How Wall Street cashed in on the American Dream: Homebuyers outbid in droves by investors

This is the first in a series investigating the impact on Indianapolis homeowners and renters of corporations that buy up large numbers of homes and convert them into rentals.

First-time homebuyers Michael Wathen and his fiancé thought they’d found their future home in a spacious brick 3-bedroom bungalow in Decatur Township. They’d fallen in love. She was moving from Cincinnati. He lived with his parents, saving for two years to afford a hefty down payment for their dream.

Then, like thousands of other Indianapolis families, they were outbid by a real estate investment company that bought their dream home for 5% more than the listing price of $170,000. Now, what could have been their first home as a married couple is being rented out by Progress Residential, one of Indianapolis’ largest companies that rent houses.

"There's no way you can ever succeed with this," Wathen said. "If you play by the rules, it's like somebody else has a cheat code while you have your regular cards to play with. It was very difficult."

IndyStar Investigations: How a mega investor turned affordable homes into rental nightmares

An Indianapolis Star investigation into institutional investor-owned houses in Marion County found five of the biggest real estate investment companies and their apparent affiliated limited liability companies control at least 5,943 of Indianapolis’ homes as of February 2023, based on analysis of property tax records from Attom Data and the Fair Housing Center of Central Indiana. Another six control at least 1,521 more.

The largest owners are mostly out-of-state companies:

New York City-based private equity firm Cerberus Capital Management owns the most, with at least 1,700 homes, which are managed by its property management affiliate, FirstKey Homes.

Second is Dallas-based VineBrook Homes with at least 1,400 homes.

Third is New York City-based private equity firm Pretium and its property management subsidiary, Progress Residential, with at least 1,000 homes.

Fourth is Indianapolis-based SLB Investments, which is managed by Marshall Welton, the man behind a predatory rent-to-own scheme that was subject to a federal lawsuit by the Fair Housing Center in 2018, with at least 800 homes.

Fifth is the nationwide giant, Las Vegas-based AMH, formerly American Homes 4 Rent, with at least 800 homes.

Indianapolis’ rental housing market has been especially affected by these mega investors. As of June 2023, 17% of houses for rent in the Indianapolis metropolitan area are owned by investors that own more than 1,000 homes in the city, according to data from John Burns Research and Consulting, compared to just 3% nationwide.

These investors are buying up homes en masse in Indianapolis with often unbeatable cash offers, pricing out low to moderate income homebuyers, and flipping them to rent, squeezing housing supply in neighborhoods on the far east side, Lawrence, the west side and the southeast side where investors are extremely dominant and where there’s already shortage of affordable homes.

It also makes homeownership more expensive, Ball State University economics professor Michael Hicks said, as the research shows increased investor activity in neighborhoods drives up how much of someone’s income they spend on housing, especially for entry-level, lower-cost homes.

The cost is more than a title deed lost. It is the foreclosure of the American dream of homeownership for low to moderate-income families. The homeownership rate in Indianapolis has decreased to just 54% since 2010, even though the number of homes in the city has increased, according to a 2022 report by the Fair Housing Center.

The challenge is particularly acute for Black and Hispanic families. The Black homeownership rate in Indianapolis has dropped 30% from 1970 to 2019, the same report found.

Investment companies, rental providers and industry representatives interviewed by IndyStar pointed out that large institutional owners of rental housing, or those that own more than 1,000 homes, control a small fraction of Indianapolis’ overall housing supply — the estimates range from 2% to 6%, depending on the statistics you use — and that it's implausible that they could drive up home prices in the city overall. Instead, they argue that they provide rental opportunities for people who cannot afford to buy a house to live in neighborhoods of their choice.

Jeff Bennett, who until recently was the senior policy adviser to the mayor and who’s worked extensively on housing policy, said he thinks the rising trend of institutional investors owning Indianapolis homes is problematic. Although the city is unable to compete with such large investors, Bennett said, there are solutions Indianapolis has pursued to attempt to keep homeownership affordable, such as creating a community land trust.

“It takes what were probably historical affordable homeownership opportunities off the market, converting them to rental,” he said.

How Wall Street came to rent homes

Wall Street hasn’t always been in the house rental business at such a huge scale.

After the 2007 to 2010 foreclosure crisis, Wall Street private equity firms and institutional investors started increasingly buying up foreclosed and distressed homes lost by homeowners and “mom-and-pop” landlords.

“The excess supply of housing we had in 2008 was gobbled up by these trusts,” Hicks said. “And they haven’t necessarily let go of them.”

Today, the majority of large investment companies buy homes on the regular market, not at foreclosure sales, David Howard, executive director of the National Rental Home Council, a nonprofit representing the interests of the industry, said.

These well-capitalized firms can buy dozens of homes in one fell swoop, sometimes in a single day, and do business under relatively opaque LLCs, real estate investment trusts and the like.

But the trend of investors squeezing limited housing supply has intensified in Indianapolis particularly in the past decade, exploding to a fever pitch as pandemic-time demand for homes and mortgage rates hitting a 20-year high made it even harder for average families to afford a home.

Indianapolis has long been seen as an affordable haven for families wanting to buy a home to raise children, but the relatively lower housing costs here compared to other major cities is also the very thing that has attracted out-of-state investors in droves.

“For us, affordability is declining, but when the rest of the country looks inward to the Midwest, they can’t believe the value they’re seeing and size of home they get for the price,” real estate agent Rochelle Perkins said.

Investors take advantage of affordability crisis

Investors have cottoned on to the fact that increasingly many families are now destined to be lifelong renters. By their own declaration, the continued success of their business model, profiting from rent checks, relies on the ever-increasing cost of homeownership.

Those in the industry have argued they have nothing to do with driving up housing prices. Their rationale goes: prices are already high and companies are giving an opportunity for people to rent houses they can’t afford to buy.

An AMH statement to IndyStar said large, house rental operators own less than 3% of houses in Marion County, adding that “it would be implausible to conclude that homeownership dynamics in the market are driven by the single-family rental industry.”

But Hicks said that while investor ownership isn’t enough to significantly affect prices across the Indianapolis metropolitan area, the ownership is probably concentrated in a few neighborhoods and drives up prices in those areas.

One thing renters, affordable housing advocates and the rental housing industry agree on is that it is becoming increasingly more costly to pay a mortgage than it is to write a rent check for a house.

“It’s very difficult to secure houses when investors are active in the area,” Steven Meyer, CEO of Intend Indiana, an affordable housing nonprofit, said.

Cash in hand, sight unseen

The vast majority of regular homebuyers can’t afford a home without a mortgage loan. But private equity firms can.

Since 2020, more than 42% of residential sales recorded in Marion County were made with cash, the Fair Housing Center found based on analyzing Marion County Recorder’s Office data.

From 2018 to 2022, out-of-state investors paid in cash in for over 70% of their real estate transactions compared to a third for Indianapolis-based homebuyers, the center found.

“What we are seeing with cash sales is an outrageous reminder of the power and money displacing those without power or money,” Amy Nelson, executive director of the Fair Housing Center of Central Indiana, said.

The investor business model is to buy in cash, “sight unseen,” or without seeing the home first.

According to Perkins, who works with one of the city’s largest real estate investors, AMH, the company rarely looks at the property in-person. They only ever make purchases in cash, she said.

A cash offer is near unbeatable. Sellers prefer cash. Well-capitalized investors can also make offers much higher than the asking price and make up for appraisal gaps that can come with conventional mortgages.

“They’re coming in like gangbusters,” Delores Kennedy, president of the Central Indiana Realtist Association, which works with low-income buyers, said.

Five homebuyers IndyStar interviewed all said they became disheartened after being outbid time and time again.

Wathen burned through an entire checkbook on offers for at least 30 homes that they were then outbid for. Void, void, void, he wrote over and over again.

“It was very difficult,” he said.

Cedric Hill, 54, and Rakesha Hill, 50, know this better than anyone. They lost their first home in the aftermath of the 2008 housing crisis. Their lender, Countrywide Financial Corporation, was accused by the Department of Justice of mortgage discrimination and giving out subprime mortgages to Black and Hispanic homebuyers.

Maybe that’s why it hurt so much, almost a decade and a half later, to repeatedly lose their chance at their dream home when they were outbid in a market dominated by real estate corporations that similarly were out for the buck, Rakesha said, at the expense of middle-class homebuyers.

After painstakingly working to improve their credit score, the Hills qualified for mortgage loans only to realize they were up against competitors who were flush with cash.

Toronto-based Tricon Residential outbid the Hills by $50,000 on a stone house in Raymond Park, property records show. Tricon owns 36,000 rentals in the United States and Canada.

The Hills were also outbid by $40,000 on an east side home with a large front porch and a tree swing that reminded Hill of her childhood.

“You just felt like we were not even in the running, you can’t compete with that," Rakesha said.

Frustrated to the brink of quitting, they finally settled on a home without the porch and backyard deck of Rakesha's dreams. She said she felt like corporate investors take opportunities away, especially from first-time homebuyers.

“They’re not invested in who’s actually in the community," she said. "They don’t care.”

Neighborhood impact

Some neighborhoods have been hit harder than others. Large swaths of the Far Eastside, Martindale-Brightwood and Riverside are now renters’ neighborhoods.

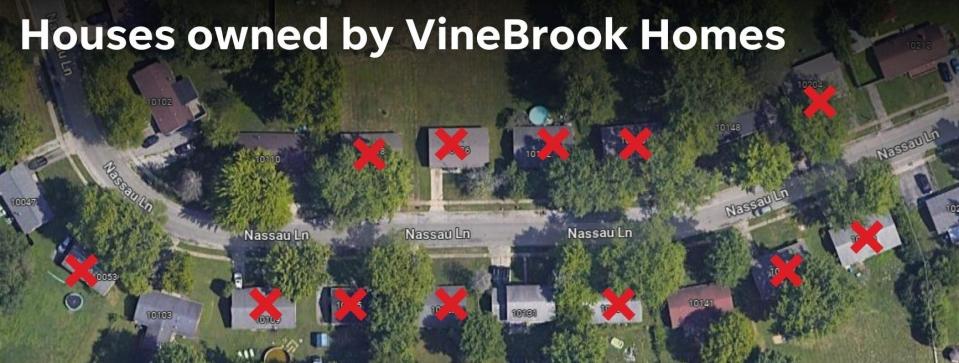

For instance, VineBrook Homes owns 12 out of 21 homes on one block of Nassau Lane on the east side.

Many disinvested neighborhoods that have historically lower property values due to redlining, the discriminatory practice in which residents were denied bank loans simply because their neighborhood was majority-Black, have become easy takings for investors concerned about their bottom line.

More than 7 out of 10 home sales in the last five years in Martindale-Brightwood, Meadows and Riverside were cash transactions, the Fair Housing Center analysis found.

“It was just low-hanging fruit for investors to go in and buy it,” Meyer said.

Nelson described it as a “dogpile of investors,” pointing to the center’s data that shows nearly half of the properties in the gentrifying Martindale-Brightwood and Riverside neighborhoods changed hands in the last three years.

Aggressive cash offers from institutional investors also take homes out of the hands of potential homeowners, for whom owning their own house could make a world of difference.

For Kindra Lesure, 33, a single mom of three kids, owning a home would mean safety and peace of mind that she cannot find in her east side apartment complex. Her car has been shot at. Her family went two weeks without air conditioning this summer. She’s afraid to let her kids go outside.

She’s been searching fruitlessly for a home for two years, having looked at 20 to 30 homes. She wants to stay in Lawrence to be close to her job and her kids’ schools. But she’s finding it hard to secure a home she can afford, within her $200,000 price range.

“I’m still looking but now I’m kind of giving up hope,” she said. “I don’t want to continue to stay here but at the same time, I don’t have a choice."

Indianapolis' largest investors, like VineBrook and SLB Investments LLC, said there is an upside to flipping houses to rentals, giving options to renters.

“It provides an option for people who want to be in a single-family home and one day know that they want to be homeowners, but they’re saving for a down payment,” Howard said. “Or maybe they want to be in a neighborhood in proximity to quality schools because they have kids. They either don’t want to be a homeowner or they're not ready to be a homeowner.”

Investor activity drives up home prices

Investor activity in home markets across the nation tends to increase housing prices and worsen affordability, especially for entry-level houses, a 2021 paper by economists Carlos Garriga, Pedro Gete and Athena Tsouderou found.

“These are usually starter homes that otherwise would be purchased by young households," the paper stated.

Meanwhile, Indianapolis' median home sale prices have only continued to reach historic highs, reaching a record high of $300,000 for the fourth month in a row in August, according to MIBOR data.

Corporate investors declare the ever-increasing cost of homeownership to be advantageous to them. In AMH’s June 2023 investor presentation, the company stated the increased cost of homeownership benefits the company’s single-family rental “value proposition” and that the national housing shortage and growing number of people who rent houses is part of a “favorable supply landscape.”

But purchasing houses in droves isn’t the only investor activity that drives up home prices.

These real estate investors also have a practice of transferring homes they own to LLCs affiliated with themselves, IndyStar found through an analysis of property records, which drives up the “comps” — or the value of comparable properties in the area that the investor is active in.

“They’re securing the investment that they’ve made in real estate by having self-dealings that raise the value of what they already control,” Meyer, who noticed this trend when his organization started a multi-year affordable housing investment on the far east side, said.

For instance, one house in Valley Mills in Decatur Township saw a $15,000 increase in price as it changed hands between LLCs all affiliated with Conrex Residential Property Group, according to property records and a purchase agreement. Conrex's property management company responded to IndyStar by saying that the transactions were between independent funds and individuals.

Indianapolis’ affordable housing developers are also feeling the squeeze.

In 2014, Habitat for Humanity of Greater Indianapolis started to buy homes in need of repair to rehabilitate into affordable housing, but noticed they were increasingly competing against out-of-state real estate investors buying homes in cash and making offers above asking price, the president and CEO, Jim Morris, said.

“We didn’t have that kind of negotiating leverage that was there for them to pay higher,” Morris said.

Up against well-capitalized corporate competitors, Greater Indy Habitat for Humanity was pushed out of the homebuying market and now focuses on buying infill lots on which to build new homes, Morris said.

Looking to solutions

Indianapolis has implemented anti-displacement strategies that allow people to age in their homes, including a property tax break pilot program in Riverside. Also in the works is a city community land trust, which is a novel idea where home resale prices are kept permanently affordable.

“It would be difficult for any city to compete at the scale of those investors,” Bennett said. “Where we’ve tried to focus is neighborhood-based solutions.”

Some homeowners’ associations have taken matters into their own hands, creating rental restrictions in their covenants to prevent investment companies from buying homes in the neighborhood. Admittedly, that's only a solution for a select number of neighborhoods that have such associations and are not already overwhelmed with rentals.

In 2020, the homeowners of Burton Crossing on the southeast side voted to amend the covenants to require a 10-year waiting period before a homeowner can lease or rent their home, with the intention of dissuading corporate investors from buying homes in their neighborhood. Burton Crossing now has no corporate rentals.

The homeowners association president Brian France told IndyStar that corporate rentals have always been the biggest problems for the neighborhood and found they don’t have the same vested interest in keeping up the homes as owner occupants do. France said problems ranged from 12-inch tall grass to broken gutters that go unrepaired.

“Corporations, I hate to say it, is out for the dollar,” he said. “They’ll drain as much rent as they can and put as little in it.”

Without obvious legal, regulatory or free market solutions, aspiring homebuyers said that the homebuying market feels like a game that’s rigged.

When Wathen and his fiancé eventually scored a home of their own, it felt like pure luck. They had been on the verge of giving up.

“My fiancé was telling me, we don't need a house, we know we're still gonna move in together, we could do it with an apartment, it doesn't matter,” he said.

As a final “Hail Mary,” they made one last offer for $175,000 on a home. They were initially outbid by another buyer, but after two weeks, the competitor’s offer fell through. The Wathens were the next best offer.

“It was a miracle,” he said.

Contact IndyStar reporter Ko Lyn Cheang at kcheang@indystar.com or 317-903-7071. Follow her on Twitter: @kolyn_cheang.

Contact business reporter Claire Rafford at 317-617-3402 or email crafford@gannett.com. Follow her on Twitter @clairerafford.

This article originally appeared on Indianapolis Star: Indianapolis real estate: Corporate investors own thousands of homes