We're Worried About Hybrid Minerals's (CVE:HZ) Cash Burn Rate

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should Hybrid Minerals (CVE:HZ) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for Hybrid Minerals

How Long Is Hybrid Minerals's Cash Runway?

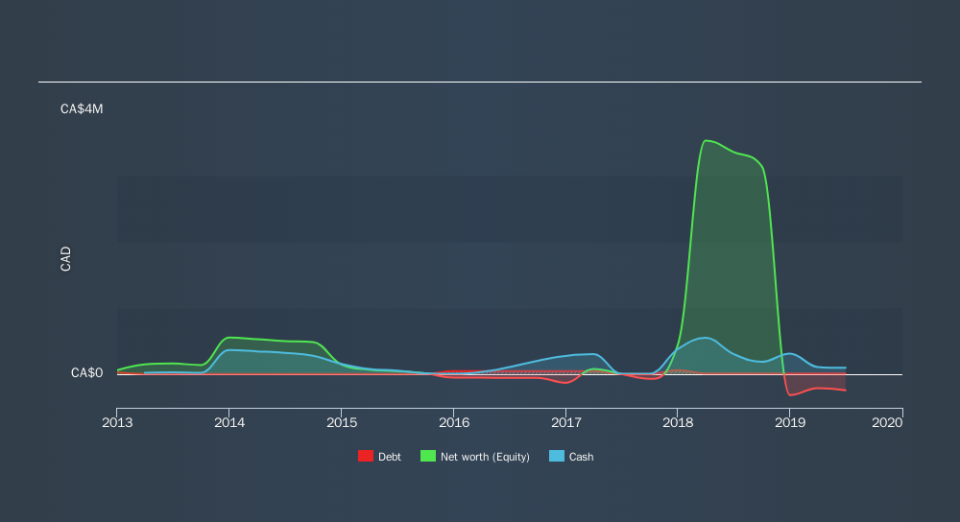

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. As at June 2019, Hybrid Minerals had cash of CA$91k and such minimal debt that we can ignore it for the purposes of this analysis. Looking at the last year, the company burnt through CA$695k. That means it had a cash runway of around 2 months as of June 2019. To be frank we are alarmed by how short that cash runway is! Depicted below, you can see how its cash holdings have changed over time.

How Is Hybrid Minerals's Cash Burn Changing Over Time?

Hybrid Minerals didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. With the cash burn rate up 13% in the last year, it seems that the company is ratcheting up investment in the business over time. That's not necessarily a bad thing, but investors should be mindful of the fact that will shorten the cash runway. Admittedly, we're a bit cautious of Hybrid Minerals due to its lack of significant operating revenues. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

Can Hybrid Minerals Raise More Cash Easily?

Since its cash burn is moving in the wrong direction, Hybrid Minerals shareholders may wish to think ahead to when the company may need to raise more cash. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash to fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Hybrid Minerals's cash burn of CA$695k is about 146% of its CA$475k market capitalisation. Given just how high that expenditure is, relative to the company's market value, we think there's an elevated risk of funding distress, and we would be very nervous about holding the stock.

Is Hybrid Minerals's Cash Burn A Worry?

As you can probably tell by now, we're rather concerned about Hybrid Minerals's cash burn. In particular, we think its cash runway suggests it isn't in a good position to keep funding growth. While not as bad as its cash runway, its increasing cash burn is also a concern, and considering everything mentioned above, we're struggling to find much to be optimistic about. Its cash burn situation feels about as comfortable as sitting next to the lavatory on a long haul flight. The need for more cash seems just around the corner, and any dilution is likely to be rather severe. While we always like to monitor cash burn for early stage companies, qualitative factors such as the CEO pay can also shed light on the situation. Click here to see free what the Hybrid Minerals CEO is paid..

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.