We're Excited To See How WAC Holdings (HKG:8619) Uses Its Cash Hoard To Grow

We can readily understand why investors are attracted to unprofitable companies. For example, WAC Holdings (HKG:8619) shareholders have done very well over the last year, with the share price soaring by 145%. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given its strong share price performance, we think it's worthwhile for WAC Holdings shareholders to consider whether its cash burn is concerning. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for WAC Holdings

Does WAC Holdings Have A Long Cash Runway?

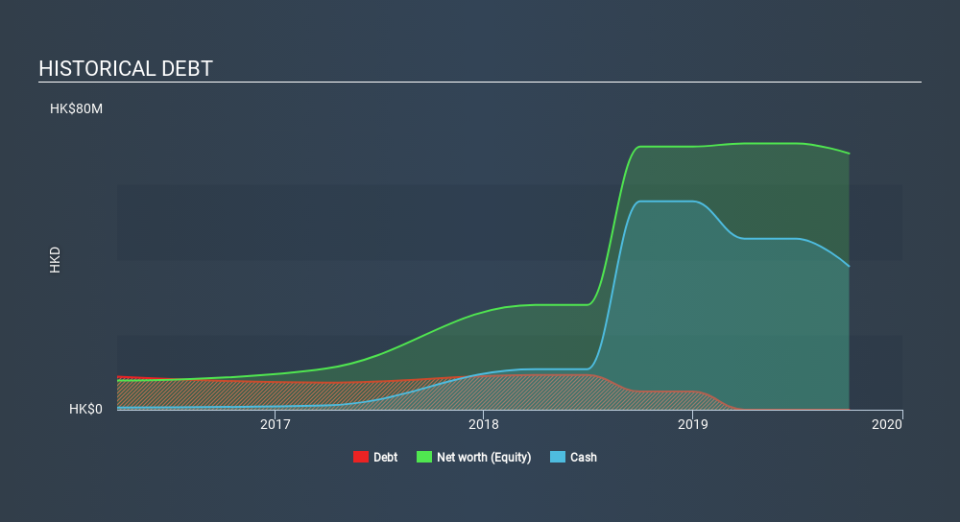

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. When WAC Holdings last reported its balance sheet in September 2019, it had zero debt and cash worth HK$38m. In the last year, its cash burn was HK$12m. Therefore, from September 2019 it had 3.2 years of cash runway. There's no doubt that this is a reassuringly long runway. You can see how its cash balance has changed over time in the image below.

Is WAC Holdings's Revenue Growing?

We're hesitant to extrapolate on the recent trend to assess its cash burn, because WAC Holdings actually had positive free cash flow last year, so operating revenue growth is probably our best bet to measure, right now. Regrettably, the company's operating revenue moved in the wrong direction over the last twelve months, declining by 4.6%. In reality, this article only makes a short study of the company's growth data. You can take a look at how WAC Holdings has developed its business over time by checking this visualization of its revenue and earnings history.

How Easily Can WAC Holdings Raise Cash?

Since its revenue growth is moving in the wrong direction, WAC Holdings shareholders may wish to think ahead to when the company may need to raise more cash. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash to drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of HK$2.5b, WAC Holdings's HK$12m in cash burn equates to about 0.5% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

Is WAC Holdings's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way WAC Holdings is burning through its cash. For example, we think its cash runway suggests that the company is on a good path. While its falling revenue wasn't great, the other factors mentioned in this article more than make up for weakness on that measure. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. Notably, our data indicates that WAC Holdings insiders have been trading the shares. You can discover if they are buyers or sellers by clicking on this link.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.