Indivior soared to its highest share price since November 2018 on Tuesday after the pharmaceuticals giant reached a settlement with former parent Reckitt Benckiser.

Indivior leapt 16.8p to 144.7p, topping the FTSE 250 index after it was agreed that Reckitt Benckiser would withdraw a $1.4bn claim against the company in relation to its marketing of Suboxone, a treatment for opioid addiction. Its former parent, in contrast, was a top drag on the FTSE 100, losing 178p to £63.76.

Under the terms of the agreement, Indivior agreed to pay its former parent a total of $50m over the next five years. Indivior was spun out of the consumer goods firm in 2014.

Shares in fellow FTSE 250 pharmaceuticals firm UDG Healthcare climbed 41p to 821.5p – the most since the end of November – after it reported first-quarter results and 2021 guidance ahead of analysts’ expectations.

Peel Hunt analysts recommend to buy the stock, saying the company reported a “great” first quarter, including unexpected growth from subsidiary Ashfield.

Elsewhere in the sector, FTSE 100 drug maker AstraZeneca gained 55p to £79.52 after it denied reports its Covid vaccine was not very effective for people over the age of 65.

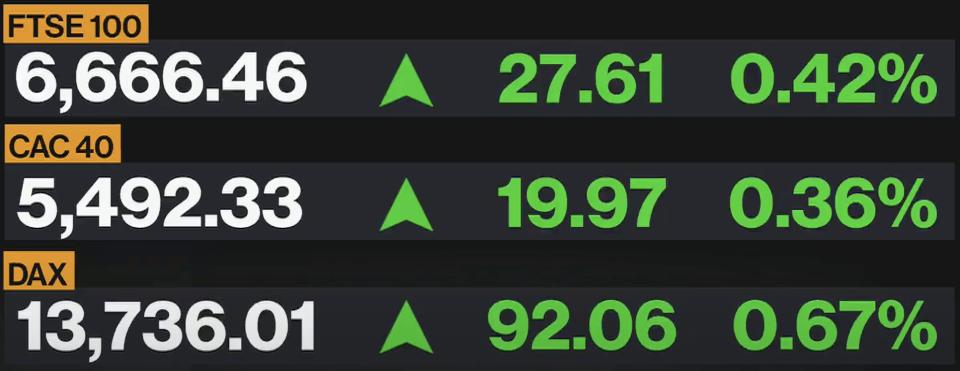

Bullish sentiment took hold of markets on Tuesday, boosted by the International Monetary Fund lifting its expectations for 2021 world growth to 5.5pc, up from 5.2pc in October. It did, however, caution that new variants of the virus are a concern for its outlook.

The blue-chip FTSE 100 index gained a slight 15.16 points to 6,654.01, while the FTSE 250 rose 97.95 points to 20,448.36. The mood was dampened, however, by a jump in Britain’s unemployment rate to 5pc in the three months to November, its highest in nearly five years.

Larger market gains were also offset by a rallying pound, which climbed despite the fresh ONS statistics. It rallied 0.5pc against the US dollar to touch $1.3740 on the back of recovery hopes from the IMF’s predictions.

Among company news, JD Sports told shareholders it is considering a cash-call to help fund its acquisition spree. The sportswear retailer said it is considering options, including an equity placing, to help it “invest in future strategic opportunities”. Shares fell 24.8p to 793.2p.

On the FTSE 250, ticketing platform Trainline was one of the leading fallers in morning trading before recouping losses to end up 4.2p to 409.2p. Traders seemed to shrug off warnings from analysts at JP Morgan that the group faces “unavoidable” cuts to its earnings forecasts amid continued weakness in railway usage.

The US investment bank said the prospects for near-term price gains looked poor, noting that passenger numbers remained “well below” last year’s levels.

Markets Hub embed test

05:56 PM

Wrapping up

That is all from our live blog today. Here are some of our top stories so far:

Numbers on: Industrial profits (China); consumer confidence (France); durable goods orders, Federal Reserve decision (US)

05:49 PM

LVMH sales tumble as Covid hits perfume and jewellery demand

LVMH

Sales at luxury goods giant LVMH tumbled 17pc to €44.7bn (£39.6bn) during 2020 compared with a year earlier, as the pandemic hit demand for perfume and high-end jewellery.

My colleague Hannah Uttley reports:

Profits fell by 28pc €8.3bn over the year, but LVMH noted that it had returned to growth during the second half with earnings up 7pc.

LVMH’s selective retailing arm, which includes make-up brand Sephora, was hit hardest by the coronavirus crisis as local lockdowns forced store closures around the world.

Its watches and jewelry and perfume and cosmetics divisions also suffered from a slump in international travel.

The results come just weeks after LVMH, which is best-known for brands including Louis Vuitton and Christian Dior, completed its $15.8bn purchase of US jeweller Tiffany.

Bernard Arnault, chairman and chief executive of LVMH, said the company had shown “remarkable resilience” during the pandemic.

He said: “In a context that remains uncertain, even with the hope of vaccination giving us a glimpse of an end to the pandemic, we are confident that LVMH is in an excellent position to build upon the recovery for which the world wishes in 2021 and to further strengthen our lead in the global luxury market.”

05:21 PM

Beyond Meat stock leaps on PepsiCo deal

Beyond Meat

Shares of plant-based group Beyond Meat are surging after it launched a joint venture with PepsiCo.

The partnership aims to produce sustainable products, with the fizzy drink firm expected to launch lines this year under the name Planet Partnership.

LA-based Beyond Meat - founded in 2009 - earlier rose 26pc to $199.38, while PepsiCo's were slightly up at $141.50.

It comes amid a rising trend of veganism among consumers that has supported the growing popularity of plant-based foods. Shoppers are also, more generally, looking for healthier snacks and are becoming more aware of sustainability issues surrounding the food they eat.

05:03 PM

Bob Seely weighs in on HSBC grilling

Commenting on the HSBC inquiry earlier today, Bob Seely, MP and IPAC member, said:

"HSBC are happy to virtue signal in the West, yet desperate even to avoid any ethical debate in HK. Their customers can make up their own minds about HSBC’s ‘values’.

"None of Mr Quinn's answers have given me any confidence that HSBC has adequately engaged with this issue."

04:59 PM

EU could be liable for damages if it blocks Covid vaccine exports

Astra

The European Union could face compensation claims from pharmaceutical firms if a possible ban on exporting Covid vaccines from the bloc prevents them fulfilling existing orders overseas, according to trade lawyers.

My colleague Michael O'Dwyer reports:

On Monday, Stella Kyriakides, EU health commissioner, proposed forcing vaccine manufacturers to disclose where exports from the bloc are being sent as the EU faces problems getting supplies of the Covid jab.

Production shortfall at AstraZeneca threatens to leave the EU with tens of millions fewer vaccines than expected.

Trade rules prevent export bans that are discriminatory, meaning any export restrictions would likely need to apply to all vaccine-makers and not just AstraZeneca, said Eric White, a trade law consultant at Herbert Smith Freehills.

EU and World Trade Organisation rules mean countries can ban exports only in limited circumstances such as a shortage of an essential product.

If new restrictions are introduced, pharmaceutical firms could argue that they should still be allowed to fulfil existing orders, Mr White said.

“If they have a contract with a country like the United States to supply and then if this would measure would lead them to breach the contract and make them liable for damages [to the buyer] that could be exempted,” he said.

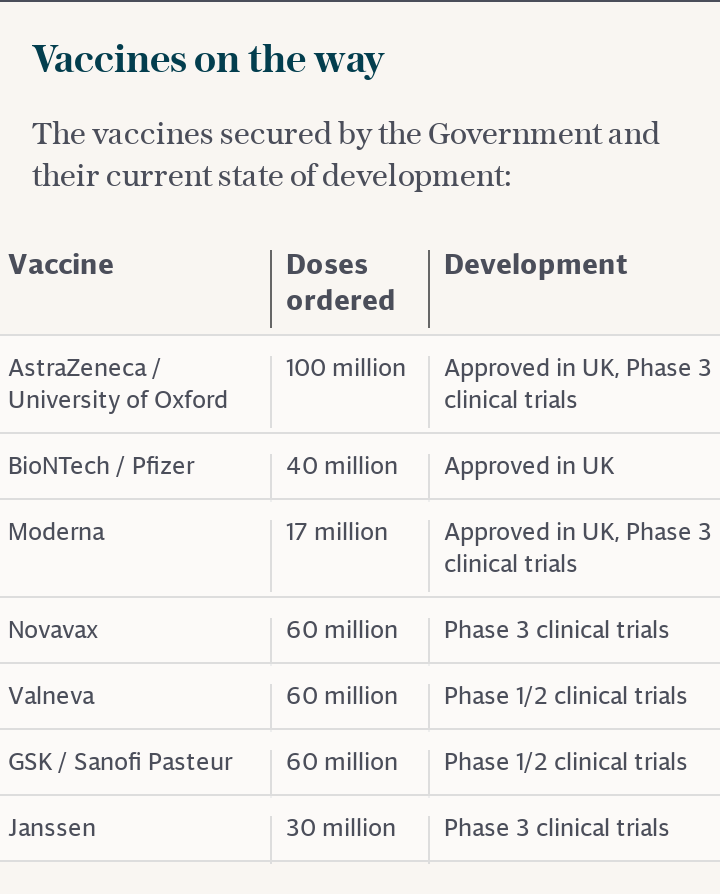

Vaccines secured by the government and current state of development

04:32 PM

Sterling jumps on recovery hopes

Sterling had jumped by about 0.5pc just after markets closed, to $1.3740 as it pulled away from a one-week low against the US dollar.

Markets also edged higher, with the FTSE 100 up about 0.2pc.

Stocks have been boosted by the International Monetary Fund (IMF) which revised its 2021 global growth forecast to 5.5pc, compared to its 5.2pc prediction in October. It did caution, however, that new coronavirus variants are a concern for this year's outlook.

While the pound had fallen in early trading after risk sentiment waned in US and Asian markets overnight, sentiment turned bullish later on as stocks boosted. US markets also hit record highs over strong corporate earnings and the dollar pushed down.

Expectations of a large US fiscal stimulus package in recent weeks, meanwhile, has helped to fuel risk sentiment and in turn benefitted the pound.

04:04 PM

MPs grill HSBC's Noel Quinn pt.2: CEO repeats he is not a politician

Noel Quinn

My colleague Lucy Burton continues:

When asked by MPs if what the bank was doing was unethical, Noel Quinn responded: "I'm the CEO of a bank, I'm not a politician" adding that he was reluctant to talk about "one country versus another, because I operate in 60 countries".

Mr Quinn said he can't be "judge and jury" for every police request the bank gets.

When asked why the bank endorsed the law, Mr Quinn said 2.9m citizens in Hong Kong signed the petition and that he witnessed the destruction taking place due to anti-government protests."It was not a political statement," he said.

Three banks in Hong Kong were asked to freeze the accounts of pro-democracy politician Ted Hui and his family by police last month. Mr Hui called on UK MPs to look into the matter.

During the hearing the bank was accused of "double standards" and "hypocrisy" which may put customers off using the lender. Mr Quinn said in response that he's doing everything he can to support the people of Hong Kong.

When asked about the crushing of democracy, Mr Quinn said "we've seen good times and bad times" in Hong Kong over the years, repeating that he is not a politician.

04:01 PM

MPs grill HSBC's Noel Quinn pt.1: bank will not walk away from HK

HSBC

HSBC's chief executive Noel Quinn and compliance head Colin Bell have been hauled in front of MPs for a hearing which will focus on why the bank has frozen the accounts of pro-democracy activists in Hong Kong.

My colleague Lucy Burton reports:

This is the first time a HSBC executive has been publicly questioned by ministers since it backed Beijing's controversial security law last year, which criminalises anti-government movements in Hong Kong. Concerns about the bank's support for the crackdown have risen in recent weeks after it began freezing activists' accounts.

Mr Quinn told the foreign affairs committee that the bank has only frozen accounts when it was legally required to do so and does not make freezing decisions based on political activity. He said the bank would commit a criminal offence if it ignored orders.

"I can not cherry-pick which law to follow and which law not to follow as the CEO of a financial institution," he said. "[I'm] not making a moral judgment, I have to comply with the law."

He said he has been speaking to the UK regulator about the situation in Hong Kong, as reported by The Telegraph last year, but has had no dialogue with the UK government.

"Am I willing to walk away from Hong Kong? The answer is no," he said.

03:32 PM

Handover

That's all from me. My colleague Louise Moon will take over for the rest for the rest of the day.

Thanks for following!

03:23 PM

Exclusive: Arcadia collapsed under £750m debt mountain

Philip Green

Sir Philip Green’s retail empire collapsed under the weight of debts totalling £750m, new filings reveal.

My colleagues Laura Onita and Oliver Gill report:

Reports prepared by Deloitte, appointed as Arcadia’s administrator at the end of November, reveal the perilous state of the finances of some of the high street’s best-known brands.

Topshop and Topman failed with gross liabilities of more than £550m. Meanwhile discount brand Outfit owed £80m, according to analysis sent to creditors and seen by The Telegraph.

The filings do not indicate how Arcadia’s implosion will affect the 9,000 members of its pension scheme or its outstanding obligations to the taxman.

A detailed listing does not include unsecured amounts owed to the Arcadia retirement fund and unpaid VAT due to HM Revenue and Customs.

Deloitte said it would update creditors, including landlords and suppliers, as it gathered further information, but warned the total amount was expected to be materially higher than its current calculations.

Asos confirmed on Monday it was in exclusive talks to buy the Topshop, Topman, Miss Selfridge and HIIT brands. It has no plans to acquire the stores, putting most of the group’s 13,000-strong workforce at risk.

City of London Corporation approves 30-storey office block

City of London

A 30-storey office-led development in the Square Mile has been approved by the City of London corporation.

My colleague Ben Gartside reports:

The Tenacity Group, based in Hong Kong, said the building will contain features such as a terrace, a suspended treetop walkway and panoramic views across London.

Chair of the Planning and Transportation Committee at the City of London Corporation, Alastair Moss, said: “We remain positive about the long-term future of the City office despite the current lockdown. It is fantastic, therefore, to see this significant vote of confidence from the developers of 55 Gracechurch Street."

Tenacity Group Chief Executive Patrick Wong said: “Today marks a significant milestone for us and underlines our commitment to the City of London and the future of truly sustainable office buildings in the City.

“Despite the events of the last twelve months and the changes and challenges that we have all witnessed, Tenacity is quite clear that the era of the office is not over. Far from it.

“Today’s decision reinforces that view, and we look forward to working with the City to bring our vision for 55 Gracechurch Street to fruition.”

02:40 PM

Wall Street opens higher

US stocks started the day in positive territory despite concerns about new Covid variants and hurdles to a fresh aid package.

US market data - Bloomberg

01:59 PM

Analysis: Sunak holds back tide of job losses

Our Economics Editor Russell Lynch has taken a close look at this morning’s labour market figures – which, he says, show that (for now) the Chancellor has prevented a surging in unemployment. Russ writes:

Despite some more visible scars such as the record rise in redundancies to 395,000 over the quarter, the anomaly remains the official 5pc unemployment rate in the Office for National Statistics’ figures.

Official data count only those who are looking for work as unemployed, although the Bank of England Governor, Andrew Bailey, has estimated that a more realistic unemployment estimate is around 6.5pc, some 500,000 higher than implied by the latest numbers.

Minister: We have no plans to extends hospitality VAT relief

Treasury minister Jesse Norman has told the commons that Commons that the Government has no intention to extend a temporary VAT cut for the tourism, hospitality and leisure industries.

At present, the sectors are charging just 5pc VAT, compared with the usual 20pc, with the relief due to wind up at the end of March.

Mr Norman told MPs:

The relief comes at a significant cost, and while the government keeps taxes under review, it has no current plans to extend it further.

01:22 PM

Crest Nicholson repay furlough cash and brings dividend back

Crest Nicholson has repaid Government furlough money and reinstated it's dividend following above expectation results.

My colleague Ben Gartside reports:

The housebuilder justified the decision by saying it expected demand to stay strong following the end of the stamp duty holiday,

In the year to October 31st, the number of houses sold dropped 23pc, and revenue dropped 38pc to £677m. Crest Nicholson recorded a a statutory pre-tax loss of £13.5 million, due to the re-valuing of certain sites and the impact of Covid. Excluding one-off costs, it recorded a profit of £45.9m, ahead of city projections.

The figures still mark a significant reduction compared to the previous year, where the company recorded a statutory pre-tax profit of over £100m.

Broker Peel Hunt said: “After a good end to the year, Crest delivered FY20 results 6% ahead of consensus and above the top end of the guided range. The turnaround plan is progressing well, with significant cost savings now embedded in the business.”

01:13 PM

IMF lifts growth outlook but warns of new virus variants

New Covid variants and stalling vaccine rollouts threaten to hamper the global economy’s recovery, the International Monetary Fund warned as it slashed its growth forecasts for the UK and eurozone.

My colleague Tom Rees reports:

The lender of last resort lifted its global GDP growth forecast for 2021 by 0.3 percentage points to 5.5pc but delivered heavy downgrades across Europe as the region battles the second wave of infections.

The IMF struck a cautious tone over predictions of a rapid bounce back, warning that “much remains to be done on the health and economic policy fronts” amid “exceptional uncertainty”.

“Although recent vaccine approvals have raised hopes of a turnaround in the pandemic later this year, renewed waves and new variants of the virus pose concerns for the outlook,” the IMF said in its latest World Economic Outlook Update.

BlackRock’s Fink says pandemic has triggered green investment boom

BlackRock - REUTERS/Lucas Jackson/File Photo

BlackRock boss Larry Fink has told company bosses that the pandemic has accelerated a “tectonic shift” towards investing in companies that are managing the risks posed by climate change.

My colleague Michael O’Dwyer reports:

Investors are increasingly concerned about the dangers to companies, not just from extreme weather events such as floods and hurricanes, but also from tightening regulations as governments take more action to slow the speed of global warming.

In his annual letter to chief executives, Mr Fink said the pandemic had accelerated trends from a “retirement crisis to systemic inequalities” and signalled that sustainability is now firmly at the top of the investment agenda.

The funds veteran said that predictions that the virus would derail investors’ and companies’ interest in reducing global warming had proven wide of the mark.

He said: “In March, the conventional wisdom was the crisis would divert attention from climate. But just the opposite took place, and the reallocation of capital accelerated even faster than I anticipated.”

Between January and November last year, investors in mutual funds and exchange-traded funds poured $288bn (£210bn) into “sustainable assets”, almost double the level in 2019.

"In this letter I asked companies to do more than just report under TCFD and SASB," says BlackRock CEO Larry Fink on his annual letter to CEOs. "I asked them to report their path towards a net zero carbon footprint, and how are they going to get that." pic.twitter.com/KOHvpzr3pq

European markets have only increased their gains since the open, pushing steadily higher despite a pretty downbeat economic and virus backdrop. Some mild M&A fever across the continent is giving a boost to stocks.

The pound is now up against the dollar, in a move that signals risk-on sentiment but has also put a drag on the FTSE 100’s performance.

12:37 PM

Greencore sales continue to slump

Sandwich - Adam Gault/Getty Images Contributor

Sandwich maker Greencore unveiled a further slump in sales and warned coronavirus restrictions continued to hammer trade as fewer workers commuted to the office.

My colleague Hannah Uttley reports:

Greencore, a supplier to major supermarkets such as Tesco and Marks & Spencer, said sales of its food-to-go products fell 22pc in the 13 weeks to Christmas Day as Government restrictions such as the regional tier system limited travel across the UK.

Sales of its other convenience foods, which include its ready meal ranges, fell 2pc, with total revenue for the period down 15pc to £312.7m compared with a year earlier.

Greencore also supplies convenience and travel retail outlets, discounters and coffee shops. Last year it manufactured 619m sandwiches and other food-to-go products.

Greencore warned that sales have worsened since the reported period, with group revenues currently running 20pc lower than prior year levels as a result of the national lockdown. Food-to-go revenue is down by around 35pc, the company said.

Banks in Europe have started the reporting season off to a strong note after UBS, the world’s largest wealth manager, unveiled a 137pc bump in profits for the fourth quarter.

My colleague Lucy Burton reports:

Investors had high hopes for the Swiss bank after Wall Street reported a strong year and a record end to 2020 despite the pandemic leaving many households significantly poorer. UBS beat expectations with a fourth quarter profit of $1.7bn, 137pc higher than the same period a year ago.

The bank now plans to buy back $4.5bn worth of shares in the next three years, starting with buying back $1.1bn worth in the first quarter of this year. These are the first results under new chief executive Ralph Hamers.

12:08 PM

Merkel speaking at Davos

German Chancellor Angela Merkel is now speaking at the World Economic Forum. In her opening comments, she says that the pandemic shows how interconnected humanity is with nature.

Shares in Etsy, the online ecommerce platform for selling handmade goods, have jumped about 4pc in premarket trading after Tesla founder Elon Musk said he “kind love[s]” the website.

It’s the latest in a near-constant string of bizarre markets moves prompted by high levels of retail trading.

Bought a hand knit wool Marvin the Martian helm for my dog

Data watchdog chief slams WhatsApp over privacy changes

Elizabeth Denham, the information commissioner, is currently in front of Digital, Culture, Media, and Sport sub-committee on Online Harms and Disinformation.

My colleague Michael Cogley reports:

It’s already been a fascinating session, with Ms Denham admitting she never uses Facebook or WhatsApp, only Signal. She’s also hit out at WhatsApp’s new privacy changes which have been described as a “personal data grab”.

In another revelation that has angered some, Denham has revealed that highly-anticipated details of a legal settlement with Facebook as part of its Cambridge Analytica investigation will not be made public.

AstraZeneca offers EU earlier vaccine supplies in February – Reuter

Reuters reports:

AstraZeneca has offered to provide the European Union with earlier supplies of its COVID-19 vaccine in February but has not given clarity on the possible rerouting of doses from Britain to boost EU deliveries, EU officials told Reuters on Tuesday.

Reuters: EXCLUSIVE-ASTRAZENECA PROPOSED TO THE EU TO BRING FORWARD START OF SUPPLIES OF VACCINE TO FEB 7 FROM 15 -EU SOURCES ASTRA DID NOT ANSWER EU QUESTIONS ON WHETHER IT COULD DIVERT TO THE EU DOSES PRODUCED IN UK IN Q1 TO BOOST EU SUPPLIES -EU SOURCE #COVID#EU#AstraZeneca

Ticketing platform Trainline is leading fallers on the FTSE 250 today, after analysts at JPMorgan warned the group faces “unavoidable” cuts to its earnings forecasts amid continued weakness in railway usage.

The US investment bank warned the prospects for near-term price gains looked poor, noting that passenger numbers remain “well below” last year’s levels.

Analyst Marcus Diebel slashed Trainline’s price target from 486p to 382p and cut its estimates for the group’s financial performance. he said:

While we highlighted that an ongoing shift towards the concession model in the UK rail industry is unlikely to meaningfully change Trainline’s offering and business model, we expect ongoing negative sentiment to impact the shares.

11:05 AM

AstraZeneca hits back at vaccine efficacy claims

AstraZeneca has hit back at reports in German media that claimed its Covid vaccine had low efficacy in over 65s, labelling the claims as "completely incorrect", while the German health ministry said the reports were false.

My colleague Simon Foy reports:

The drugmaker was forced to issue a blistering denial after a report in Handelsblatt, Germany’s leading financial daily, claimed the Oxford/AstraZeneca vaccine is only 8pc effective in people over the age of 65, citing unnamed German officials.

A separate report in tabloid Bild claimed German officials do not believe the AstraZeneca jab will receive approval from the European Medicines Agency for use on over-65s.

However, the German health ministry denied the reports on Tuesday morning, saying the data does not suggest efficacy of just 8pc. Rather, the 8pc figure referred to the number of people aged between 56 and 69 who took part in the study. It expects the EMA decision on the Oxford vaccine to be announced on Friday.

The digital World Economic Forum (aka Davos) enters its second day today, with the great and occasionally good of globalism making appearances during the week.

There are three key speakers today: EU Commission President Ursula von der Leyen, German Chancellor Angela Merkel, and French President Emmanuel Macron.

This year’s WEF is on the theme of the ‘Great Reset’, which includes economic reforms and changes aimed at tackling climate change.

Ms Von der Leyen is speaking currently, with Ms Merkel speaking at 12pm GMT, and Mr Macron at 2pm GMT.

Rolls-Royce - Rolls-Royce Deutschland / Steffen Weigelt

Rolls-Royce has warned that new and more infectious variants of coronavirus have created uncertainty that will continue to hammer the aviation industry in 2021 as it downgraded its cash flow forecast for the year.

My colleagues Simon Foy and Alan Tovey report:

The blue-chip aerospace engineer expects to burn through £2bn of cash this year, £500m higher than analyst expectations. It warned that more contagious Covid variants will delay the recovery in air travel.

As a result of the continued uncertainty, the number of flying hours for its wide-body engines is expected to decline to just 55pc of 2019 levels, compared with previous guidance of 70pc.

Rolls’s civil aerospace business normally generates half of the company’s total revenues, with customers charged for the number of hours they use jet engines.

Indivior rises after reaching settlement with Reckitt Benckiser

Shares in pharma group Indivior have risen sharply today after it reached a settlement with consumer goods giant Reckitt Benckiser over a $1.4bn claim by the latter.

Under the terms of the agreement, Indivior agreed to pay RB a total of $50m over the next five years.

RB’s claim reportedly related to a $1.4bn settlement reached between the group and the US Department of Justice in connection to Indivior’s marketing of suboxone, a treatment for opioid addiction. Indivior was spun out of RB in 2014.

09:02 AM

Pound down against dollar

The pound has slipped against most of its major international peers following this morning’s labour market data, including a 0.3pc fall against the dollar. The US currency is strengthening broadly as a nervous mood holds across markets.

08:47 AM

Labour market data reaction: Rebound should keep unemployment from financial crisis levels

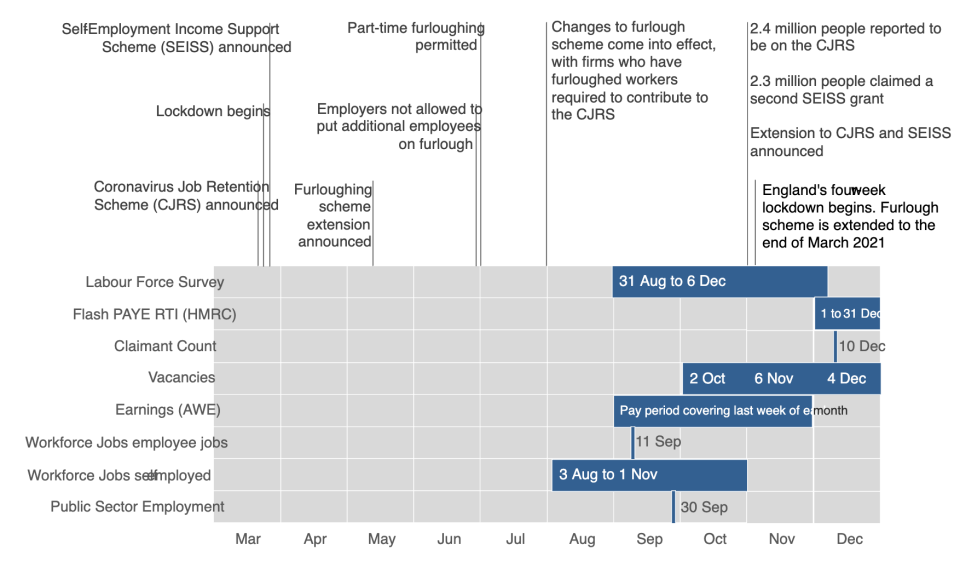

Today’s labour market report was incremental in many ways: unemployment is continuing to tick up slowly, with the biggest factor in future moves likely to be how long the furlough scheme stays around for.

Thomas Pugh, from Capital Economics, said:

Overall, the labour market will probably continue to weaken over the rest of this year, especially once the furlough scheme finishes at the end of April. But a rapid rebound in GDP in the second half of this year should prevent the unemployment rate from reaching GFC levels.

Yael Selfin from KPMG noted that a tighter labour market due to Brexit could also limit joblessness:

[The] labour market is also shrinking following the UK exit from the EU. More EU nationals are leaving and fewer are likely to come in future. This is keeping the unemployment rate lower, but will also make it harder for employers to fill some vacancies.

Samuel Tombs from Pantheon Macroeconomics says that some people who left the country in the face of the pandemic may return, Hwever, increasing competition for roles:

[At] least 600K non-UK nationals left the UK last year and might return later this year, provided they submitted the right paperwork before they left.

08:27 AM

Young people have borne brunt of job losses

Today’s ONS figures show young people have taken the heaviest job losses as a result of the pandemic – despite signs of a bounceback, there were about 200,000 fewer 16- to 24-year-olds in work between September and November than a year before.

There are also worrying signs over a drop in employment among 35- to 49-year-olds – we will have to see how that develops in the coming months.

08:14 AM

European markets pick up after initial drop

European markets dropped straight after the open, but have bounced back into the green pretty quickly, and are now moderately up following a sharp drop yesterday.

Bloomberg TV - Bloomberg TV

08:10 AM

Hit to lower-paid jobs pushes up pay growth

Annual growth in average employee pay continued to strengthen in November, a rise which the ONS said is increasingly being driven by a fall in the number and proportion of lower-paid jobs.

The ONS said:

Current average pay growth rates are being impacted upwards by a fall in the number and proportion of lower-paid jobs compared with before the Covid-19 pandemic; it is estimated that underlying wage growth – if the effect of this change in profile of jobs is removed – is likely to be under 2pc.

07:55 AM

Vacancies recover

A recovery in UK job vacancies continued to lose pace at the end of 2020, with the job in job postings between October and December at half the previous quarter’s levels.

07:43 AM

Making sense of today’s data

The ONS has produced this helpful breakdown of the different measures in today’s release, and the time periods they cover:

ONS - ONS

07:40 AM

Economic activity broadly unchanged

Economic activity rates shifted only slightly during November, with the rate for women falling as activity among men picked up:

07:28 AM

Redundancies peaked in September

A more granular look at redundancies data suggests the biggest spike in job losses over the period occurred in late September, with the figures easing off somewhat over the subsequent weeks:

07:21 AM

PAYE payrolls increase slightly

HMRC’s experimental PAYE payrolls count data suggests a slightly pickup in jobs during December, with the total count rising slightly. As noted earlier, the figures are very volatile: but at this point, they suggest that around 830,000 jobs have been lost since February 2020.

07:13 AM

Claimant count still elevated

The total count of Britons claiming benefits due to unemployment was barely changed in December, holding just above 2.6m. The experimental measure – which tracks claimants of Jobseekers’ Allowance and certain forms of Universal Credit – has held fairly steady after soaring in the wake of 2020’s initial lockdowns.

07:08 AM

Redundancy rate hits record high

The UK’s redundancy rate climbed 10 points over a year to hit 14.2 per thousand in the three months to the end of November – a record high.

07:03 AM

Unemployment hits 5pc

Unemployment in the UK continued to rise, hitting 5pc over the three months to the end of November. That’s slightly less than the 5.1pc expected by economists.

06:56 AM

What to expect from today’s figures

As ever, the Office for National Statistics’ labour market data will be something of a smorgasbord – with varied collection methods yielding a mixture of data points.

The headline figure will be unemployment, which is measured on a three-month basis using International Labour Organisation methodology that makes is comparable with other countries’ figures.

Economists polled by Bloomberg expect unemployment to reach 5.1pc in the three months to the end of November. That would be a nearly five-year high, but would remain low given the scale of economic crisis triggered by coronavirus and associated restrictions.

That relatively modest rise has pinned on two key factors: the furlough scheme, which is likely to be keeping some people in jobs that will not continue when the support scheme unwinds, and a large number of Britons who are neither working nor seeking work not yet defining as unemployed.

Forecasts by the Office for Budget Responsibility project unemployment will hit a peak in the second quarter of 2021 after the furlough scheme lapses. That is currently slated for the end of April, but the Treasury has already shown a willingness to repeatedly extend the scheme.

Some companies may have cut jobs in October as it appeared the furlough scheme would lapse at the end of that month – those job cuts would show up in today’s figures. Meanwhile, jobs cut during the November lockdowns probably won’t show up until December’s data.

There will also be a string of other measures, including redundancies (which hit a record high in the three months to the end of October), unemployment support claimant levels, job vacancies and average earnings.

There will also be HMRC payrolls data. One of the best measures of ‘true’ job losses in the opening months of the crisis, it has (as experimental data so often does) proved to be unstable and prone to corrections – but is still well worth looking at.

06:41 AM

Agenda: Unemployment rise set to continue

Good morning. UK unemployment is expected to continue to creep higher in the latest UK labour market figures, set for release at 7am.

Joblessness has risen sharply in recent weeks, but remains subdued but recent levels – something economists have ascribed to the the flattering effects of the Government’s furlough scheme.

Elsewhere, there are a handful of UK companies set to release updates today. The FTSE 100 is set to open flat after a sharp fall yesterday and headwinds from Asia overnight.

3) Call for self-employed to pay more tax: The Institute for Fiscal Studies' has called for tax reforms that could increase bills for millions of self-employed workers and business owners.

Former NBA guard Darius Morris has died at the age of 33. He played for five teams during his four NBA seasons. Morris played college basketball at Michigan.

Jason Fitz and Frank Schwab join forces to recap the draft in the best way they know how: letter grades! Fitz and Frank discuss all 32 teams division by division as they give a snapshot of how fans should be feeling heading into the 2024 season. The duo have key debates on the Dallas Cowboys, New York Giants, New Orleans Saints, Los Angeles Rams, New England Patriots, Las Vegas Raiders and more.