We Think Chongqing Machinery & Electric (HKG:2722) Has A Fair Chunk Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Chongqing Machinery & Electric Co., Ltd. (HKG:2722) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Chongqing Machinery & Electric

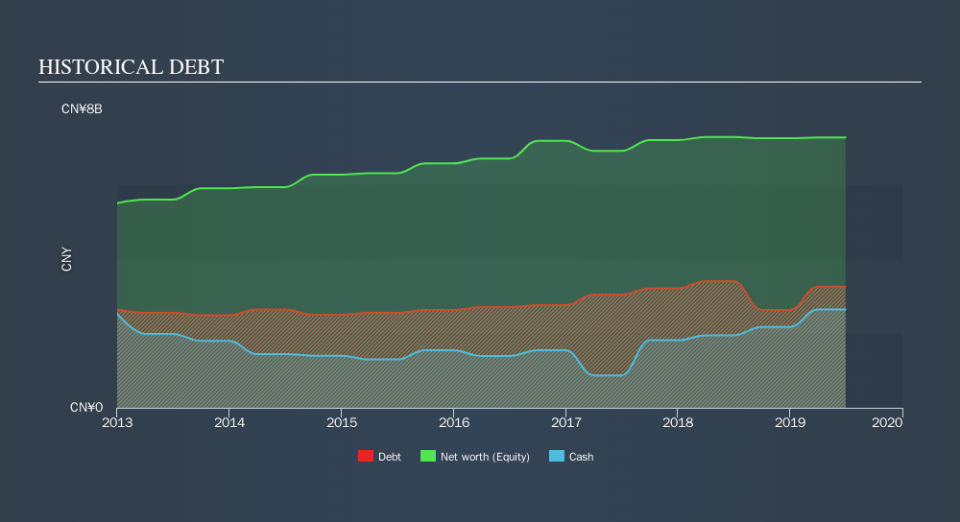

What Is Chongqing Machinery & Electric's Net Debt?

As you can see below, Chongqing Machinery & Electric had CN¥3.25b of debt at June 2019, down from CN¥3.58b a year prior. However, it does have CN¥2.64b in cash offsetting this, leading to net debt of about CN¥614.6m.

A Look At Chongqing Machinery & Electric's Liabilities

The latest balance sheet data shows that Chongqing Machinery & Electric had liabilities of CN¥7.11b due within a year, and liabilities of CN¥3.07b falling due after that. Offsetting these obligations, it had cash of CN¥2.64b as well as receivables valued at CN¥6.10b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥1.44b.

This deficit is considerable relative to its market capitalization of CN¥1.84b, so it does suggest shareholders should keep an eye on Chongqing Machinery & Electric's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Chongqing Machinery & Electric will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Chongqing Machinery & Electric had negative earnings before interest and tax, and actually shrunk its revenue by 42%, to CN¥5.0b. That makes us nervous, to say the least.

Caveat Emptor

While Chongqing Machinery & Electric's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost CN¥93m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled CN¥194m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. For riskier companies like Chongqing Machinery & Electric I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.