We Think Fiat Chrysler Automobiles (BIT:FCA) Is Taking Some Risk With Its Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Fiat Chrysler Automobiles N.V. (BIT:FCA) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Fiat Chrysler Automobiles

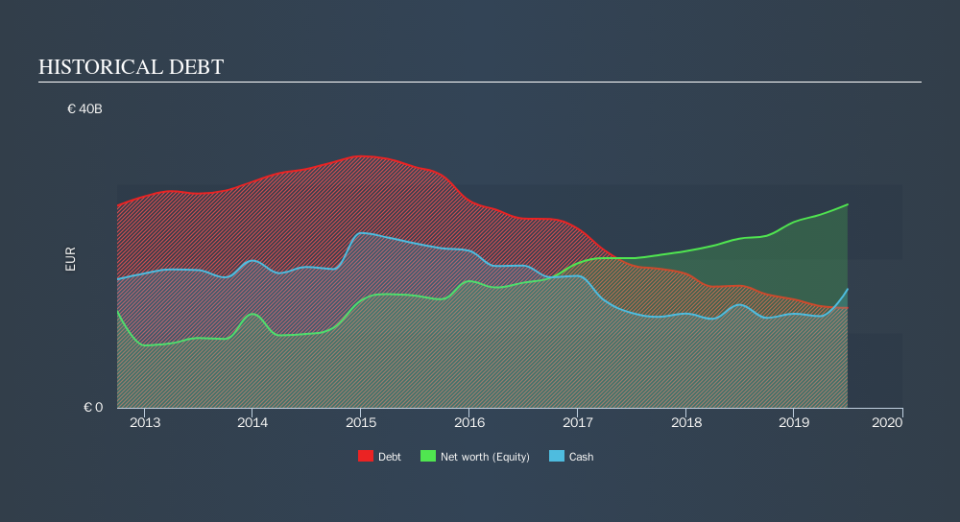

What Is Fiat Chrysler Automobiles's Net Debt?

The image below, which you can click on for greater detail, shows that Fiat Chrysler Automobiles had debt of €13.4b at the end of June 2019, a reduction from €16.4b over a year. However, it does have €15.9b in cash offsetting this, leading to net cash of €2.50b.

How Strong Is Fiat Chrysler Automobiles's Balance Sheet?

The latest balance sheet data shows that Fiat Chrysler Automobiles had liabilities of €46.5b due within a year, and liabilities of €25.4b falling due after that. Offsetting this, it had €15.9b in cash and €4.43b in receivables that were due within 12 months. So it has liabilities totalling €51.6b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the €19.5b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Fiat Chrysler Automobiles would likely require a major re-capitalisation if it had to pay its creditors today. Given that Fiat Chrysler Automobiles has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

But the bad news is that Fiat Chrysler Automobiles has seen its EBIT plunge 14% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Fiat Chrysler Automobiles can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Fiat Chrysler Automobiles may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Fiat Chrysler Automobiles produced sturdy free cash flow equating to 51% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

Although Fiat Chrysler Automobiles's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of €2.5b. Despite the cash, we do find Fiat Chrysler Automobiles's level of total liabilities concerning, so we're not particularly comfortable with the stock. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.