Vishay Intertechnology (NYSE:VSH) Seems To Use Debt Quite Sensibly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Vishay Intertechnology, Inc. (NYSE:VSH) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Vishay Intertechnology

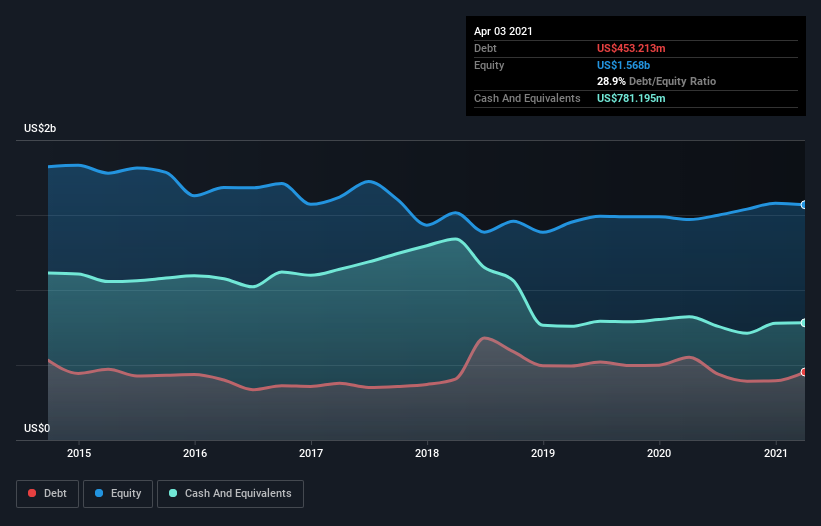

What Is Vishay Intertechnology's Debt?

As you can see below, Vishay Intertechnology had US$453.2m of debt at April 2021, down from US$552.3m a year prior. But it also has US$781.2m in cash to offset that, meaning it has US$328.0m net cash.

How Healthy Is Vishay Intertechnology's Balance Sheet?

We can see from the most recent balance sheet that Vishay Intertechnology had liabilities of US$588.0m falling due within a year, and liabilities of US$1.05b due beyond that. Offsetting these obligations, it had cash of US$781.2m as well as receivables valued at US$385.2m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$475.7m.

Since publicly traded Vishay Intertechnology shares are worth a total of US$3.12b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Vishay Intertechnology boasts net cash, so it's fair to say it does not have a heavy debt load!

Also good is that Vishay Intertechnology grew its EBIT at 14% over the last year, further increasing its ability to manage debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Vishay Intertechnology's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Vishay Intertechnology may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Vishay Intertechnology's free cash flow amounted to 40% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Summing up

While Vishay Intertechnology does have more liabilities than liquid assets, it also has net cash of US$328.0m. And it also grew its EBIT by 14% over the last year. So we don't have any problem with Vishay Intertechnology's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - Vishay Intertechnology has 1 warning sign we think you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.