TrueCar, Inc. Just Reported, And Analysts Assigned A US$3.53 Price Target

TrueCar, Inc. (NASDAQ:TRUE) shares fell 7.0% to US$3.48 in the week since its latest annual results. TrueCar reported revenues of US$354m, in line with expectations, but it unfortunately also reported (statutory) losses of US$0.52 per share, which were slightly larger than expected. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for TrueCar

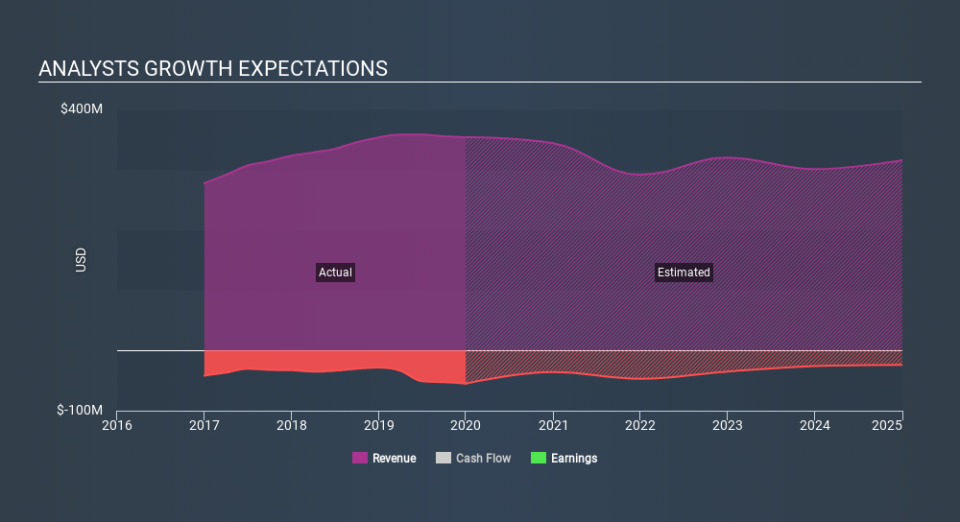

After the latest results, the consensus from TrueCar's twelve analysts is for revenues of US$343.8m in 2020, which would reflect a noticeable 2.9% decline in sales compared to the last year of performance. Per-share statutory losses are expected to explode, reaching US$0.34 per share. Yet prior to the latest earnings, analysts had been forecasting revenues of US$367.5m and losses of US$0.38 per share in 2020. While revenue forecasts have been revised downwards, analysts look to have become more optimistic on the company's earnings power, given the decent improvement in to earnings per share forecasts.

Analysts have cut their price target 32% to US$3.53 per share, suggesting that the declining revenue was a more crucial indicator than the forecast reduction in losses. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic TrueCar analyst has a price target of US$5.25 per share, while the most pessimistic values it at US$2.50. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

It can be useful to take a broader overview by seeing how analyst forecasts compare, both to the TrueCar's past performance and to peers in the same market. These estimates imply that sales are expected to slow, with a forecast revenue decline of 2.9% a significant reduction from annual growth of 10% over the last five years. Compare this with our data, which suggests that other companies in the same market are, in aggregate, expected to see their revenue grow 14% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect TrueCar to grow slower than the wider market.

The Bottom Line

The most important thing to note from these estimates is that the consensus increased its forecast losses next year, suggesting all may not be well at TrueCar. Unfortunately, analysts also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider market. Even so, earnings per share are more important to the intrinsic value of the business. Even so, earnings are more important to the intrinsic value of the business. The consensus price target fell measurably, with analysts seemingly not reassured by the latest results, leading to a lower estimate of TrueCar's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple TrueCar analysts - going out to 2024, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.