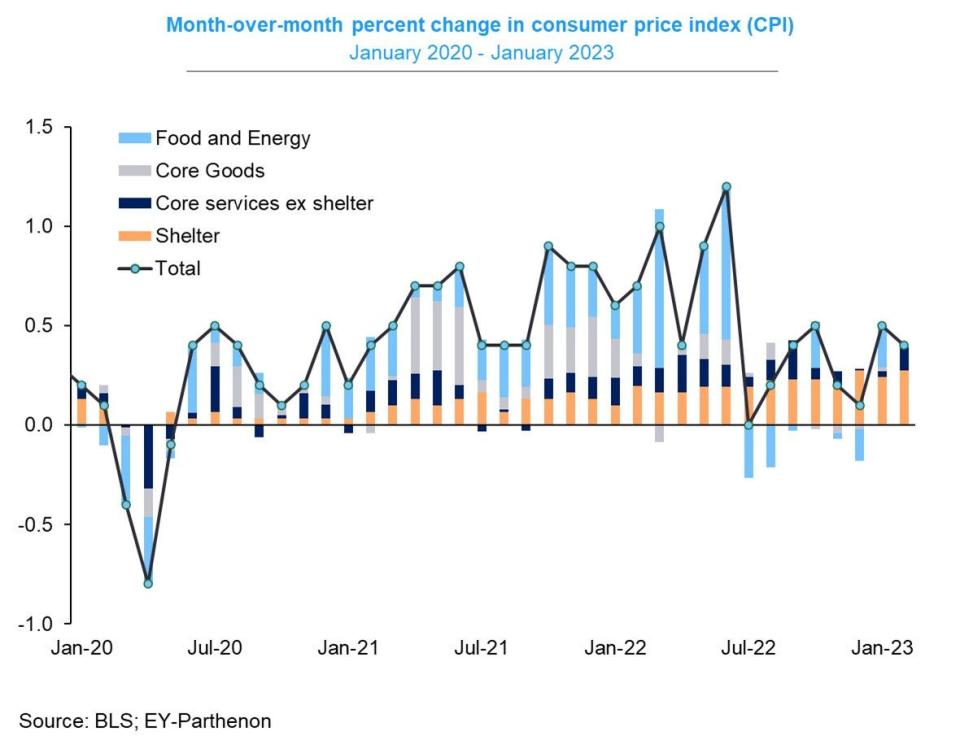

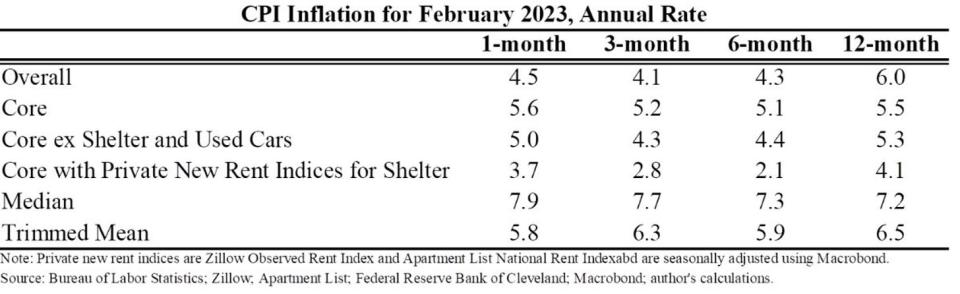

🎈 Inflation continues to moderate. The consumer price index (CPI) in February was up 6.0% from a year ago, down from 6.3% in January. Adjusted for food and energy prices, core CPI was up 5.5%, down marginally from the month prior.

On a month-over-month basis, CPI was up 0.4% as energy prices fell 0.6% during the period. Core CPI was up 0.5% as shelter prices jumped 0.8%.

If you annualize the three-month trend in the monthly figures, CPI is rising at a 4.1% rate and core CPI is climbing at a 5.2% rate.

The bottom line is that while inflation rates have been trending lower, they continue to be above the Federal Reserve’s target rate of 2%.

For more on the implications of cooling inflation, read: The bullish 'goldilocks' soft landing scenario that everyone wants 😀.

🏡 Rents are cooling. From Redfin: “The median U.S. asking rent rose 1.7% year over year to $1,937 in February — the smallest increase in nearly two years and the lowest level in a year… February was the ninth straight month in which rent growth slowed on a year-over-year basis. Rents fell 0.3% from a month earlier. Still, the median asking rent remained 21.4% higher than it was in February 2020, the month before the coronavirus was declared a pandemic.“

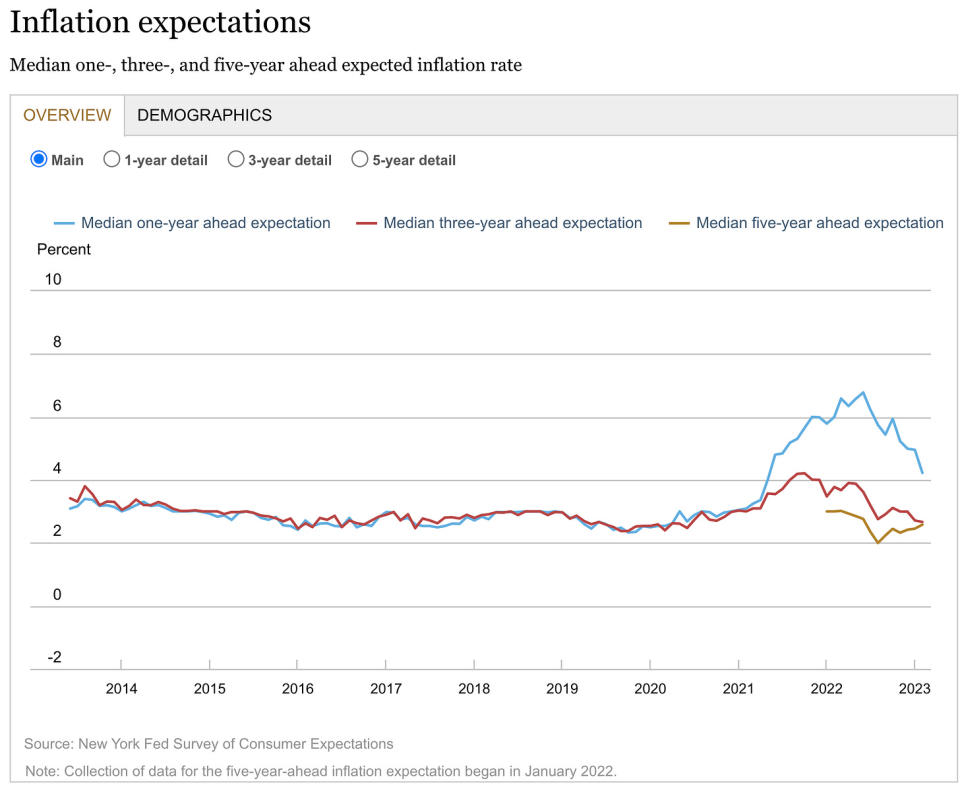

👍 Expectations for inflation ease. From the New York Fed’s February Survey of Consumer Expectations: “Median inflation expectations dropped by 0.8 percentage point at the one-year-ahead horizon to 4.2%, remained unchanged at the three-year-ahead horizon at 2.7%, and increased by 0.1 percentage point at the five-year-ahead horizon to 2.6%.“

This echoes the University of Michigan’s March Survey of Consumers: “Year-ahead inflation expectations receded from 4.1% in February to 3.8%, the lowest reading since April 2021, but remain well above the 2.3-3.0% range seen in the two years prior to the pandemic. Long-run inflation expectations edged down to 2.8%, falling below the narrow 2.9-3.1% range for only the second time in the last 20 months.“

🛍️ Retail sales cool. According to Census Bureau data, retail sales in February declined 0.4% to $697.9 billion.

Excluding autos and gas, sales were flat as gains in online retail, health and personal care, groceries, and electronics were more than offset by declines in department stores, furniture, restaurants and bars, and clothes.

🏭 Industrial activity cools. Industrial production activity in February was unchanged from January levels, with manufacturing output climbing 0.1%.

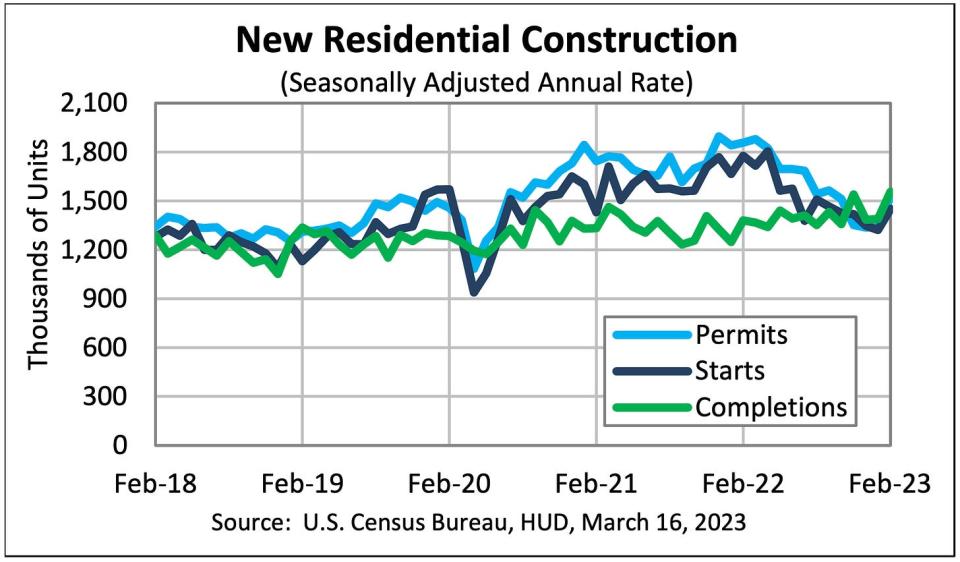

🏠 Housing construction jumps. According to the Census Bureau, new building jumped 13.8% month-over-month in February to an annualized rate of 1.52 million units. Housing starts surged 9.8% to 1.45 million units.

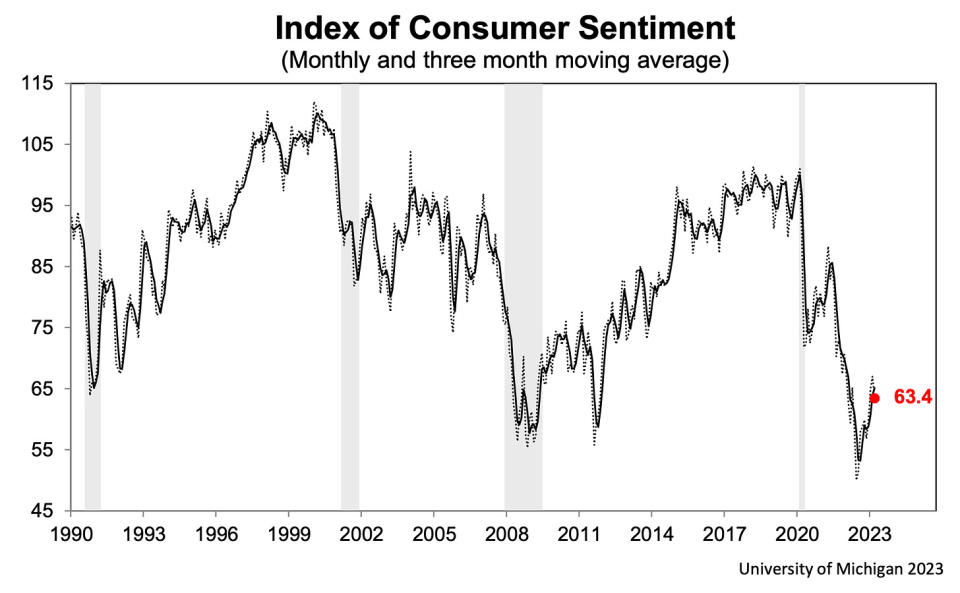

👎 Surveys sour. Regional manufacturing surveys from the New York Fed and Philly Fed suggested business activity contracted in March.

Consumer sentiment, meanwhile, deteriorated in March for the first time in four months.

For more on the signals sent by surveys, read: What businesses do > what businesses say 🙊.

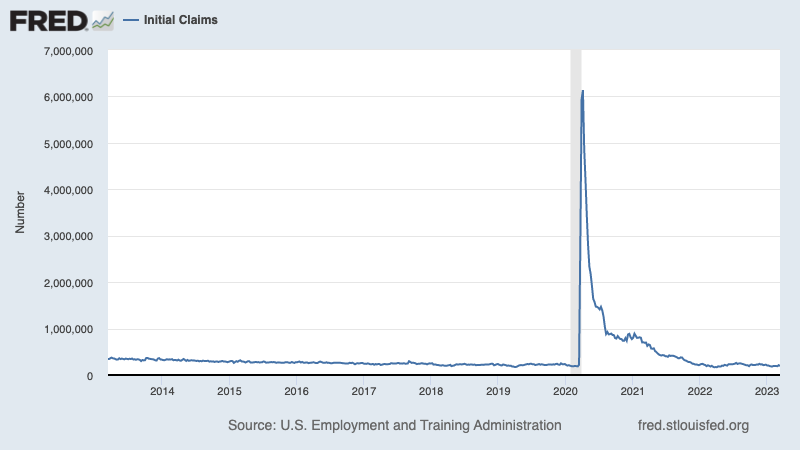

💼 Unemployment claims remain low. Initial claims for unemployment benefits — the most up-to-date of the major labor market stats — fell to 192,000 during the week ending March 11, down from from 212,000 the week prior. While the number is up from its six-decade low of 166,000 in March 2022, it remains near levels seen during periods of economic expansion.

For more on low unemployment, read: The labor market is simultaneously hot 🔥, cooling 🧊, and kinda problematic 😵💫.

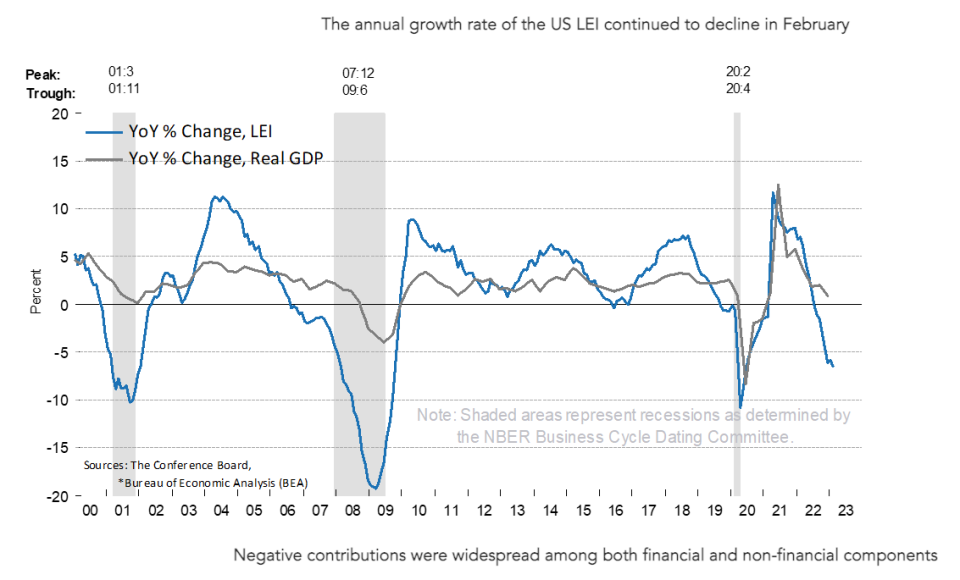

🚨Recession warning sign. The Conference Board’s Leading Economic Index¹ fell in February, the eleventh consecutive month of declines. From The Conference Board's Ataman Ozyildirim: "Negative or flat contributions from eight of the index’s ten components more than offset improving stock prices and a better-than-expected reading for residential building permits. While the rate of month-over-month declines in the LEI have moderated in recent months, the leading economic index still points to risk of recession in the US economy. The most recent financial turmoil in the US banking sector is not reflected in the LEI data but could have a negative impact on the outlook if it persists. Overall, The Conference Board forecasts rising interest rates paired with declining consumer spending will most likely push the US economy into recession in the near term."

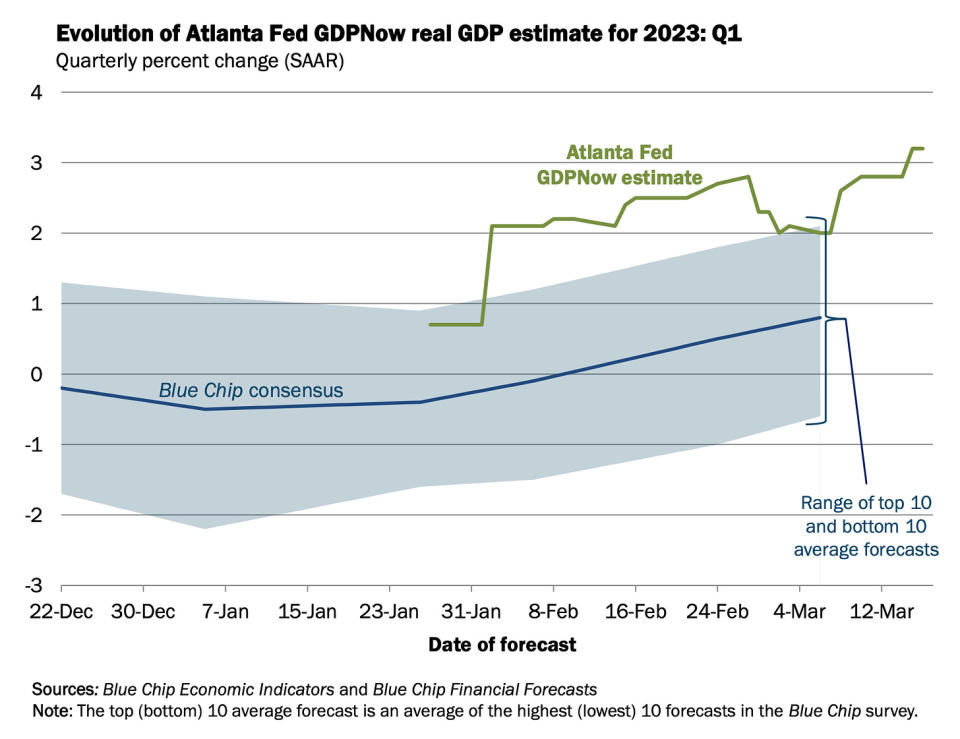

📈 But near-term GDP growth estimates remain rosy. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 3.2% rate in Q1. This is up considerably from its initial estimate of 0.7% growth as of January 27.

For more on the improving economic outlook, read: Economic forecasts are getting revised up, and people aren't thrilled about it 🙃

Putting it all together 🤔

Despite recent banking tumult, we’re getting a lot of evidence that we could see a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

The Federal Reserve recently adopted a less hawkish tone, acknowledging on February 1 that “for the first time that the disinflationary process has started.“ We will learn more about the Fed’s evolving thinking on March 22 after the next Federal Open Market Committee.

In any case, inflation still has to come down more before the Fed is comfortable with price levels. So we should expect the central bank to continue to tighten monetary policy, which means we should be prepared for tighter financial conditions (e.g. higher interest rates, tighter lending standards, and lower stock valuations).

All of this means the market beatings may continue, and the risk the economy sinks into a recession will be relatively elevated. In fact, recession risks intensified recently with bank failures sparking concerns about financial stability.

However, it’s important to remember that while recession risks are elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs. Those with jobs are getting raises. And many still have excess savings to tap into. Indeed, strong spending data confirms this financial resilience. So it’s too early to sound the alarm from a consumption perspective.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

As always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a pretty rough couple of years, the long-run outlook for stocks remains positive.

A version of this post was originally published on TKer.co

Sam Ro is the founder of TKer.co. Follow him on Twitter at @SamRo

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance